January 2024 / INVESTMENT INSIGHTS

Where we see opportunities in Asia ex-Japan equities

Key Insights

- We see compelling stock valuations and fundamentals in various parts of Asia ex-Japan, which supports our constructive view from the bottom up as we enter 2024.

- In China, pockets of cheap valuations, secular growth opportunities in electric vehicle and green energy supply chains, and an import substitution trend have our attention.

- India’s robust economy is a bright spot. More meaningful for Taiwan and South Korea is the technology hardware cycle, which we think is on a path to recovery.

Asia ex-Japan equities look set to finish a challenging year behind their developed market peers. However, the weak performance masks divergent returns across the region’s markets, reflecting the wide range of market drivers at play. We see compelling stock valuations and fundamentals in various parts of the investment universe, which supports our constructive view from the bottom up as we enter 2024.

Lower correlations across markets

We have long viewed Asia ex-Japan equities as a diverse asset class, and we believe the region’s markets have become even less correlated in the past few years. One way we currently think about the region is as a collection of three almost distinct components.

The first component comprises China and Hong Kong. China’s economic cycle has become increasingly more distinct from the rest of the world, with vital implications for Hong Kong. Lately, China’s regulatory cycle has distinguished both markets further. As a result, we have seen their valuations decouple from their regional peers.

India and much of Southeast Asia make up the next category. These markets have broadly benefited from a shift in foreign direct investment and portfolio flows away from China in recent years. Some economies, especially India and Indonesia, have also fared well on the back of sound government policies and strong domestic growth engines.

The third bucket is Taiwan, South Korea, and Singapore, three of the region’s most advanced markets. We view them as cyclicals with relatively greater exposure to the global economy. In particular, Taiwan and South Korea tend to be more closely linked to the technology hardware cycle.

Given the differentiated factors influencing each of these three buckets, their market performances understandably vary. We see a broadly balanced mix of stock valuations and fundamentals across the region. In our view, valuations for the China-Hong Kong component are compelling, though their fundamentals are less so. This contrasts with the strong fundamentals but less appealing valuations that we see in the India-Southeast Asia category. As for the bucket comprising Taiwan, South Korea, and Singapore, we find a lack of clear directional signals in terms of the global economic backdrop.

While the diversity of Asia ex-Japan markets should favor stock picking, finding winning stocks has been more difficult in recent times as macroeconomic events have overshadowed company fundamentals. We see this especially in China, where policy shifts have been a major market driver. Going forward, we expect fundamental factors to reassert themselves once more and an environment that is more conducive to bottom-up stock selection.

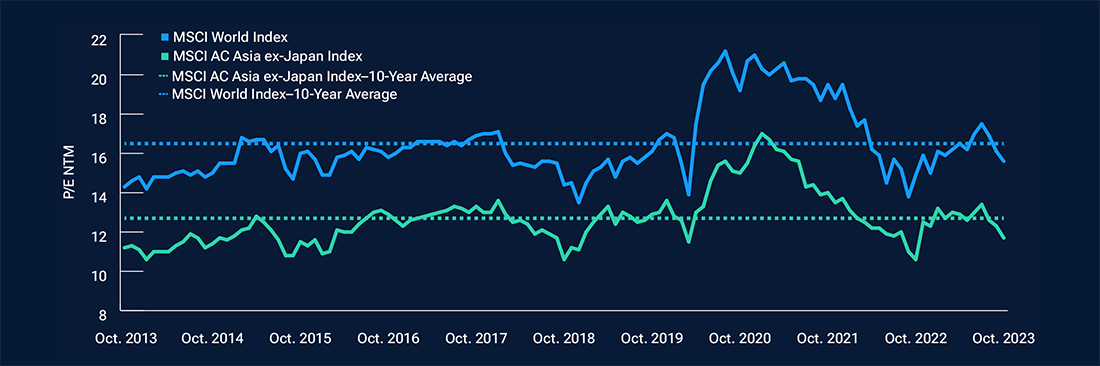

We remain constructive about investing in the region. Its overall valuation, relative to historical and developed market levels, looks attractive to us (Figure 1).

We also expect earnings improvements in markets such as India and Southeast Asia. In China, we see conditions turning more favorable for stock selection. Judging from our bottom-up research, many companies have braced themselves for a tougher operating environment and are pursuing self-help in various ways, seeking new markets, vying for market share, or increasing share buybacks, for example.

