T. Rowe Price

T. Rowe Price

Global Structured Research Equity

An active, global equity portfolio seeking to provide long-term capital appreciation with low tracking error.

What is the Global Structured Research Equity Strategy?

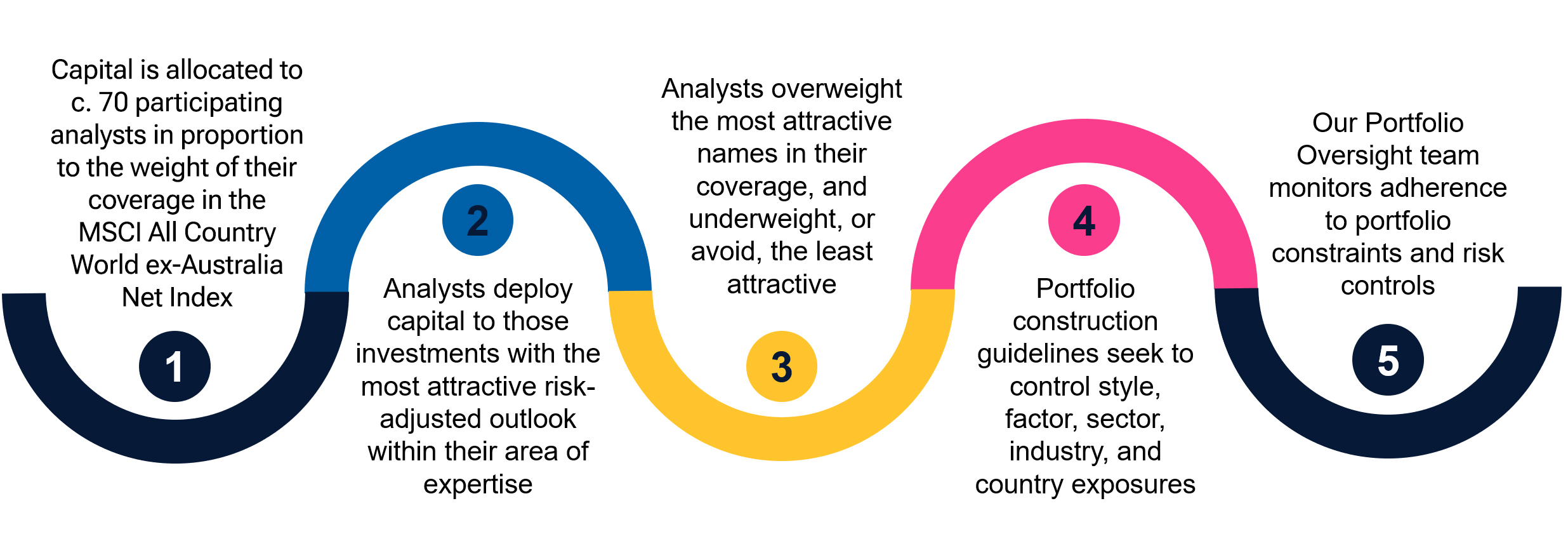

The Global Structured Research Equity Strategy (GSRS) is a core equity strategy designed to provide clients with broad exposure to the core segment of the global equity market. This actively managed portfolio leverages analyst-driven stock selection, typically involving around 70 analysts, seeks to achieve diversified global exposure with low tracking error relative to the MSCI All Country World ex Australia Net Index. The strategy holds between 750 and 1,000 stocks and operates under the oversight and discretion of portfolio managers, aiming to consistently add value through fundamental stock selection across a wide range of market environments.

Risk-managed alpha

Aims to offer low tracking error alternatives to passive allocations, providing benchmark-like risk characteristics with added opportunity for alpha generation.

Consistent performance

Pursues performance across different market environments with less exposure to extreme style or sector leadership changes.

Deeply researched

Provides access to the fundamental company insights of our c.70-strong world-class equity research team in the purest form.

How does it work?

The strategy utilises a clearly defined investment process which involves our industry-focused investment analysts making buy and sell decisions within their individual areas of expertise, subject to the oversight and discretion of the Portfolio Managers.

Ways to invest

The T. Rowe Price Global Structured Research Equity Strategy is available as both hedged and unhedged solution.

T. Rowe Price Global Structured Research Equity Fund- I Class

APIR: ETL4238AU

| Inception date | 29 July 2025 |

| Benchmark | MSCI All Country World ex Australia Net Index |

| No. of holdings | 750–1000 |

| Management fees and costs^ | 0.50% pa |

| Distribution | Annual |

Fund literature

^The Management Fee for the T. Rowe Price Global Structured Research Equity Fund - I Class is 0.50% p.a. and the Indirect Cost is 0.05% p.a. The indirect costs component is based on a reasonable estimate of the costs for the current financial year to date, adjusted to reflect a 12 month period. Full details of other fees and charges are available within the Fund's Product Disclosure Statement and Reference Guide.

