Concentration makes way for dispersion

June 2026, Equity

For much of the last decade, outperforming the index often came down to owning the market’s biggest technology companies. A small group of mega-cap leaders drove an outsized share of returns, making markets increasingly concentrated and challenging for active investors.

But that landscape may now be changing.

A new market cycle is emerging, one shaped by artificial intelligence, higher interest rates, and a renewed focus on infrastructure and deep capital investments.

The companies that once thrived with asset-light business models are now spending heavily to compete in the AI race.

Building data centers, expanding computing power, and investing in new technologies requires enormous amounts of capital, and that could pressure profitability and free cash flow in the near term.

At the same time, leadership in the market is broadening. Opportunities are expanding across industries, sectors, and regions.

For investors, this shift could mark an important turning point.

Rather than relying solely on passive exposure to concentrated benchmarks, success may increasingly depend on identifying companies that can turn higher investment into durable earnings growth and stronger returns on capital.

This is more than a market rotation.

This is a shift from concentration toward greater dispersion and active opportunity.

For much of the past decade, outperforming often meant owning more of the benchmark’s largest companies. A small group of mega‑cap, asset‑light platforms dominated equity returns, making active investors compete against a concentrated index. That dynamic is shifting as AI changes the economics of the market’s largest companies and broadens the opportunity set beyond the winners of the last cycle.

The post‑global financial crisis era rewarded duration, scale, and asset‑light models. Capital flowed to companies capable of delivering durable earnings growth with limited capital intensity. The post‑COVID world is different. Higher nominal growth, stickier inflation, higher rates, and the build‑out of AI infrastructure are rewarding businesses tied to infrastructure, industry, and capital investment.

The economics of the prior leaders are changing, too. Hyperscalers collectively are being pulled from asset‑light compounding into a capital‑intensive investment race. They may have little choice but to spend aggressively to defend their positions, but that spending can pressure free cash flow and alter return profiles.

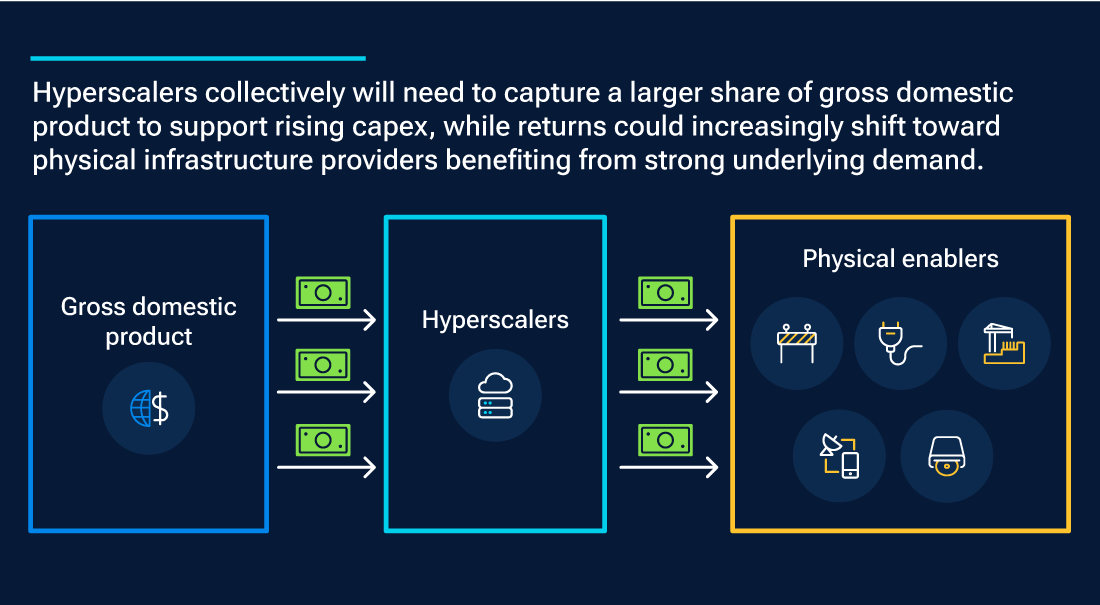

The great rotation

(Fig. 1) Returns may shift toward infrastructure providers

As of May 31, 2026.