China: cheap valuations and more

At a broader level, we note three key areas of investment opportunity in China. The first is the pockets in the market where valuations look heavily depressed and fundamental conditions are stabilizing. Internet companies, for example, have endured years of intense government scrutiny, which we see easing. With a less punitive policy regime, businesses are now able to refocus on growth. In real estate, policies to curb leverage and home prices have eased marginally as officials shore up the economy, sending encouraging signals for some property stocks.

Second, we see secular growth opportunities for companies in industries where China is globally competitive. We believe companies along the electric vehicle and green energy supply chains are well positioned for multiyear expansion, not just domestically, but also abroad as they ramp up exports.

Related to the second tailwind is our third area of opportunity—import substitution in China. Geopolitical tensions have forced China to rely less on imports and to become more self-sufficient via accelerated innovation, especially when it comes to making semiconductors, software, autos, and a host of industrial products.

We see Chinese manufacturers building the capabilities to take market share from foreign competition within China. Furthermore, we think their success will enable them to gain market share outside of China.

Asia ex-Japan equities offer a discounted valuation

(Fig. 1) Next 12-month (NTM) price-to-earnings (P/E) ratios in Asia ex-Japan and the world

These statistics are not a projection of future results. Actual results may vary significantly.

As of October 31, 2023.

Source: Financial data and analytics provider FactSet. Copyright 2023 FactSet. All Rights Reserved.

