January 2023 / MARKETS & ECONOMY

Global Markets Monthly Update

Keep up-to-date on our views on developments in global capital markets.

Key Insights

- Global markets rallied to start the year, boosted by signs of falling inflation and China’s relaxation of pandemic restrictions.

- Shares in China led the gains among major markets, but European shares also performed especially well as the Continent’s energy supplies held up better than many expected.

- Bonds also saw gains as investors wagered that the Federal Reserve was nearer the end of its rate hiking cycle than it had appeared.

U.S.

Stocks recorded their best January performance since 2019, as investors welcomed data suggesting that the Federal Reserve might be able to tame inflation without causing a recession. As inflation and interest rate fears moderated, making anticipated future earnings more attractive to investors, growth stocks performed best. Rebounds in Tesla and Amazon.com helped consumer discretionary shares within the S&P 500 Index record a total return (including dividends) of 15.0%, while a bounce in the shares of Facebook parent Meta Platforms contributed to a gain of 14.5% in communication services stocks. As investors pivoted toward taking on more risk, the typically defensive utilities, health care, and consumer staples sectors recorded small losses.

Bonds also recorded good returns as longer-term yields decreased. The “risk on” turn in the markets was reflected in tightening corporate credit spreads, or the extra yield demanded by investors for investing in credit-sensitive bonds rather than Treasuries with similar maturities.

Services Sector Activity Contracts for First Time Since Early in the Pandemic

Stocks began to build momentum on January 6, as investors seemed to react positively to a stream of signals indicating slowing growth and inflation pressures. The Labor Department reported that job growth slowed in December to its lowest level in two years, if somewhat less than expected. The year-over-year growth in average hourly earnings also fell to its lowest level (4.6%) since September 2021. Even more impactful may have been the release of the Institute for Supply Management’s gauge of services sector activity, which surprised investors by falling into contraction territory for the first time since early in the pandemic.

Much of the data released over the remainder of the month confirmed that consumers were growing more cautious and less willing or able to pay higher prices. Most notable may have been a 1.1% drop in December retail sales, which was roughly triple consensus estimates. A decline in sales at gas stations was partly at work, but Americans pulled back on sales of furniture, electronics, and other discretionary items. November sales data were also revised lower.

Meanwhile, headline consumer prices ticked lower in December, bringing the year-on-year gain to 6.5%—still well above the Federal Reserve’s long-term 2% inflation target but the slowest pace since October 2021. Producer prices fell 0.5% in December, the biggest drop since early in the pandemic, raising hopes that further retail price cuts were in the pipeline.

Central Bank Cautions That More Work Lies Ahead

Federal Reserve officials cautioned repeatedly that work remained in taming inflation, however, and that additional rate hikes lie ahead. Fed Chair Jerome Powell and others cited continuing tightness in the labor market as a particular concern, and the month brought little data to suggest firms’ competition for workers was easing substantially. Weekly jobless claims fell to their lowest level since the previous April, and roughly two jobs remained open for every person seeking work—in comparison, an average of roughly 2.2 workers have been available for every open job over the postwar period.

The month’s gains may have also been restrained by a steep slowdown in corporate earnings, which had spiked over the past two years. As of the end of the month, analysts polled by FactSet were anticipating that overall earnings for the S&P 500 would have declined by 5.0% in the final quarter of 2022 versus the year before, marking the first contraction since late 2020.

Europe

Investors bid shares in Europe sharply higher in January, taking their cue from falling energy prices, slowing inflation, encouraging economic data, and optimism around China’s reopening. These developments helped to overcome concerns about the pace of monetary policy tightening. In local currency terms, the pan-European STOXX Europe 600 Index ended more than 6.6% higher. Germany’s Xetra DAX Index, Italy’s FTSE MIB Index, France’s CAC 40 Index, and the UK’s FTSE 100 Index also climbed.

ECB Policymakers Press for Higher Rates

European Central Bank (ECB) policymakers kept up the pressure for more significant interest rate increases at forthcoming meetings, even as inflation slowed and the economy skirted a recession. The minutes of the ECB’s December meeting—where the Governing Council raised key rates by half a percentage point—showed that a “large number” of members wanted to raise borrowing costs by 0.75 percentage point. These policymakers only backed the smaller increase once the remaining central bank governors agreed to maintain a hawkish stance.

