A new survey on retirement spending by T. Rowe Price revealed that many recent retirees who have 401(k)s and/or rollover IRAs have accumulated significant nest eggs, and most say they are faring well, both financially and emotionally. Meanwhile, workers in their 50s who are participating in an employer 401(k) have also accumulated significant assets, but feel more anxious about retirement than those who have already retired.

To learn about the current landscape and help 401(k) plan sponsors and participants, the survey focused on a unique population: new retirees who have 401(k) account balances or rollover IRAs and workers age 50 and older who are 401(k) participants. The survey is based on a national sample of 1,507 retirees who have been in retirement for one to five years and have a rollover IRA or an account balance in their 401(k) plan. It also includes a second sample of 1,030 workers, age 50 and older, who are currently contributing to a 401(k) plan or are eligible to contribute and have a balance of at least $1,000.

Findings among retirees:

- Many have considerable savings: Recent retirees reported median household assets (investable assets plus home equity minus debt) of $473,000, with 48% having $500,000 or more in household assets. Of their investable assets, 38% was in stocks and stock mutual funds, 13% was in asset allocation mutual funds, and 31% was held in cash. More than eight in 10 (82%) of the retirees own real estate with a median of $191,000 in home equity.

- Social Security accounted for the largest portion of their income: 43% of their income came from Social Security. The second largest source came from traditional defined benefit plans (19%), followed by amounts withdrawn from personal savings and investment accounts including IRAs and defined contribution plans (18%).

- Work is part of the picture: 21% are working either part-time (16%) or full-time (4%). Another 14% are retired but looking for work.

- Those with a withdrawal plan are withdrawing close to 4% of their assets annually: 48% of retirees indicated that they have a withdrawal plan, and the median retirement withdrawal among them was 4% of their investable assets within the past 12 months. But the average does mask some extremes, including nearly a quarter who withdrew 8% or more and over a quarter who withdrew only 1%.

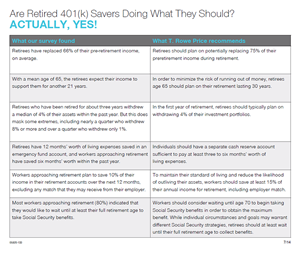

- Living on less: Nearly three years into retirement, retirees report living on 66% of their pre-retirement income on average.

- But that has not translated to dissatisfaction with their lifestyle: 57% report they live as well or better than when they were working. And 85% agree with the statement, "I don't need to spend as much as I did before I retired to be satisfied," including 37% who say this describes them a "great deal." Most (65%) like not spending as much and see it as a new found freedom from "keeping up with the Joneses," with 25% saying this describes them a "great deal."

- They feel satisfied: 89% are somewhat or very satisfied with retirement so far. Additionally, 74% say they are somewhat or much better off financially compared with how their parents lived when they were their age.

- Most are flexible: 60% of the retirees would rather adjust their spending up and down depending on the market to maintain the value of their portfolio rather than maintain the same level of spending year after year, at the expense of potentially diminishing their portfolio.

- But there are exceptions...not everyone is well off: Households of retirees who are not married or living with a partner, are not doing as well as their married counterparts, both financially and emotionally. And women represent a greater proportion of single households than men: 48% of women reside in single households compared with 26% of men. These single households have only a median of $248,000 in investable assets plus home equity minus debt combined (compared with $731,000 for married households). They are more likely to be looking for work (19% vs. 11%), a higher proportion are finding it difficult to live without their preretirement paycheck (36% vs. 27%), more believe that they will run out of money (19% vs. 11%), and fewer are "very satisfied" with their retirement experience (37% vs. 48%).

Findings among workers age 50 and older:

- Workers are more anxious than retirees: A greater percentage of workers believe that they will have to reduce their standard of living compared with the retirees (49% vs. 35%). More workers also believe that they will run out of money (22% vs. 14%). And they are less likely to believe that they will have enough money to pay for health care (49% vs. 70%).

- But most have considerable savings: Workers have accumulated median household assets (investable assets plus home equity minus debt) of $465,000. They are invested less conservatively than their retired counterparts, with 47% of their investable assets in stocks or stock mutual funds, 13% in asset allocation funds, and 23% in cash. Of the workers, 81% own real estate, with a median of $171,000 in home equity.

- They do not plan to use home equity to generate retirement income: 60% do not plan to tap their home equity at all for retirement income, and only 11% plan to use more than half of their home equity.

- High savings rates: The median personal deferral rate for their retirement plan is 10%, not counting any match that they may receive from their employer.

- Confidence that they will save enough: The median minimum they would like to save is $693,000 before they retire and 61% are confident that they will hit that number

- They expect to work longer and have considered delaying retirement: On average, they expect to retire at age 68. Additionally, 43% have considered delaying retirement in the last 12 months.

- Social Security can be delayed: 80% indicated their intent to wait until at least their full retirement age (age 66) to begin collecting Social Security benefits, with 34% willing to take the maximum benefit at age 70. Only 20% indicated their intent to collect Social Security benefits as soon as they become eligible (age 62).

- Job security is a concern: 29% of the workers are somewhat or very concerned that they may lose their jobs in the next 12 months.

Quotes

Aimee DeCamillo, head of T. Rowe Price Retirement Plan Services, Inc.

"For workers approaching retirement, we know there is anxiety and uncertainty as they look ahead and think they can't possibly be prepared for retirement. But this study demonstrates that you can do it. Many people are successfully saving in the private retirement system, and they report that post transition, they are fine. We have an opportunity to share these positive stories with 401(k) savers. We also need to emphasize the important role Social Security plays as the foundation of retirement income for most American households and the strategic advantages of delaying Social Security benefits."

Anne Coveney, senior manager of Thought Leadership at T. Rowe Price

"While we know there are people with little or no retirement savings, our survey suggests that many who participated in a 401(k) are entering retirement with considerable assets. And new retirees are flexible with their spending and report high satisfaction with their retirement so far."

About T. Rowe Price

Founded in 1937, Baltimore-based T. Rowe Price (troweprice.com) is a global investment management organization with $738.4 billion in assets under management as of June 30, 2014. The organization provides a broad array of mutual funds, subadvisory services, and separate account management for individual and institutional investors, retirement plans, and financial intermediaries. The company also offers a variety of sophisticated investment planning and guidance tools. T. Rowe Price's disciplined, risk-aware investment approach focuses on diversification, style consistency, and fundamental research. For more information, visit troweprice.com, Twitter (twitter.com/troweprice), YouTube (youtube.com/trowepricegroup), LinkedIn (linkedin.com/company/t.-rowe-price), or Facebook (fb.com/troweprice).

About the survey

This research is based on online interviews with workers and retirees. This includes 1,030 working adults age 50 or over who are currently contributing to a 401(k) plan or are eligible to contribute and have a balance with their current employer of $1,000 or more. Retirees are represented by 1,507 adults who have retired in the past one to five years and who have a rollover IRA or an account balance in a 401(k) plan. Interviewing was conducted during February 19 - March 3, 2014. Findings in both samples are subject to a margin of error of just under 3%.