Structural reforms buoy India

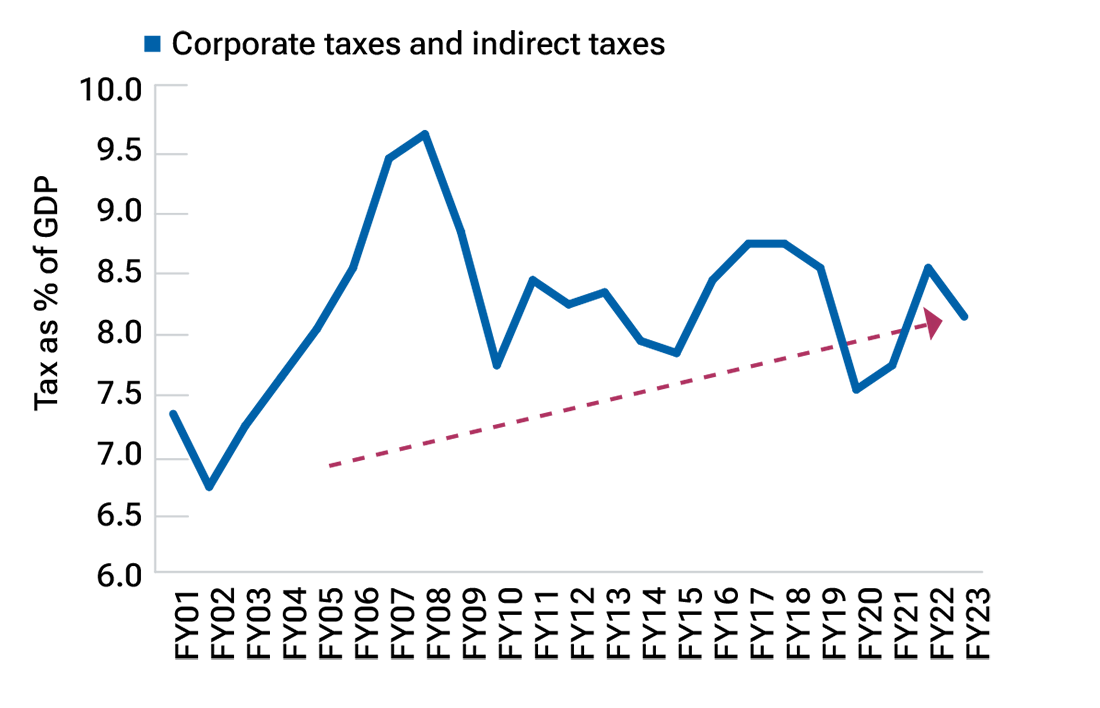

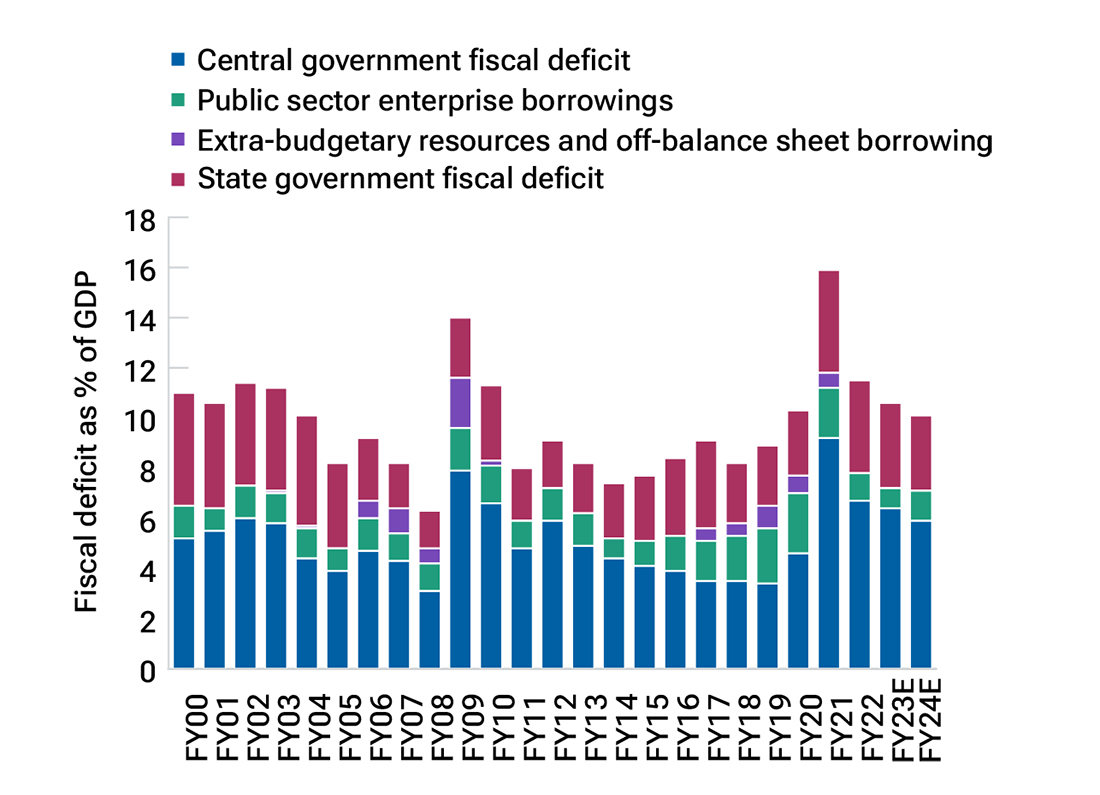

India’s robust economy is a bright spot in Asia ex-Japan, and we expect it to continue strengthening. We think it is reaping the rewards of structural reforms in the past few years. These include measures to lift tax revenues as a percentage of gross domestic product (GDP) and thereby improve the country’s fiscal position (Figure 2).

India’s “Make in India” initiative to become a global manufacturing hub, coupled with geopolitical friction that has prompted supply chain shifts, has also supported the economy.

The resilience of India’s economy has come through in the latest period of rising U.S. interest rates. In the past, higher U.S. rates typically sparked capital flows out of India, weighing on its finances and currency. A weaker Indian rupee would augur ill for inflation given the country’s heavy reliance on imports, especially oil. This time around, the vicious circle has not materialized given India’s much improved economic position. Indian companies have also weathered this period well, delivering good earnings growth.

Nonetheless, we are judicious about stock valuations in India, some of which appear hard to justify. We see multiples in certain areas rerating significantly ahead of projected earnings growth, which underscores the need for careful stock selection. In particular, stock multiples have climbed partly due to a surge in domestic investor inflows, especially in the mid-cap space. A reversal of these flows will hurt the stock market, in our view.

The promise in parts of Southeast Asia

India’s emergence as a manufacturing base highlights a similar trend that has benefited Vietnam in the past few decades. We think U.S.-China tensions have strengthened the case for companies globally, including Chinese businesses, to diversify the locations of their supply chains in favor of Vietnam. We expect sizable positive spillover effects for the economy as it continues to develop from a low base. Vietnam’s equity valuations have also moderated amid the government’s anticorruption campaign and a property market slowdown. We are watching the policy environment closely for signs of stabilization.

