March 2021 / INVESTMENT INSIGHTS

Enhancing the T. Rowe Price Glide Paths

Higher equity allocations reflect changes in retirement investing.

Key Insights

- We believe that retirement outcomes can be improved by modestly increasing equity allocations at the front and back ends of the T. Rowe Price glide paths.

- Our research suggests plan sponsors and participants can and will accept modest risk increases at certain points of the glide path to seek better outcomes.

- We are not changing equity allocations in the years immediately before and at retirement, when investors appear to be most sensitive to market volatility.

The T. Rowe Price approach to target date investing has long reflected our view that retirement investors need adequate exposure to growth‑oriented assets. Trends in target date investing—and our continued focus on improving our methodology since we launched our first target date strategies in 2002—have only strengthened this belief.

Accordingly, T. Rowe Price is moving to increase equity exposure modestly at the front and back ends of our glide paths, while leaving equity allocations unchanged in the years immediately before and at retirement. These changes began in April 2020, are being phased in over a two‑year period, and currently are expected to be completed in the second quarter of 2022, depending on market conditions.

The modifications to our glide paths reflect T. Rowe Price’s ongoing analysis of the behavior and preferences of both retirement investors and defined contribution (DC) plan sponsors, as well as recent enhancements to our glide path modeling process, which have given us increased confidence that participants are willing and able to accept modest increases in short‑term market risk at points before and after retirement in an effort to achieve better outcomes during retirement.

Over the past two decades, T. Rowe Price has made a substantial investment in the design and assessment of our target date glide paths. Our process seeks a deep understanding of both markets and investor behavior and how those elements potentially may interact over a wide range of market and economic cycles.

Defining the objective is the first step of our process. The objective is informed by the relative focus that a DC plan sponsor places on the trade‑offs between key preferences, such as consumption versus wealth sustainability and a lifetime planning horizon versus a primary focus on the few years around retirement.

T. Rowe Price currently offers two different glide paths because we recognize that different plan sponsors may have different objectives for their target date offerings. The primary objective of the Retirement Glide Path is to help support lifetime income over a lengthy retirement. The primary objective of the Target Glide Path is to seek to limit balance variability around retirement, with a secondary focus on supporting income during retirement.

Although the two glide paths take slightly different approaches, both are built with the view that an adequate retirement strategy must have some focus on income replacement. For example, while the Target Glide Path places a somewhat greater relative emphasis on seeking to mitigate market risk around retirement, it still maintains a substantial allocation to equities and other growth‑oriented assets in an effort to help support income needs during retirement.

An Increased Focus on Longevity Risk

The changes we are making to our glide paths are supported by an evolution in plan sponsor and participant preferences. We continue to see both groups increase their focus on long‑term income sustainability and place a higher priority on seeking strategies to manage longevity risk.

The reality is many investors face powerful head winds to achieving a comfortable retirement. As the retirement landscape shifts away from defined benefit pensions, future retirees will need to rely more on other income sources, such as their defined contribution plans.

In addition, life expectancies have risen over the past 20 years, meaning today’s retirement investors are likely to need an income stream that lasts longer than their currently anticipated time horizons.

- According to the Centers for Disease Control and Prevention (CDC), the conditional average life expectancy of U.S. individuals age 65 increased by two years between 2000 and 2018, from 82.5 years to 84.5 years.1

- CDC data also indicate that there is a relatively high probability of individuals living into their 90s, meaning they’ll need their retirement savings to support consumption for multiple decades.2

Moreover, it is widely understood that many retirement investors are chronically underfunded—they simply aren’t saving enough to meet their expected income needs in retirement.

Reflecting these sobering realities, our work with DC plan sponsors shows that many are now overwhelmingly focused on longevity risk as their top priority. Many plans also now prefer that their qualified default investment alternatives be designed to meet the needs of their full, active participant populations.

