High yield returns

High yield - the name says it all

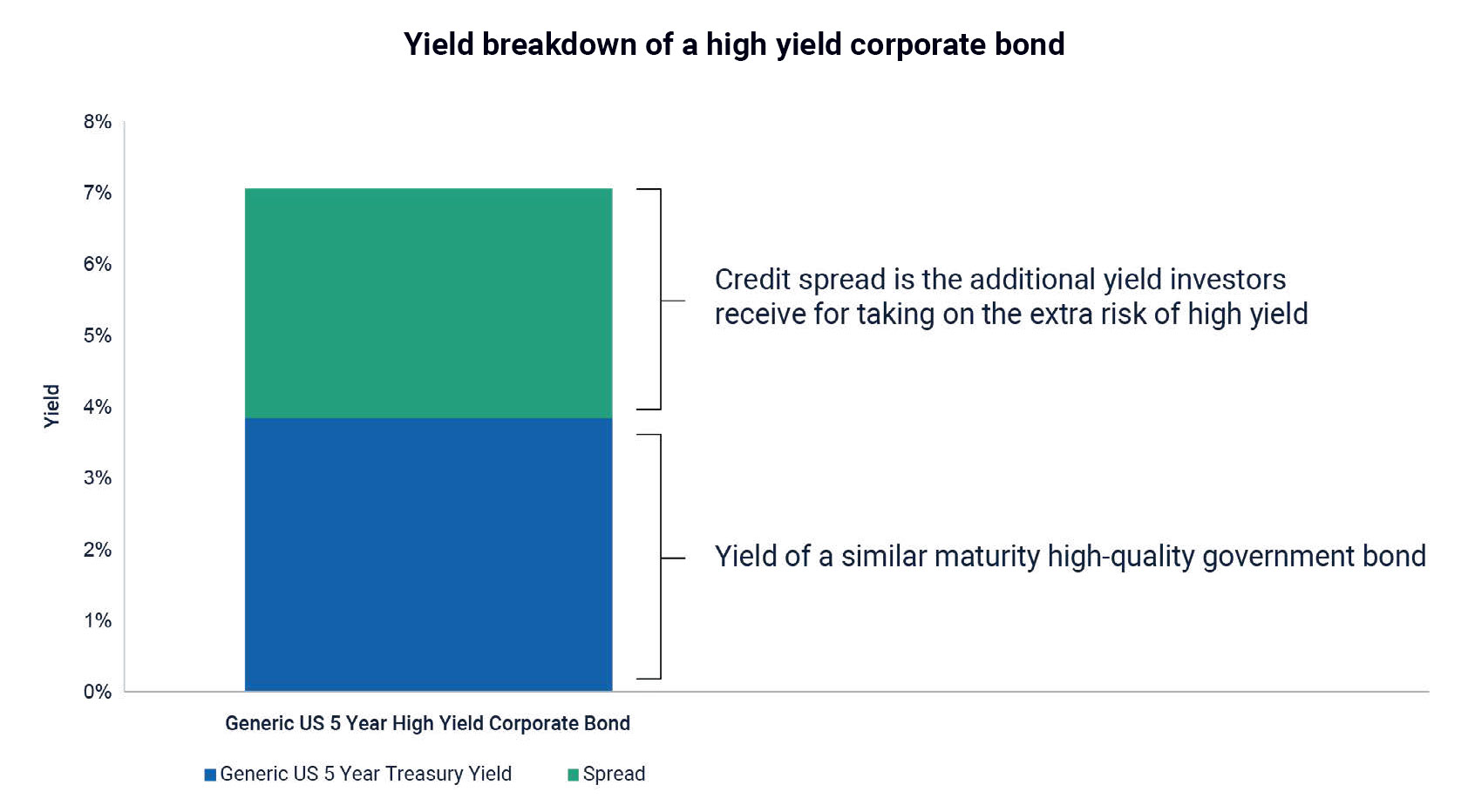

Breaking down a high yield bond

Transcript

Hi, I’m Jennifer Poon from the T. Rowe Price Fixed Income team, and I want to talk about one of the most important concepts in high yield investing – credit spreads.