Analysis by T. Rowe Price. For illustrative purposes only. Actual outcomes may differ materially.

For investors, the implications are significant. Index exposure remains highly concentrated even as the economics of the largest benchmark constituents become more complex. At the same time, leadership is broadening across sectors and geographies, widening the gap between companies that can turn higher investment into stronger returns on capital and those that cannot. Many beneficiaries of this cycle are also seeing improving relative growth, contributing to shifts in valuations and helping explain the recent underperformance of traditional quality and durable growth.

This creates a more challenging benchmark environment, but also a richer opportunity set for active investors who can distinguish between capex that could enhance returns and spending that dilutes them. It is more than a market rotation—it is a shift from concentration to dispersion. In the next phase, returns are likely to depend less on index exposure and more on identifying where capital intensity is creating better economics—not eroding them.

Investment implications

- Market leadership is broadening beyond a narrow group of mega‑cap technology companies, creating a more attractive environment for active security selection.

- As AI investment is likely to change corporate return profiles, companies converting capital spending into durable earnings growth may be better positioned than those facing weaker free cash flow.

ETFs are bought and sold at market prices, not NAV. Investors generally incur the cost of the spread between the prices at which shares are bought and sold. Buying and selling shares may result in brokerage commissions which will reduce returns.

202606-5571695

Strategies to Consider

- June 2026

- On the Horizon

Geopolitical fragmentation raises risk premium

Contact us

Appendix

Financial terms: Investors in the U.S. and Canada, for a glossary of financial terms, please go to troweprice.com/glossary.

Investment Risks:

Active investing may have higher costs than passive investing and may underperform the broad market or passive peers with similar objectives. Each person’s investing situation and circumstances differ. Investors should take all considerations into account before investing.

Investing in technology stocks entails specific risks, including the potential for wide variations in performance and unusually wide price swings, both up and down. Technology companies can be affected by, among other things, intense competition, government regulation, earnings disappointments, dependency on patent protection, and rapid obsolescence of products and services due to technological innovations or changing consumer preferences.

The value approach to investing carries the risk that the market will not recognize a security’s intrinsic value for a long time or that a stock judged to be undervalued may actually be appropriately priced. Growth stocks are subject to the volatility inherent in common stock investing, and their share price may fluctuate more than that of income‑oriented stocks.

All investments involve risk, including possible loss of principal. Diversification cannot assure a profit or protect against loss in a declining market.

T. Rowe Price cautions that economic estimates and forward‑looking statements are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual outcomes could differ materially from those anticipated in estimates and forward‑looking statements, and future results could differ materially from any historical performance. The information presented herein is shown for illustrative, informational purposes only. Any historical data used as a basis for this analysis are based on information gathered by T. Rowe Price and from third‑party sources and have not been independently verified. Forward‑looking statements speak only as of the date they are made, and T. Rowe Price assumes no duty to and does not undertake to update forward‑looking statements.

Important Information

This material is being furnished for informational and/or marketing purposes only and does not constitute an offer, recommendation, advice, or solicitation to sell or buy any security.

Prospective investors should seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services.

Past performance is not a guarantee or a reliable indicator of future results. All investments involve risk, including possible loss of principal.

Information presented has been obtained from sources believed to be reliable, however, we cannot guarantee the accuracy or completeness. The views contained herein are those of the author(s), are as of June 2026, are subject to change, and may differ from the views of other T. Rowe Price Group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

All charts and tables are shown for illustrative purposes only. Actual future outcomes may differ materially from any estimates or forward‑looking statements provided.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

Issued in the USA by T. Rowe Price Investment Services, Inc., distributor and T. Rowe Price Associates, Inc., investment adviser, 1307 Point Street, Baltimore, MD 21231, which are regulated by the Financial Industry Regulatory Authority and the U.S. Securities and Exchange Commission, respectively.

© 2026 T. Rowe Price. All Rights Reserved. T. ROWE PRICE, INVEST WITH CONFIDENCE, the Bighorn Sheep design and related indicators (see troweprice.com/ip) are trademarks of T. Rowe Price Group, Inc. All other trademarks shown are the property of their respective owners. Use does not imply endorsement, sponsorship, or affiliation of T. Rowe Price with any of the trademark owners.

- 202606-5512997