Elsewhere in Southeast Asia, we see positive catalysts emerging in Indonesia and the Philippines. Indonesia’s bid to diversify its economy away from commodity exports has led to increased infrastructure spending, a greater focus on investments in higher-value downstream industries, and a digitalization push. While it continues to enjoy gains from higher commodity prices in recent years, we expect its economy to become less exposed to the commodity cycle and more resilient over time.

The Philippines is unique for the large remittances it receives from a vast number of Filipinos working overseas. The inflows have traditionally supported domestic consumption, acting as a crucial source of stability for the economy when activity slows. Although the property market has been weak, we see indications of an improvement in 2024, which bodes well for the earnings of several major Philippine companies with real estate exposure.

India’s government finances show signs of structural improvement

(Fig. 2) Tax and fiscal deficit, each as a percentage of GDP

As of March 31, 2023. Most recent data available.

Sources: CMIE, CEIC, Morgan Stanley Research, IIFL Research, Indian government budget documents.

Note: India’s fiscal year begins in April, i.e. FY23 = April 2022 to March 2023. E = estimated. Actual outcomes may differ materiallyfrom estimates.

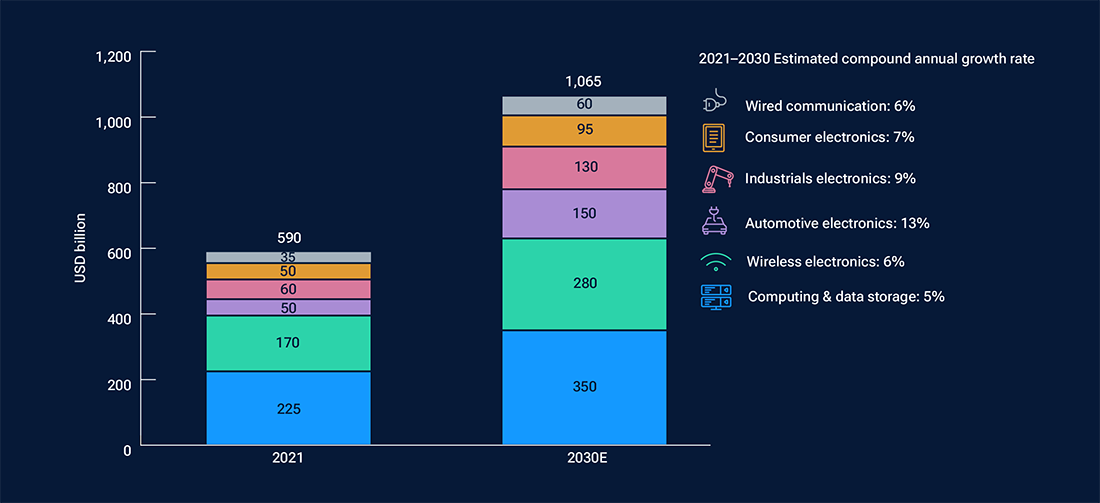

Technology hardware: eyeing a trough

In our view, Taiwan and South Korea stand out as homes to several world-leading technology companies, especially in the semiconductor space. More meaningful for these two markets is the technology hardware cycle, which we think remains on a path to recovery, even if progress has taken longer than expected. Improving trends in semiconductor prices are encouraging signs, we think. We also see the release of smartphones with new form factors in China triggering an upturn in smartphone demand.

Over time, we expect the rise of new technologies in various areas to boost semiconductor demand (Figure 3). In particular, we are optimistic about artificial intelligence (AI) potentially expanding the total addressable market for technology products. For example, smartphones’ adoption of AI may kindle a wave of mobile upgrades, bringing good news for smartphone-related companies in Asia ex-Japan.

What lies ahead

In short, despite a lackluster 2023 for Asia ex-Japan equities, we see plenty of investment opportunities on offer. The return drivers are diverse, which has become more apparent given our view of reduced correlations between the region’s markets. Navigating risks still matters—regulatory priorities in China and Vietnam, India’s general election next year, and U.S.-China relations are some areas to watch. However, we think bottom-up investors with a prudent eye on risks are well positioned for the year ahead.

New technologies are poised to boost semiconductor demand

(Fig. 3) Global semiconductor market outlook

Actual outcomes may differ materially from estimates.

As of May 31, 2023. Most recent data available.

Source: Morgan Stanley.

IMPORTANT INFORMATION

Where securities are mentioned, the specific securities identified and described are for informational purposes only and do not represent recommendations.

This material is being furnished for general informational purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. Investment involves risks. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

January 2024 / U.S. FIXED INCOME