Client Conversations

It's Time to Get Serious About Retirement Income Solutions

Key Insights

- Thoughtful consideration of a participant’s journey, both up to and through retirement, can help participants meet their retirement goals—and better position plans to retain assets.

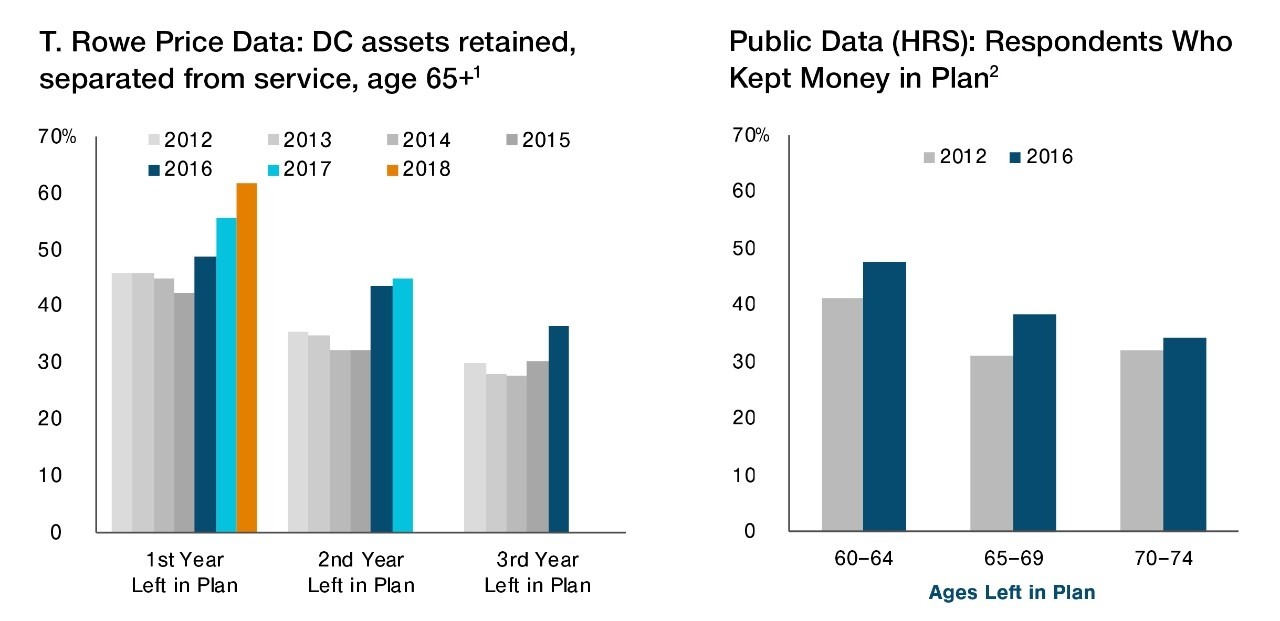

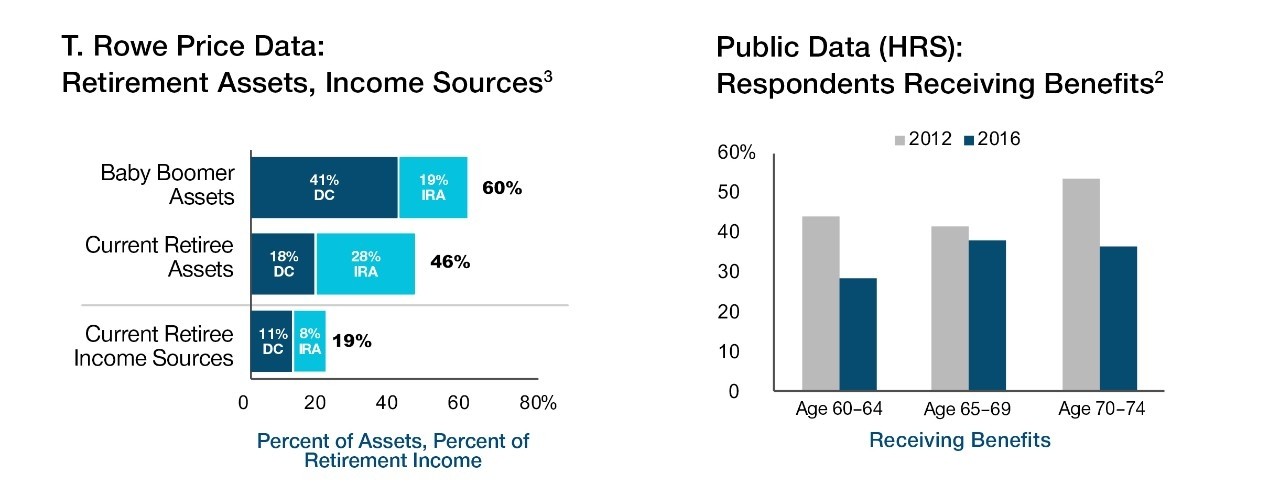

- More defined contribution (DC) plan participants are keeping their savings in plan after they retire, and future retirees expect to derive a greater share of retirement income from their DC plan balances.

- Despite more assets remaining in plans, money is being distributed at lower levels. This suggests that participants may need help converting DC plan assets into an income stream once they reach retirement.

- Every participant has their own unique circumstances that will impact their preferences for certain product features, such as income yield, income duration, income volatility, asset liquidity, and asset preservation.

- There is no one-size-fits-all solution for retirement income. Participants’ unique and changing needs require various solutions to help them achieve their goals.

Important Information

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass.

The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other

T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

USA—Issued in the USA by T. Rowe Price Associates, Inc. and T. Rowe Price Investment Services, Inc., 100 East Pratt Street, Baltimore, MD, 21202, which are regulated by U.S. Securities and Exchange Commission and the Financial Industry Regulatory Authority, respectively. For Institutional Investors only.

© 2021 T. Rowe Price. All rights reserved. T. ROWE PRICE, INVEST WITH CONFIDENCE, and the bighorn sheep design are, collectively and/or apart, trademarks or registered trademarks, of T. Rowe Price Group, Inc.