Manufacturing revival complicates inflation fight

June 2026, Fixed Income

Global inflation may prove far more persistent than markets currently expect, and a revival in the manufacturing cycle could be a major reason why.

While investors have focused on short-term energy price spikes tied to geopolitical tensions, a broader shift may already be underway beneath the surface.

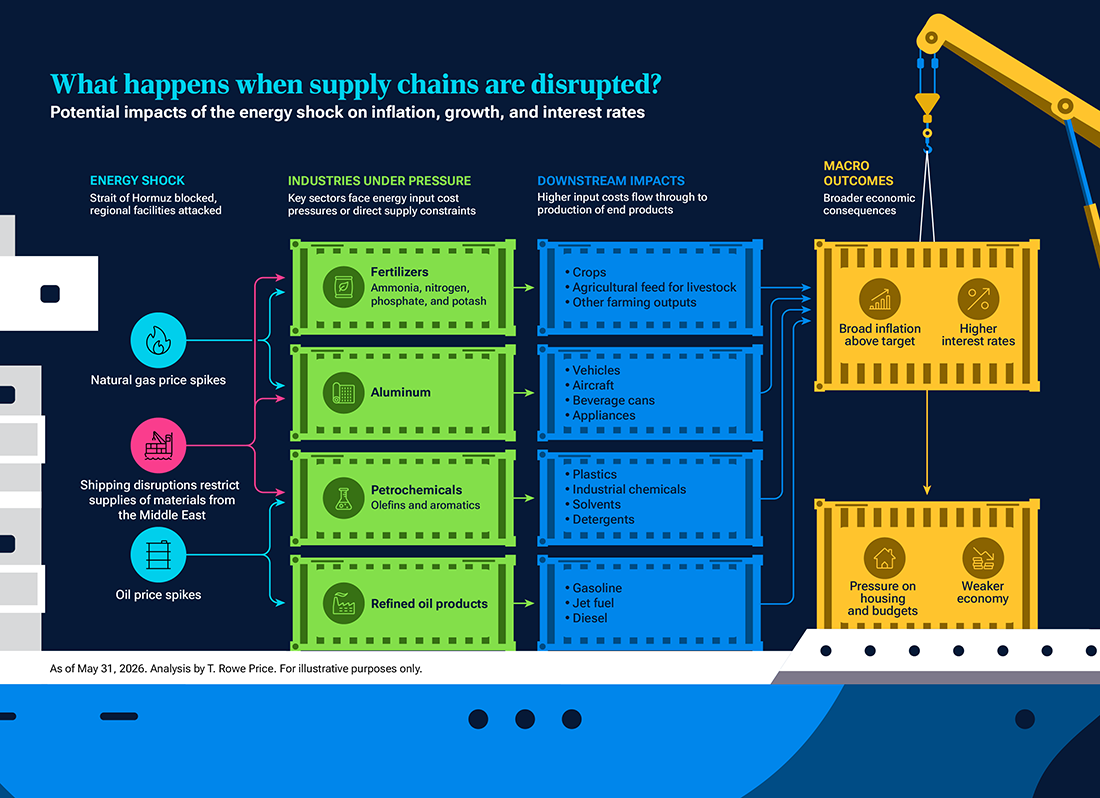

Around the world, central banks are facing a very difficult balancing act. Inflation remains elevated, yet shortages of refined oil products could weigh on growth in nations such as the UK, New Zealand, and Australia.

This combination raises the risk of stagflation and can complicate policy decisions.

At the same time, the global manufacturing cycle appears to be turning higher after several years of weakness.

In China, industrial companies are already beginning to raise prices as demand improves and raw material costs climb.

Producer prices have already started moving higher again, and we’re already starting to see signals that inflationary pressures may be spreading beyond energy markets alone.

Markets may be underestimating these less obvious forces. So even if oil supply disruptions ease, structural inflation tied to manufacturing activity and industrial pricing may remain.

For investors, long inflation breakeven exposures could become hedges to consider for portfolios with credit exposure, and there may be opportunities in strategies positioned for changing interest rate expectations and evolving global growth dynamics.

Rising inflation worldwide is prompting central banks to abandon the rate‑cutting cycle earlier than expected or, in some cases, to resume hiking rates. Fiscal policy is pulling in the other direction as governments use fuel subsidies and other support measures to soften the growth hit from the Iran war. A revival in global manufacturing now looks set to add to these pressures, which would make inflation broader and more durable than markets expect.

Nations such as the UK, New Zealand, and Australia will have to contend with the growth effects of a potential longer‑term shortage of refined oil products such as jet fuel and diesel, leaving central banks to grapple with stagflationary outcomes that make their policy decisions much more difficult.

Further complicating this backdrop are clear signs of a sustained pickup in global manufacturing Purchasing Managers’ Indexes (PMIs) after a three‑year downtrend in the manufacturing cycle (Figure 1). Additionally, last year the Chinese government announced its “anti‑involution” drive to curb overinvestment and support profit margins across various industrial sectors. While the actual impact of this policy is debatable, its effects reached the Chinese economy around the same time that the global manufacturing cycle reached a bottom and started to turn positive.

