September 2023 / MARKETS & ECONOMY

The Resilient Engine of the US Economy Could Stall

Consumer fundamentals seem to be weakening from a strong position

Key Insights

- We believe that consumer balance sheets remain healthy and are supportive of spending fundamentals.

- We see the recent worsening in debt quality as reason for some concern.

- The resumption of student debt payments for millions of borrowers in early fall is likely to present a key headwind to consumer spending.

Consumer spending typically has made up over 70% of the US economy and historically has been a significant driver of growth. At this juncture, the consumer balance sheet appears healthy after many years of deleveraging1 after the global financial crisis. However, we see two key risks to consumer spending heading into year‑end: rising consumer credit card debt and delinquencies and the resumption of student loan repayments.

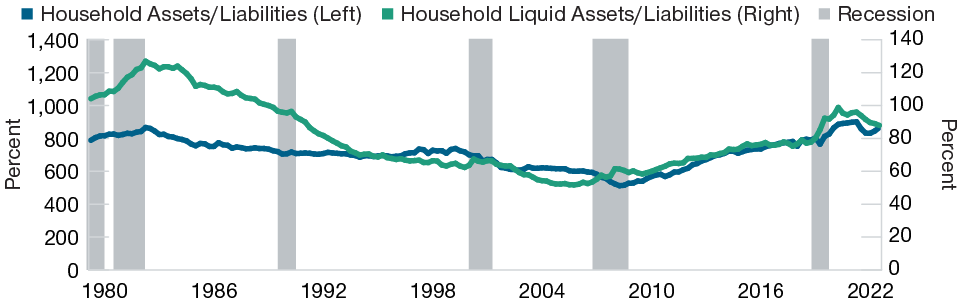

Consumer Debt Level Appears Manageable…

We believe that consumer balance sheets remain healthy and are supportive of spending fundamentals. Despite headlines about high debt levels, total and liquid assets as a share of liabilities are both high for US households. Unlike the 2000s, when consumers were over‑levered relative to their assets, today’s consumers do not need to deleverage. Checking account balances also remain well above pre-pandemic levels.

Household Assets Remain High Relative to Liabilities

(Fig. 1) US Household Balance Sheet Ratios

As of June 30, 2023.

Sources: Federal Reserve Board and Haver Analytics.

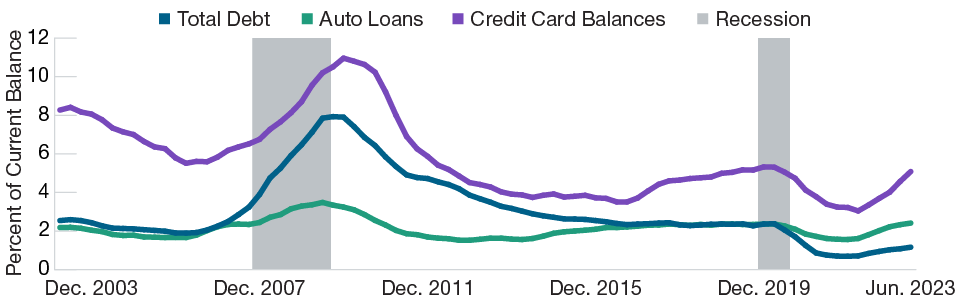

New Serious Delinquencies by Debt Category

(Fig. 2) Percentage of Balances Newly Delinquent

As of June 30, 2023.

Sources: Federal Reserve Bank of New York and Haver Analytics.

Additionally, debt servicing costs remain low relative to history, even with rising interest rates, and US consumers’ financial obligations remain manageable relative to disposable income. Mortgage debt represents a sizable proportion of total household debts, and many borrowers were able to lock in low mortgage rates in recent years. This has helped insulate a large portion of debt from higher interest rates.

…but Credit Card and Auto Loans Are Showing Signs of Stress

While our baseline expectation is for the US consumer to remain on a steady upward trajectory, we see the recent worsening in debt quality as reason for some concern. For instance, credit card and auto loan delinquencies have risen recently, particularly among younger borrowers. While overall delinquencies are still below pre-pandemic levels, the acceleration could be a sign that consumers are feeling the stress of rising interest rates and the squeeze to disposable incomes from high inflation. The recent rise in consumer bankruptcy filings could be another sign of stress.

Credit conditions for consumer loans have also tightened significantly in the past year, meaning they are less likely to fund large purchases with favourable loans. Banks face higher funding costs and heightened regulation to retain capital following the regional banking crisis in March 2023. According to the Fed’s Senior Loan Officer Opinion Survey on Bank Lending Practices, the proportion of banks less willing to lend to consumers has risen to historic highs.

Key Risks to the Consumer Outlook

Following the US Supreme Court’s ruling on student loan debt forgiveness, the resumption of student debt payments for millions of borrowers starting in October is likely to present a key headwind to consumer spending in the fourth quarter of 2023 and into 2024. We anticipate that student loan payments will have a larger impact on younger borrowers, who are already displaying pockets of weakness in the form of increased delinquencies on credit cards and auto loans.

Finally, the excess savings accumulated during the height of the pandemic across developed economies has been dwindling. While there is some debate about exactly when the excess savings will be completely depleted, most analyses indicate this buffer will have run out by the end of 2023. Without the savings buffer to smooth over the shocks of rising prices, interest rates, or the resumption of student loan repayments, the US consumer could be under increased pressure.

T. Rowe Price cautions that economic estimates and forward-looking statements are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual outcomes could differ materially from those anticipated in estimates and forward-looking statements, and future results could differ materially from historical performance. The information presented herein is shown for illustrative, informational purposes only. Any historical data used as a basis for analysis are based on information gathered by T. Rowe Price and from third-party sources and have not been verified. Forecasts are based on subjective estimates about market environments that may never occur. Any forward-looking statements speak only as of the date they are made, and T. Rowe Price assumes no duty to and does not undertake to update forward-looking statements.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

September 2023 / MARKETS & ECONOMY

Blerina Uruçi is the chief U.S. economist in the Fixed Income Division. She contributes to the formulation of investment strategy and supports investment and client development activities throughout T. Rowe Price, specifically focusing on the outlook for the U.S. economy, inflation, and monetary policy. Blerina is a vice president of T. Rowe Price Group, Inc., and T. Rowe Price Associates, Inc.