T. Rowe Price Global Structured Research Equity Fund (Hedged)- I Class

APIR: ETL0944AU

| Inception date | 29 July 2025 |

| Benchmark | MSCI All Country World ex Australia Net Index (Hedged to AUD) |

| No. of holdings | 750–1000 |

| Management fees and costs^ | 0.52% pa |

| Distribution | Annual |

Fund literature

^The Management Fee for the T. Rowe Price Global Structured Research Equity Fund (Hedged) - I Class is 0.52% p.a. and the Indirect Cost is 0.05% p.a. The indirect costs component is based on a reasonable estimate of the costs for the current financial year to date, adjusted to reflect a 12 month period. Full details of other fees and charges are available within the Fund's Product Disclosure Statement and Reference Guide.

Quarterly Analyst Spotlight Webinar

How AI Is Reshaping the Industrial Opportunity Set

Our Analyst Spotlight webinar series allows you to hear directly from the experts behind our Structured Research Equity strategies (SRS). Portfolio Specialist Tamzin Manning was joined by Investment Analyst Bill Ledley who covers Industrials.

As AI drives a new wave of demand for power, cooling, connectivity, and infrastructure, the opportunity set across industrials is evolving quickly. In this update, Bill explains where he sees the strongest secular tailwinds, which companies are standing out, and what the market may still be underappreciating.

Hi everyone. Thanks so much for joining us today as we provide insight into the work of our research team.

Today joining me is Bill Ledley, whose coverage includes many of the leading providers of data centre power and utility infrastructure, a key focus of the market today.

Hi Bill, thanks so much for joining us.

As mentioned, you manage a sleeve of the portfolio focused on the industrial sector and we currently have a somewhat unusual industrial backdrop with parts of the industrial economy slowing while areas related to AI and electrification are accelerating.

How has that divergence shaped how you're allocating capital today?

Sure, Tamzin.

First off, it's important to remember that divergences create opportunities for fundamental investors.

Understanding where companies are and their business cycle is a critical part of my process and informs which stocks I want to own and when.

Over the past few years, we've seen a wide divergence in industrials as sectors with powerful secular tailwinds such as data center, utility and power infrastructure, have strongly outperformed, whereas other sectors of the US industrial economy have suffered through rolling recessions such as ag and construction machinery, electronic test and measurement, industrial automation and housing.

Going forward, I expect those secular tailwinds to remain strong, but I believe it's increasingly important to identify and focus on those companies that are separating themselves from the pack.

In my view, these true winners can develop and deploy differentiated technology capabilities and service at scale.

That said, some industries look poised to return to growth, which is typically a very attractive setup for cyclical stocks.

Within this group, the best opportunities in my view are those companies whose long-term growth opportunities were overly discounted at the bottom of their business cycle.

Thanks Bill.

Let's focus in on what continues to be the biggest theme in markets today, AI and infrastructure.

AI is becoming increasingly capital intensive in the physical world.

From your perspective, where are you seeing the most compelling second order effects of this in industrials?

The most compelling opportunities I see are companies who are increasingly separating themselves from the pack. In an environment where customers are not only starred for compute, but are also struggling to deploy increasingly complicated large and powerful GPU clusters.

Being able to develop and deploy differentiated technology, capability and service at scale will produce outsized earnings growth in my view.

I believe this is true across all facets of data center development, including power, cooling, labor and connectivity, all of which are increasingly constrained by the way.

You’ve highlighted the intensity of power and thermal requirements as rack densities increase.

How does that dynamic change the opportunity set for companies exposed to data center infrastructure?

Data centers are getting bigger, more complex and hotter.

Infrastructure requirements are changing almost daily given the pace of innovation.

As such, suppliers of data center infrastructure have seen large increases in their adjustable market as measured on a dollar per MW basis as legacy systems grow in size and complexity and as new systems get deployed, such as liquid cooling.

As the leading provider of data center power and thermal management systems, Vertiv is exceptionally well positioned for this trend, which is why the company remains a large position.

For me, Vertiv is also an example of a company that is separating itself from the competition through product innovation, manufacturing capabilities, and service footprint.

For instance, the company's ability to integrate pieces of the power and thermal management change into modular design reduces data center complexity and decreases installation time.

Further, Vertiv has established itself as a leading supplier of liquid cooling, giving the company a very attractive growth opportunity as liquid cooling penetration increases globally.

Of course, all this is enabled by Vertiv’s close partnership with NVIDIA, which fosters continued innovation and aligns Vertiv product road map with future customer needs.

Thanks, Bill.

So alongside the physical build out, there's also a layer of increasing complexity in the underlying technology, particularly in these areas like networking, semiconductors and communications.

How are you thinking about companies that are effectively enabling that innovation?

I believe addressing the increasing complexity of data centers and AI infrastructure is a strategic imperative for hyperscalers and their partners.

Every kilowatt of power is precious and decreasing latency of token generation helps differentiate frontier models and improve the user experience.

Further, we are seeing the development of custom ASICS that are designed to handle new AI specific workloads.

All this bodes exceptionally well for Keysight in my view. The company can be viewed as a pick-and-shovel supplier for technical and for technological innovation as the company is the leading supplier of critical electronic tests and measurement equipment for R&D labs and leading edge manufacturing facilities.