Manufacturing PMIs are recovering

As of April 30, 2026.

Sources: S&P Global Business Surveys—Manufacturing PMI (seasonally adjusted index data). PMIs above 50 indicate expansion and below 50 indicate contraction.

The year‑over‑year change in China’s producer price index turned positive in March. Conversations with management teams at Chinese industrial companies suggest that nearly all have been raising prices to offset higher raw material costs and to respond to firmer demand.

Markets have priced in the short‑term implications of the supply‑driven rise in oil prices but not the more persistent inflation tied to the upturn in the global manufacturing cycle and industrial price increases driven by more expensive raw materials. This has created a scenario where markets are trying to look through a short‑term inflationary spike on the assumption that the Strait of Hormuz will be opened relatively quickly—but investors may be disappointed by structural inflation that could remain after the immediate energy supply crunch.

Investment implications

- Positioning for U.S. yield curve flattening could benefit from a combination of less disinflation from Chinese imports and an accelerating manufacturing cycle.

- Long inflation breakeven1 exposures could become hedges to consider for portfolios that have underlying credit exposure.

ETFs are bought and sold at market prices, not NAV. Investors generally incur the cost of the spread between the prices at which shares are bought and sold. Buying and selling shares may result in brokerage commissions which will reduce returns.

202606-5571695

Strategies to Consider

- June 2026

- On the Horizon

Supply shock sparks energy security push

Contact us

1 Long inflation breakeven is a strategy that aims to profit if the spread widens between nominal bond yields and Treasury inflation protected securities (TIPS) yields. Investments that employ this strategy often involve shorting nominal bonds or using derivatives such as inflation swaps.

Appendix

Financial terms: Investors in the U.S. and Canada, for a glossary of financial terms, please go to troweprice.com/glossary.

Investment Risks:

Active investing may have higher costs than passive investing and may underperform the broad market or passive peers with similar objectives. Each person’s investing situation and circumstances differ. Investors should take all considerations into account before investing.

International investments can be riskier than U.S. investments due to the adverse effects of currency exchange rates, differences in market structure and liquidity, as well as specific country, regional, and economic developments. The risks of international investing are heightened for investments in emerging market and frontier market countries. Emerging and frontier market countries tend to have economic structures that are less diverse and mature, and political systems that are less stable, than those of developed market countries.

Commodities are subject to increased risks, such as higher price volatility and geopolitical and other risks. Commodity prices can be subject to extreme volatility and significant price swings.

Inflation‑linked bonds (Treasury inflation protected securities in the U.S.): In periods of no or low inflation, other types of bonds, such as U.S. Treasury bonds, may perform better than Treasury inflation protected securities (TIPS).

All investments involve risk, including possible loss of principal.

Fixed income securities are subject to credit risk, liquidity risk, call risk, and interest rate risk. As interest rates rise, bond prices generally fall.

Derivatives may be riskier or more volatile than other types of investments because they are generally more sensitive to changes in market or economic conditions; risks include currency risk, leverage risk, liquidity risk, index risk, pricing risk, and counterparty risk.

Investments that short securities employ leverage that would magnify any losses.

T. Rowe Price cautions that economic estimates and forward‑looking statements are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual outcomes could differ materially from those anticipated in estimates and forward‑looking statements, and future results could differ materially from any historical performance. The information presented herein is shown for illustrative, informational purposes only. Any historical data used as a basis for this analysis are based on information gathered by T. Rowe Price and from third‑party sources and have not been independently verified. Forward‑looking statements speak only as of the date they are made, and T. Rowe Price assumes no duty to and does not undertake to update forward‑looking statements.

Important Information

This material is being furnished for informational and/or marketing purposes only and does not constitute an offer, recommendation, advice, or solicitation to sell or buy any security.

Prospective investors should seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services.

Past performance is not a guarantee or a reliable indicator of future results. All investments involve risk, including possible loss of principal.

Information presented has been obtained from sources believed to be reliable, however, we cannot guarantee the accuracy or completeness. The views contained herein are those of the author(s), are as of June 2026, are subject to change, and may differ from the views of other T. Rowe Price Group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

All charts and tables are shown for illustrative purposes only. Actual future outcomes may differ materially from any estimates or forward‑looking statements provided.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

Issued in the USA by T. Rowe Price Investment Services, Inc., distributor and T. Rowe Price Associates, Inc., investment adviser, 1307 Point Street, Baltimore, MD 21231, which are regulated by the Financial Industry Regulatory Authority and the U.S. Securities and Exchange Commission, respectively.

© 2026 T. Rowe Price. All Rights Reserved. T. ROWE PRICE, INVEST WITH CONFIDENCE, the Bighorn Sheep design and related indicators (see troweprice.com/ip) are trademarks of T. Rowe Price Group, Inc. All other trademarks shown are the property of their respective owners. Use does not imply endorsement, sponsorship, or affiliation of T. Rowe Price with any of the trademark owners.

- 202606‑5512997