In subsequent interviews, policymakers indicated that more large rate hikes were likely in February and March. At the World Economic Forum in Davos, Switzerland, ECB President Christine Lagarde remarked that “inflation, by all accounts, however you look at it, is way too high” and pledged that policymakers were “taking all the measures that we have to” in order to bring it back to 2%. She dismissed market speculation that a fall in energy prices would allow policymakers to slow the pace of monetary policy tightening.

Eurozone Inflation Falls Below 10%; Economy Grows in Fourth Quarter

A decline in energy price increases helped push eurozone inflation below 10% in December. Consumer prices rose 9.2% year over year, below a FactSet consensus estimate of 9.7%. Even so, core inflation—which excludes volatile food, energy, alcohol, and tobacco prices—quickened to 5.2%.

The eurozone economy grew 0.1% in the fourth quarter. Surveys of purchasing managers in manufacturing and services suggested that business activity in the bloc unexpectedly stabilized in January after contracting for six months. The European Commission’s business and consumer surveys also indicated that confidence strengthened in January.

UK Inflation Slows for Second Month; BoE’s Bailey Hints Rates Could Peak at 4.5%

The annualized rate of inflation in the UK slowed for a second consecutive month in December. The consumer price index (CPI) slipped to 10.5%. Unemployment rose slightly, remaining close to a record low in the three months to November, while average wage inflation (excluding bonuses) was running at an annualized pace of 6.4%. In addition, the UK economy grew 0.1% sequentially in November, beating a consensus forecast for a 0.2% contraction in a FactSet survey of economists.

Bank of England (BoE) Governor Andrew Bailey said in a newspaper interview that a second consecutive month of slowing inflation could be “the beginning of a sign that a corner has been turned.” He also suggested that financial market expectations that rates currently at 3.5% would peak at 4.5% was not dissimilar to the bank’s view. Bailey said he still expected a “long, but shallow” recession in the UK this year.

Japan

Japanese equities advanced in January, with the MSCI Japan Index up 4.7% in local currency terms. Sentiment was supported by the prospect of China’s reopening boosting the global economy and hopes that the major central banks would slow the pace of their rate hikes amid some signs of waning inflationary pressures. Investors’ focus was on the Bank of Japan (BoJ), which left its policy stance unchanged at its January meeting, having surprised markets in December by tweaking its yield curve control framework by raising the cap on the Japanese government bond (JGB) yield from 0.25% to 0.50%.

The BoJ continued to conduct unscheduled bond-buying operations to keep the 10-year JGB yield around its new 0.50% cap, roughly the level at which it ended the month, up from 0.42%. Pressure on the cap reflected investors’ expectations that the BoJ would increasingly pivot away from its ultra-loose monetary policy stance. The yen strengthened, to around JPY 130.10 against the U.S. dollar, from about JPY 131.13 at the end of December.

No Change in BoJ Monetary Policy; Inflation Forecasts Raised

The BoJ said that medium- to long-term inflation expectations had risen, albeit at a moderate pace relative to short‑term ones, and it raised its forecasts for the core consumer price index for fiscal years 2022 and 2023, which had also been widely anticipated. The central bank noted that risks to inflation are skewed to the upside, leaving open the possibility that forecasts would be revised up at the time of the next release in April. Japan’s core CPI rose 4% year on year in December, a 41-year high, as companies passed rising costs onto consumers. Producer prices also surged over the same period.

Kishida Urges Companies to Deliver Above-Inflation Pay Rises

With nominal wage growth in November well below consensus expectations, Prime Minister Fumio Kishida urged Japanese companies to deliver above‑inflation pay rises. He warned of the risks associated with inflation outpacing wage growth, including the erosion of households’ purchasing power in an environment of low economic growth. Raising pay is a key pillar of the government’s “New Capitalism” agenda to better distribute the fruits of growth.

Private Sector Returns to Growth

Japan’s private sector activity returned to growth in January, but there remained a divergence between services and manufacturing, according to the latest Purchasing Managers’ Index (PMI) data. Activity in the services sector expanded moderately, with the government’s travel subsidy program and the relaxation of COVID restrictions providing a tailwind. Conversely, the health of the manufacturing sector deteriorated, as subdued demand weighed on output and new orders.

