Choose a site

Localization Settings

Current Selection

Americas

Asia Pacific

Europe

Search

Account

Products

Mutual Funds

Mutual Fund Finder U.S. Equity International Equity Fixed Income Multi-Asset Target Date Money Market LiteratureSeparately Managed Accounts (SMAs)

Overview SMA Finder U.S. Equity International Equity Fixed Income Multi-Asset LiteratureModel Portfolios

Overview Target Allocation Building Block OutcomeExchange-Traded Funds (ETFs)

Overview ETF Finder U.S. Equity International Equity Fixed Income LiteratureCollective Investment Trusts (CITs)

Overview CIT Finder U.S. Equity International Equity Fixed Income Target Date LiteratureAlternatives

T. Rowe Price OHA Select Private Credit FundResources

Tax Center Capacity Constrained Strategies Product Literature FinderCapabilities

How we’ve helped investors navigate 20 years of market ups and downs.

Insights

Tectonic shifts create new opportunities.

Portfolio Construction

Learn how our Asset Allocation Committee is positioning its portfolios.

How your peers are positioning their portfolios and related insights.

Practice Management

Build trust, boost satisfaction, get results. Consider what coaching can do for you.

About

How we’ve helped investors navigate 20 years of market ups and downs.

Tectonic shifts create new opportunities

The economic distortions of the past few years have produced major changes to the global investment landscape. We are in a new regime of higher interest rates and stickier inflation. Investors will need to adapt to this new normal but could find opportunities by staying agile and taking a broad view. Read our 2024 Global Market Outlook for timely insights on navigating this transformed world.

Three themes for a world transformed

Global economies have stayed resilient amid uncertainty, but investors will need to adapt themselves to a new market regime.

We think the Fed is likely to remain on hold in 2024. High yield and shorter-term investment-grade corporate bonds could offer opportunities.

Equity investors may benefit from casting wider nets in 2024. We see opportunities in Japan, emerging markets, health care, and artificial intelligence (AI).

Global economies have stayed resilient amid uncertainty, but investors will need to adapt themselves to a new market regime.

We think the Fed is likely to remain on hold in 2024. High yield and shorter-term investment-grade corporate bonds could offer opportunities.

Equity investors may benefit from casting wider nets in 2024. We see opportunities in Japan, emerging markets, health care, and artificial intelligence (AI).

Key takeaways from our 2024 Global Market Outlook

Summary with global Investment Specialist Ritu Vohora, CFA®

The economic distortions stemming from the pandemic have produced tectonic shifts in the global investment landscape. Investors have had to navigate conflicting macroeconomic signals and a market narrative that has gyrated almost every few weeks.

Many economies have been resilient in 2023, despite aggressive rate hikes and tightening liquidity. This has fueled hopes of a soft landing. However, as we head into 2024, uncertainties remain. Global growth is at risk, as the long and variable lags of monetary policy start to bite. And while inflation is rolling over, there’s a risk it will inflect higher. We remain neutral on stocks and bonds overall.

Bond yields have been on a roller coaster ride in 2023. While central banks are likely at the end of their hiking cycles, the baton of volatility will be handed from the short end to the long end of the yield curve—given supply dynamics and an uncertain economic outlook.

We think rate cuts will materialize later than markets expect, but the Fed will remain data dependent. A steepening of global yield curves is likely to be a more significant driver for markets than the outlook for short-term rates.

Attractive yields provide the opportunity to lock in income in high-quality bonds. Shorter-term investment-grade bonds, high yield bonds, and emerging market debt also offer opportunities.

The massive outperformance of the “Magnificent Seven” tech stocks has been a defining feature of equity markets in 2023. 2024 may invite broader equity opportunities and warrants a diversified approach. Delivery on earnings expectations will be key.

Alongside generative AI, health care innovation and falling energy productivity are structural areas of opportunity. We also see select opportunities in Japan, emerging markets, and small-caps.

Tectonic market shifts will create new opportunities to put cash to work in 2024. It will also demand a greater focus on fundamentals, diversification, and risk management. A fertile ground for active investors.