High yield bonds, as the name suggests, offer higher yields than government or investment-grade bonds. That’s because you’re taking on a bit more credit risk, and the extra yield – called the credit spread – is your compensation for that risk.

A credit spread is the extra yield a company has to pay above a government bond to borrow money. So the riskier the company is, the bigger the spread investors demand as compensation for taking on that extra credit risk.

In high yield, the biggest risk is credit risk – specifically the risk of default.

A default occurs when a company doesn’t meet its debt obligations. That could mean missing a coupon payment, failing to repay the principal at maturity, or restructuring its debt in a way that causes losses to bondholders.

In short, the company doesn’t pay what it promised – and those are permanent losses that can drag on returns.

But the good news is that investors are compensated for that risk by the credit spread. And historically, credit spreads – that extra yield – have more than covered actual default losses. So while the risk is real, the market tends to overprice it, which creates opportunities for disciplined investors.

Defaults do happen in high yield, but they’re not as frequent as many people think. The average default rate in the US high yield market in the last 10 years has been 2.6% per year. The credit spreads over the same period are on average around 4.4%. So that extra yield you earn – has historically been much higher than the actual losses from defaults, leaving a cushion for investors.

I hope this gives you a clearer picture of what you’re really being compensated for in high yield.

For more information on how high yield can help your portfolio, consider reaching out to your financial adviser.

Key takeaways

1. The credit spread

The "credit spread" is the difference in yield between the high yield bond and a government bond of similar maturity.

The information presented is shown for illustrative purposes only. The information is not intended as a recommendation to buy or sell any particular security, and it is not a reliable indicator that results shown will be achieved. A positive yield does not imply a high or positive return.

2. Historical risk premium

Credit spreads have historically more than compensated investors for actual default losses in the market.

Read the complete story

Complete the learning and short quiz to earn CPD points.

New to high yield terms?

Get quick definitions of key concepts to help you navigate the high yield education hub with confidence.

Continue your learning

items Introduction to high yield

Introduction to high yield

Why global high yield?

Looking for income opportunities? This exciting asset class could be a compelling option

Introduction to high yield

Introduction to high yield

High yield is all around us...

You could be surprised by some familiar names

High yield returns

High yield returns

Understanding high yield bond returns

The power of the compounding coupon

Role of high yield

Role of high yield

Comparing high yield to other asset classes

See how high yield stacks up from a risk and return, and volatility perspective

Role of high yield

Role of high yield

Correlations

It behaves more like equities than traditional bonds

Role of high yield

Role of high yield

More ups than downs

See how it's performed during times of market stress

Portfolio construction

Where does global high yield fit in your portfolio?

Risks

Risks

The importance of avoiding defaults

How active management can make a big difference

Risks

Risks

Risks of high yield

Things to consider before investing

T. Rowe Price Global High Income Fund

Exciting companies.

Compelling incomes.

Current yield

7.08%*

*As of 30 September 2025. Past performance is not a guarantee or a reliable indicator of future results. The current yield of the fund reflects the market-weighted average of coupon divided by price per security.

Risks

Fixed income securities are subject to credit risk, liquidity risk, call risk, and interest-rate risk. As interest rates rise, bond prices generally fall. Investments in high yield bonds involve greater risk of price volatility, illiquidity, and default than higher-rated debt securities.

Additional Disclosures

ICE BofA do not accept any liability for any errors or omissions in the indexes or data, and hereby expressly disclaim all warranties of originality, accuracy, completeness timeliness, merchantability and fitness for a particular purpose. No party may rely on any indexes or data contained in this communication. Visit https://www.troweprice.com/en/au/market-data-disclosures for additional legal notices & disclaimers.

202508-4771180