China

Chinese equities rallied for the first three weeks of January, with markets in mainland China closed from January 21 to January 30 for the Lunar New Year holiday. Reports of better-than‑expected economic data boosted investor sentiment as domestic activity recovered after Beijing eased pandemic restrictions. The MSCI China Index gained 11.8% while the China A Onshore Index advanced 10.4% in U.S. dollar terms.

China’s gross domestic product failed to grow in the fourth quarter and expanded 3.0% for the full year. The full-year growth pace missed the official target of around 5.5% set last March. Still, the reading surpassed economists’ forecasts after Beijing abandoned its stringent pandemic restrictions and rolled out a slew of pro-growth policies toward the end of 2022. For 2023, economists predict that China’s growth rate will recover to close to 5% as infections subside and domestic demand accelerates.

In early January, hopes of further support for property developers rose following news that financial regulators may ease the stringent “three red lines” policy, Bloomberg reported, citing unnamed sources. The policy featured prominently in the government’s crackdown on the real estate sector in 2020 and consisted of a series of debt thresholds aimed at curbing leverage among developers seeking to borrow more. China is also considering a nationwide cap between 2.0% to 2.5% on real estate commissions to boost demand. Separately, the People’s Bank of China announced that first-time homebuyers would be offered lower mortgage rates if new home prices fall for three consecutive months. The changes mark a significant shift in China’s real estate policy as Beijing attempts to restore confidence in a sector that accounts for almost a quarter of the nation’s economy.

Meanwhile, China’s domestic activity picked up significantly during the weeklong holiday at the end of the month, fueling optimism about a faster‑than-anticipated economic recovery as people enjoyed the break from pandemic restrictions. Approximately 95.9 million trips were taken via road, rail, air, and waterways in the first four days of the holiday, or a daily average of 24 million trips compared with 18.6 million over the 2022 break, according to Ministry of Transport data. Total box office sales also outpaced the prior year, while outbound air tickets more than quadrupled for the full year and hotel bookings doubled.

Economic Data Point to Softer Momentum

On the trade front, China’s exports fell 9.9% in December from a year ago as global demand softened and rising infections disrupted activity after the government rolled back pandemic restrictions. Imports fell a better-than‑expected 7.5%. The official PMI reports for manufacturing and nonmanufacturing weakened in December. The composite PMI fell to 42.6 from 47.1 the previous month, marking the biggest decline since February 2020, before the coronavirus outbreak.

However, China’s inflation gained momentum, rising 1.8% in December. Core inflation, which excludes food and energy prices, picked up slightly after remaining unchanged for three consecutive months.

Other Key Markets

Hungary Keeps Pace With Broad Emerging Markets

Stocks in Hungary, as measured by MSCI, returned 7.91%, as did the MSCI Emerging Markets Index.

Toward the end of the month, Hungary’s central bank held its regularly scheduled policy meeting and decided to leave its base interest rate at 13.0%. Policymakers also decided to leave the overnight collateralized lending rate at 25.0%. This interest rate is considered the upper limit of an interest rate “corridor” for the base rate. The lower limit of the corridor is the overnight deposit rate, which remained at 12.5%.

However, according to T. Rowe Price credit analyst Ivan Morozov, the outcome of the meeting was hawkish, as policymakers decided to raise the reserve requirement rate to 10% from 5% and to introduce weekly discount bill auctions starting February 1. Both of these measures are intended to drain liquidity from the banking system and the economy, which is struggling with an inflation rate near 25%. Based on comments from Deputy Governor Barnabas Virag—that monetary policy needs to be driven by patience—and on the post-meeting statement, in which policymakers claim that it may be “necessary to maintain tight monetary conditions over a prolonged period,” Morozov believes that the central bank is in no hurry to cut rates.