The company's growth opportunity looks exceptionally strong over the next three to five years, driven by global defence modernization, increasing semiconductor manufacturing capacity and complexity, accelerating innovation cycles for wired communications such as 800 gig and 1.6 terabit ethernet, autonomous vehicles, and ultimately to the development of 6G wireless.

Furthermore, many of these innovations are increasingly intertwined, such as the need for powerful, secure and precise communication networks that enable the proliferation of autonomous vehicles or the eventual move of AI from the cloud to edge devices.

Thanks Bill. This is just so fascinating.

And in a sense, you're capturing AI from two angles - physical infrastructure and the innovation ecosystem. As that build out accelerates, you know, power availability is becoming a real constraint and increasingly it's about speed to market.

How should investors think about power generation solutions that can accelerate time to power for these data centres?

As I said before Tamzin, every kilowatt of power is valuable right now and the competition to establish the best in class frontier model is pushing up the importance of speed to market or in this case time to power.

In my view, Caterpillar is exceptionally well positioned with its behind-the-meter solutions that enable much faster time to power.

The company's reputation is already best in class with data center operators given the company's leading position in backup generators, and Caterpillar is only building on this reputation.

The company's Solar Turbines franchise has decades of experience delivering prime power for off grid facilities, making their solutions an attractive option for data center developers facing 5 plus year wait times to secure power from the grid.

Caterpillar's ability to provide local market service is also differentiated in my view.

Furthermore, the company's construction machines are being used to build these data centers in addition to a host of other industrial mega projects.

And ultimately, I believe Cat's mining franchise will also be called upon to address the world's growing shortage of copper and other mining materials.

Lastly, Caterpillar is also leading the way for the development and deployment of physical AI.

The company has already embedded AI capabilities for operators to use across all their machines.

The company's global position gives cat head start in designing and innovating novel ways to extend AI to the digital realm and into the physical realm to unlock productivity, improve safety and increase output.

It's so interesting to me how this traditional business is now becoming an AI play.

So one last question to wrap up today, where do you have the highest conviction as things are today and what do you think the market is still underappreciating?

Keysight remains my highest conviction idea, which is why the stock is my largest position.

In my view, the market still doesn't appreciate the strength of Keysight's competitive position, nor does the market fully appreciate the multitude and size of Keysight's opportunities over the next three to five years.

Lastly, the current wave of technological innovations are increasingly intertwined, which creates a fantastic environment for Keysight.

These dynamics coupled with an attractive cyclical starting point make hindsight my highest conviction idea.

Thanks so much Bill for your time today and for sharing these insights.

Of course, thanks for having me.

View our latest insights

Restoring America’s nuclear energy capacity—digging in to potential impacts and implications

Jun 2025

In the Spotlight

Jun 2025

In the Spotlight

The Power of Alternative Data in Company Analysis

May 2025

From the Field

May 2025

From the Field

Dynamic markets may favor a hybrid of active and passive investing

Additional Disclosures

MSCI and its affiliates and third party sources and providers (collectively, “MSCI”) makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed, or produced by MSCI. Historical MSCI data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. None of the MSCI data is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

To the extent the Fund invests in another commingled vehicle(s), such vehicles may apply additional exclusions on top of what is stated in the PDS. Currently, the Fund will either hold securities directly or gain exposure by investing in the T. Rowe Price Funds SICAV Global Structure Research Equity Fund, which has additional exclusions relating to controversial weapons, coal, assault-style weapons, adult entertainment, gambling and conduct-based. More information around these exclusions, can be found on the Exclusion Policy on our webpage at troweprice.com.

Important Information

Available in Australia for Wholesale Clients only. Not for further distribution.

Equity Trustees Limited (“Equity Trustees”) (ABN: 46 004 031 298, AFSL: 240975), is the Responsible Entity for the T. Rowe Price Australian Unit Trusts ("the Fund"). Equity Trustees is a subsidiary of EQT Holdings Limited (ABN: 22 607 797 615), a publicly listed company on the Australian Securities Exchange (ASX: EQT).

This material has been prepared by T. Rowe Price Australia Limited ("TRPAU") (ABN: 13 620 668 895, AFSL: 503741) to provide you with general information only. In preparing this information, we did not take into account the investment objectives, financial situation or particular needs of any particular person. It is not intended to take the place of professional advice and you should not take action on specific issues in reliance on this information. Neither TRPAU, Equity Trustees nor any of its related parties, their employees or directors, provide any warranty of accuracy or reliability in relation to such information or accepts any liability to any person who relies on it.

Past performance is not a guarantee or a reliable indicator of future results. You should obtain a copy of the Product Disclosure Statement, which is available from Equity Trustees (www.eqt.com.au/insto) or TRPAU (www.troweprice.com.au), before making a decision about whether to invest in the Fund named in this material.

The Fund’s Target Market Determination is available here. It describes who this financial product is likely to be appropriate for (i.e. the target market), and any conditions around how the product can be distributed to investors. It also describes the events or circumstances where the Target Market Determination for this financial product may need to be reviewed.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

202507-4690755