Behavioral changes in the DC space have further strengthened the case for higher long‑term equity exposure, in our view. Until fairly recently, many DC plan sponsors assumed that participants would exit their plans at or soon after retirement, rolling their balances over into individual retirement accounts (IRAs). However, data show that retirees now are increasingly more likely to retain assets in their DC plans, while plan sponsors have grown more interested in keeping them there:

- T. Rowe Price’s recordkeeping data show that in 2019 over 56% of DC participant balances at time of retirement were still invested in plan accounts one year after retirement, up from 55.2% in 2018 and only 48.4% in 2016.3

- A 2020 T. Rowe Price survey found that 55% of larger plan sponsors either preferred to keep retiring participants in their plan or were currently reconsidering their position on the matter; only 7% reported having an explicit preference that retiring participants roll their balances over to IRAs.4

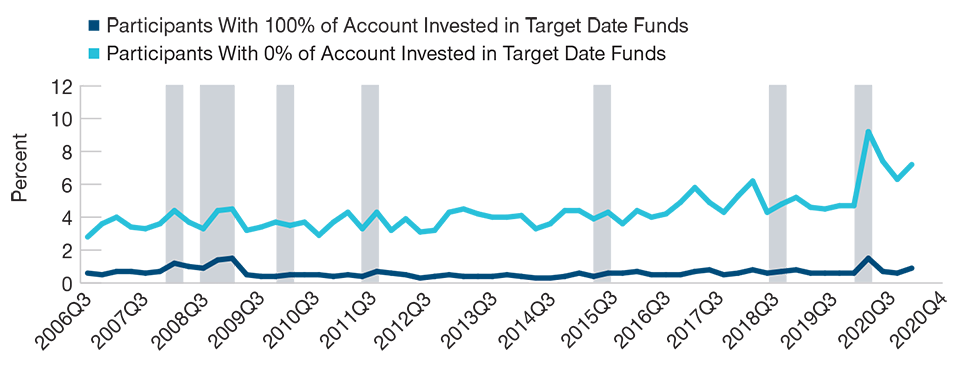

Our insights into participant behavior, as well as improvements in our modeling framework, also give us confidence that most target date participants are less sensitive to market volatility than may be commonly believed. Historically, target date investors have been much less likely than other investors to make allocation changes during market downturns (Figure 1). Importantly, this trend holds for young investors as well as for those approaching and in retirement.

As a recent example, 2020 saw a significant amount of market volatility, both upside and downside, related to the coronavirus and its economic impacts. Equity markets went through a swift and short bear market, followed by a speedy rebound and then a rally at the end of the year. Importantly, our data show that the vast majority of target date investors stayed the course with their investments and thus were likely to end the year with higher account balances than when they began.

Indeed, the target date investors in our data were eight times more likely to keep their investment allocations intact compared with non-target date investors. In our view, this comparison confirms that target date investors are using these investments appropriately for the long haul. To us, the data suggest that modestly higher exposure to market volatility is an acceptable trade‑off for participants as they seek to achieve better long‑term outcomes in retirement.

(Fig. 1) Target Date Participants Less Likely to React to Short‑Term Volatility

Percentage of investors who made an allocation change during quarter1

Third quarter 2006 through fourth quarter 2020

Source: T. Rowe Price.

1 Shading represents quarters in which the S&P 500 Index dropped by more than 5%. Based on quarterlydata for all DC plan participants in retirement plans administered by T. Rowe Price.

Addressing Today’s Retirement Challenges

The demographic and behavioral trends described above have only reinforced our view that achieving adequate portfolio growth is critical for most retirement investors. We also believe that the potential benefits of a growth‑oriented strategy are likely to outweigh the potential negative impacts of large market declines close to or soon after retirement.5

Historically, the compounding of the equity risk premium—the additional return on stocks relative to bonds—has led to meaningful differences in investment outcomes. Although equities have been more volatile than bond and other fixed income assets over shorter periods, the higher long‑term returns associated with equities have facilitated wealth accumulation over the long term.

T. Rowe Price’s Glide Path Approach

We believe an effective approach to life-cycle investing must rely upon a deep understanding of both markets and investors, reflecting how those elements potentially can evolve and interact over time horizons spanning several decades and a wide range of market and economic cycles.