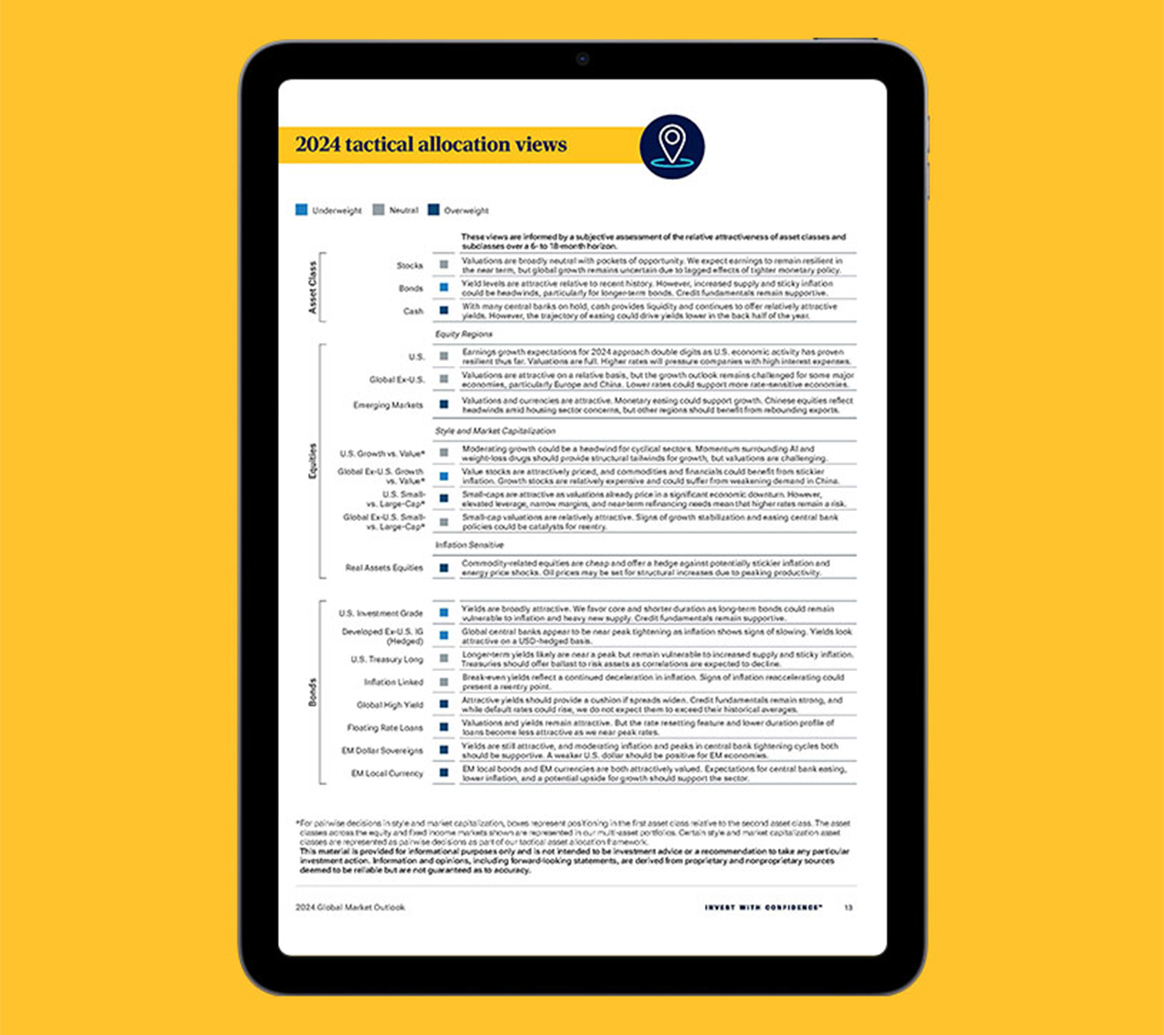

Tactical allocation views

Investment professionals from the T. Rowe Price Multi-Asset Division present their views on the relative attractiveness of asset classes and subclasses over the next six to 18 months.

Watch the CE webinar replay

Our chief investment officers weigh in on the state of markets and the economy heading into 2024. Continuing education (CE) credits available for financial professionals.

Important Information

CFA® and Chartered Financial Analyst are registered trademarks owned by CFA® Institute.

This material is provided for informational purposes only and is not intended to be investment advice or a recommendation to take any particular investment action.

The views contained herein are those of the speaker as of December 2023 and are subject to change without notice; these views may differ from those of other T. Rowe Price associates.

This information is not intended to reflect a current or past recommendation concerning investments, investment strategies, or account types, advice of any kind, or a solicitation of an offer to buy or sell any securities or investment services. The opinions and commentary provided do not take into account the investment objectives or financial situation of any particular investor or class of investor. Please consider your own circumstances before making an investment decision.

Information contained herein, including forecasts and forward-looking statements, is based upon sources we consider to be reliable; we do not, however, guarantee its accuracy or completeness. There is no guarantee that any forecasts made will come to pass.

The specific securities identified and described are for illustrative purposes only and do not represent all of the securities purchased, sold, or recommended by T. Rowe Price, and no assumptions should be made that investments in the securities identified and discussed were or will be profitable.

Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

All investments involve risk, including possible loss of principal.

International investments can be riskier than U.S. investments due to the adverse effects of currency exchange rates, differences in market structure and liquidity, as well as specific country, regional, and economic developments. These risks are generally greater for investments in emerging markets.

Small-cap stocks are generally more volatile than stocks of large, well-established companies.

Fixed income investing includes interest rate risk and credit risk. When interest rates rise, bond values generally fall. Investments in high yield bonds involve greater risk of price volatility, illiquidity, and default than higher-rated debt.

Investments concentrating in a specific sector can be more volatile than investments in a broader range of industries.

Diversification cannot assure a profit or protect against loss in a declining market.

T. Rowe Price Investment Services, Inc., distributor.

© 2023 T. Rowe Price. All Rights Reserved. T. ROWE PRICE, INVEST WITH CONFIDENCE, and the Bighorn Sheep design are, collectively and/or apart, trademarks or registered trademarks of T. Rowe Price Group, Inc.

202312-3272148