December 2023 / GLOBAL MARKET OUTLOOK

Australia Market Outlook: Challenges But Also Opportunities

Key Insights

- We expect a sluggish economy in 2024, due to weak global growth and the lagged effects of RBA tightening. Wage inflation remains a key issue for investors.

- We view Australia as being well-positioned for the new global investment regime, with good long-term opportunities even if the short-term remains challenging.

- We continue to maintain a defensive posture as we expect quality, defensive and growth companies to benefit as their earnings could prove more resilient in 2024.

With per capita GDP falling, the Australian economy is well and truly into the slowdown phase, though high post-Covid immigration numbers have been enough to prevent recession. Australia is entering the second phase in the battle against inflation in which the RBA has been lagging behind the US Fed. The easy wins against inflation have been made and hard yards lie ahead in moving from around 5% inflation closer to 2-3%. You can’t add between 500,000-600,000 people in a single year without adding to inflation pressures. Net immigration in 2023 is adding a staggering 2.0%+ to Australia population, well up on 2022. As in a number of other Developed Markets, wage inflation is still increasing in Australia. It is likely to be one of the key issues investors should watch most closely in 2024, particularly given the parlous state of Australia’s productivity performance.

There has been some good inflation news in the form of lower food price inflation, especially set against earlier concerns over the prices of wheat, corn and fertilizer due to the Russia-Ukraine war. Nevertheless, progress towards the RBA’s inflation target (2-3%) expected by late 2025 is likely to be slow. It may be well into 2026 rather than late 2025 before the target is reached. We were not surprised when the RBA raised the cash rate in November, as the board settled on a rate hike amid the risk of not achieving the inflation target by end-2025 and an accompanying risk of a rise in inflation expectations.

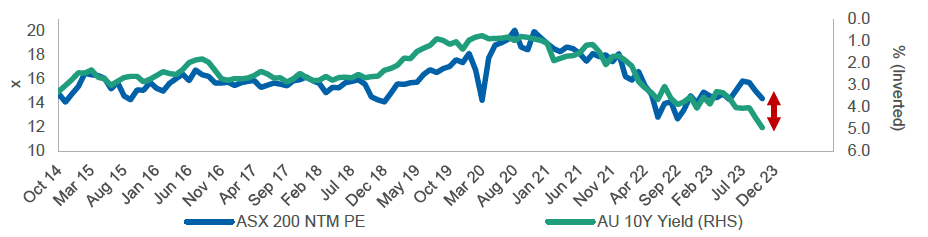

Governor Bullock said later in a speech to Australian business economists that there is a “sizeable demand-driven element to inflation,” and that capacity pressures remain evident, indicating the probability of one or more interest rate hikes in 2024. As a result, Australian 10 year government bond yields, which are forward looking, rose from a 4.0% to 4.25% range in the US summer to a peak of 4.9% in late October, before falling back to around 4.40% in November.

Where is Australia in the business cycle?

We expect a sluggish Australian economy in 2024, reflecting weaker global growth and the lagged effects of past RBA tightening, where the cash rate has risen from 0.1% in April 2022 to 4.35% in November. We are currently experiencing the last 30 to 40 per cent of the rollover of fixed rate mortgages, which will further subdue activity in the residential property market. Debt service ratios for households have risen sharply in Australia due to the higher share of variable rate mortgages. Some respite might come with the Stage Three tax cuts from July 1, 2024, which the Labor government has promised to implement. With an increase in the top tax bracket from AUD180,000 to AUD200,000 plus a reduction in the main marginal tax rate from 32.5% to 30%, the benefits go largely to the highest income bracket households. As such, their multiplier impact on consumer spending may be moderate.

Already halfway through its first term, the Albanese government will need to focus on the rising cost of living with greater urgency following a May 2023 budget that contained no new policies to lower inflation. There is little for Australians to get excited about on the domestic growth front in 2024. Despite a slowing global economy in 2023, commodity prices have held up fairly well, better than many had expected in January. The external sector has once again provided some support to Australia at a time of need. But with most regions expected to see slower GDP growth in 2024, commodity prices may currently be close to the top of the range. Further material support for the Australian economy from commodities in FY24 thus seems rather unlikely.

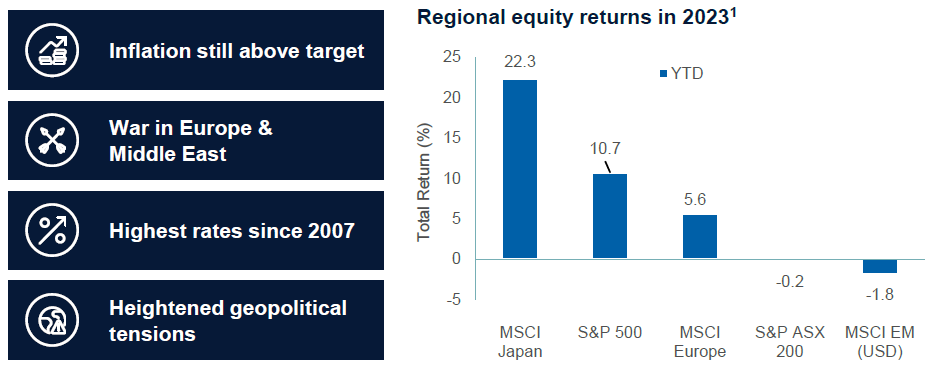

Equity investors are becoming more cautious globally

(Fig. 1) Many challenges remain

As of October 31, 2023.