In order to properly assess the impact and interaction of these elements, we employ a structural model to help us evaluate and design glide paths. The primary benefit of this model is that it is intended to ensure consistency of our approach.

We recognize that individuals are skillful at using intuition and judgment to solve complex problems, but they are not as effective applying these skills consistently or at scale. We believe our structural model allows us to apply our insights consistently across the range of glide path problems that we seek to solve.

Our evaluation framework is a utility satisfaction model that incorporates key variables that influence glide path design. Accounting for utility gives us the capability to assess and score the level of satisfaction different outcomes provide relative to plan sponsor and participant preferences and objectives.

The first step in understanding how we apply our framework is to understand the primary factors that can influence glide path design:

Capital Markets: These are the assumptions about potential asset class returns that are informed by variables such as economic growth, inflation, and interest rates. The capital markets factor is incorporated through an economic model of the economy and capital markets.

Demographics: These assumptions represent how we model the cash flows—savings and spending needs—that impact glide path design. They include variables such as earnings, savings rates, employer matching contributions, projected Social Security benefits, and assumptions about life expectancy. These inputs are captured using a behavioral model of participant demographic factors. For our proprietary solutions, demographic assumptions are seeded with information from the T. Rowe Price DC recordkeeping platform.

Behavioral Preferences: Our model also incorporates a range of behavioral preferences that allow the model to account for participant and plan sponsor attitudes toward risk, balance depletion, planning horizons, and investment goals. These inputs can be divided into two categories: innate preferences and objectives. Innate preferences are ingrained in individual investors—for example, how do they feel about risk? Objectives are determined by plan sponsors on behalf of participants and are related to investment goals and planning horizons in retirement.

Through the use of Monte Carlo simulation, we use our economic and behavioral models to generate thousands of different potential economic and demographic scenarios.

As discussed previously, defining the objective is the first step in our process. Once the objective is set, we calibrate the behavioral preferences, investment goal, and planning horizon to reflect the objective we are solving. The economic and behavioral models generate thousands of different scenarios. We then use our utility satisfaction model to identify the glide path that robustly maximizes potential utility satisfaction as defined by the behavioral preferences, the plan sponsor objective, and the demographic inputs.

The final step of our process incorporates the judgment of our target date team. While our models are effective at applying the themes and insights of the team consistently across a population of investors, our depth and experience as an investment manager and recordkeeper provide critical balance to our process as we seek to ensure that our model is capturing the potential benefits of our insights in the manner intended and in a way that reflects the needs of our clients. We believe this feedback loop is essential to building and maintaining a robust glide path construction process.

IMPORTANT INFORMATION

This material is being furnished for general informational purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, and prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

USA—Issued in the USA by T. Rowe Price Associates, Inc., 100 East Pratt Street, Baltimore, MD, 21202, which is regulated by the U.S. Securities and Exchange Commission. For Institutional Investors only.

© 2023 T. Rowe Price. All rights reserved. T. ROWE PRICE, INVEST WITH CONFIDENCE, and the bighorn sheep design are, collectively and/or apart, trademarks or registered trademarks of T. Rowe Price Group, Inc.

10 February 2021 / RETIREMENT INSIGHTS

Kim DeDominicis is a portfolio manager of the target date strategies in the Multi-Asset Division. She also leads the College Savings Plan investment efforts. Kim is a vice president of T. Rowe Price Group, Inc., T. Rowe Price Trust Company, and T. Rowe Price Associates, Inc.

Andrew Jacobs van Merlen is a portfolio manager and co-portfolio manager for the target date strategies in the Multi-Asset Division. Andrew is a vice president of T. Rowe Price Group, Inc., T. Rowe Price Trust Company, T. Rowe Price Associates, Inc., and T. Rowe Price International Ltd.

Wyatt Lee is the head of Target Date Strategies in the Global Multi-Asset Division. He is co-manager of target date portfolios. Wyatt also is a member of the firm's Asset Allocation and Multi-Asset Steering Committees. Wyatt is a vice president of T. Rowe Price Group, Inc., T. Rowe Price Trust Company, and T. Rowe Price Associates, Inc.