Also toward the end of the month, two of the major credit agencies revised their assessments of Hungary. On January 20, Fitch changed its outlook on Hungary’s BBB rating from “stable” to “negative,” citing a tough external environment and uncertainty regarding the flow of funds from the European Union (EU) as the main catalysts for the change. Morozov acknowledges and agrees that higher energy costs following Russia’s invasion of Ukraine—given that Hungary relies greatly on Russian energy exports—have pushed Hungary’s current account into a significant deficit situation and that uncertainty regarding the flow of EU funds translates into uncertainty about how Hungary would fund that deficit.

Just one week later, S&P downgraded its credit rating on Hungary from BBB to BBB-, citing the same reasons. The timing, however, was sooner than Morozov expected: S&P had reduced its outlook to negative in August, so Hungary has not had much time to address S&P’s credit concerns. Despite these actions, Morozov notes that Hungary still has an investment‑grade rating and believes that possible downgrades to below investment grade are not imminent.

Brazilian Stocks Gain Despite Political Turbulence

Stocks in Brazil, as measured by MSCI, returned 6.99% but modestly underperformed the MSCI Emerging Markets Index.

On January 1, Luiz Inácio Lula da Silva (Lula) took office as president. His inauguration speech sounded very similar to one of his campaign speeches, though he spent more time playing up the negative legacy that he believes he inherited from outgoing President Jair Bolsonaro. Although Lula had a narrow election victory over Bolsonaro, his speech did not seem aimed at unifying the divided electorate. On the other hand, Fernando Haddad, who was sworn in as finance minister, delivered a moderate speech in which he expressed interest in funding important government programs without creating an unsustainable debt situation. However, Haddad failed to provide firm details on how to find that balance.

Just one week later—in a scene reminiscent of January 6, 2021, at the U.S. Capitol—Bolsonaro’s supporters broke through security lines at a demonstration in Brasilia and temporarily invaded Congress, the supreme court, and the president’s office, though not the president’s residence. While security forces removed the demonstrators and made hundreds of arrests, T. Rowe Price sovereign analyst Richard Hall believes that this demonstrates the degree of rejection that President Lula is facing from a sizable portion of the population. While there will be investigations and additional fallout in terms of identifying financiers and supporters of the protests and riots, Hall believes that these events will ultimately just be a temporary shock to the financial markets. He believes Lula’s economic and fiscal policies are likely to have a greater impact over time.

Indeed, a few days thereafter, Haddad announced a number of fiscal measures intended to reduce the government’s budget deficit. According to Hall, this fiscal package is not overwhelming. It relies heavily on the revenue side, particularly temporary tax measures. Haddad did announce some plans for spending cuts, but details were lacking. Based on Haddad’s estimates, all of these proposed measures should be sufficient to balance the budget in 2023. However, Haddad stated that he thought a deficit of 0.5% to 1.0% of gross domestic product was more likely to be the result, due to expectations for spending pressures to emerge this year.

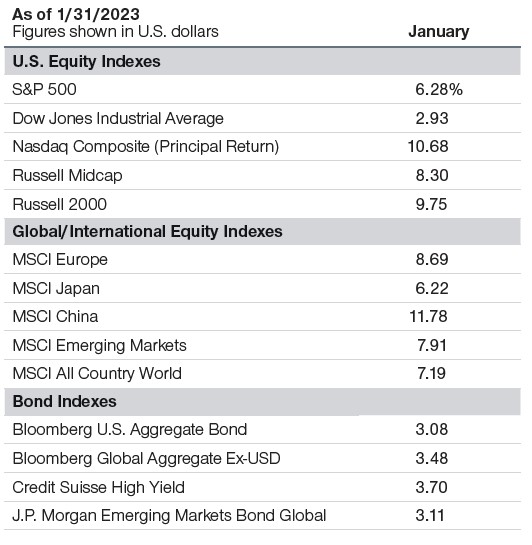

Major Index Returns

Total returns unless noted

Past performance is not a reliable indicator of future performance.

Note: Returns are for the periods ended January 31, 2023. The returns include dividends and interset income based on data supplied by third-party provider RIMES and compiled by T. Rowe Price, except for the Nasdaq Composite Index, whose return is principal only.

Sources: Standard & Poor's, LSE Group, Bloomberg Index Services Limited, MSCI, Credit Suisse, Dow Jones, and J.P. Morgan (see Additional Disclosures).

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date written and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.