1 Local currency returns.

Past performance is not a reliable indicator of future performance.

Source: Factset. Financial data and analytics provider FactSet. Copyright 2023 FactSet. All Rights Reserved.

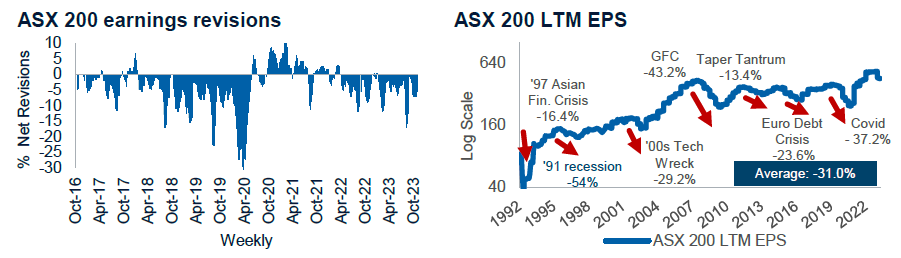

Sluggish economy + rising costs = earnings retreat?

Turning to the outlook for earnings, most forecasts in 2024 are for a decline of 5% to 10%. In our view, the outturn will likely be closer to 10% than 5%. Even then, risk is skewed more to the downside around this consensus forecast decline. Our concern over earnings is a general one. We ask every company that we speak to “What are you doing with prices?” and “What wages pressures are you facing?” And the consistent message we have been receiving is that while input prices and unit wage costs are rising by around 5% to 6%, it is challenging to increase product prices by as much, implying an ongoing squeeze on profit margins and increased earnings risk.

Mining and banking are two sectors that are important for ASX 200 profits. Both have clearly underperformed, with first half profit declines recently reported for the major banks, including Westpac, NAB and Macquarie. Revenues are flat to down and costs are up, and this squeeze is likely to continue into 2024. There is also growing pressure on consumer stocks, especially those where consumer spending is tied to housing demand, such as Harvey Norman.

In the mining sector, energy prices have given back much of their summer gains with Brent oil falling from its early September peak of USD92 per barrel to USD80 per barrel, or around late-July levels. Of course, in terms of individual commodity importance to Australia and the terms of trade, iron ore has no equal. Iron ore prices have been broadly flat at around USD120 per tonne in mid-September, having soared from USD105 per tonne in August, on expectations of further measures from the Chinese authorities to support the Chinese economy. Among metals, we have seen a steep fall in lithium prices due to oversupply and slowing EV demand combined with a sharp rise in mining costs pressuring margins. Notwithstanding this near-term cyclical weakness, we think that the medium- to longer-term outlook for lithium remains very positive, driven by the world’s energy transition to a low carbon intensive economy.

Given Beijing’s increased determination to underpin around 5% GDP growth in 2024, we are comfortable with our view that the current historically high iron ore price should stay relatively firm in 2024. Following the latest policy easing steps in China, the price of iron ore surged to around USD130 per tonne, the highest level since March 2023 when the Chinese economy was widely expected to rebound strongly after the pandemic. In turn, this suggests that the outlook for the Australian commodities sector overall in 2024 is relatively benign, though major gains from current price levels are not expected.

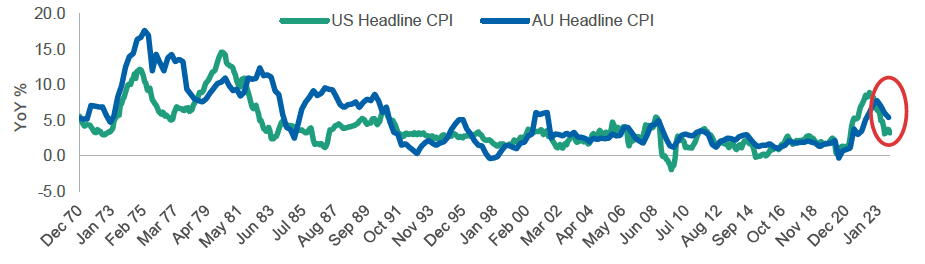

Have we won the inflation battle?

(Fig. 2) Consumer price inflation (year-on-year %)

As of October 31, 2023

YoY: Year on year.

CPI: Consumer Price Index.

Source: Bloomberg Finance L.P.

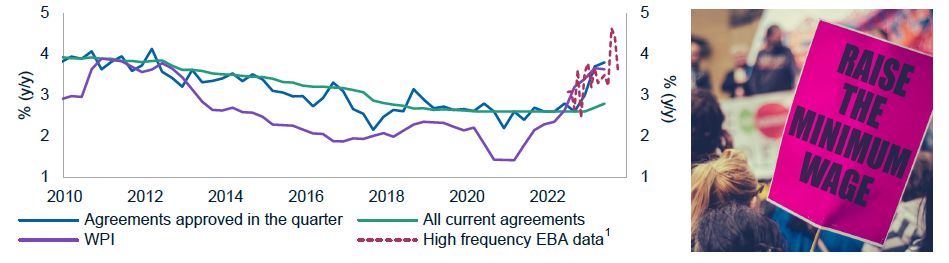

Wage inflation will be key

(Fig. 3) Enterprise bargaining agreements (EBAs) vs Wage Price Index (WPI)

As of September 1, 2023.

Source: Jarden, 1 FWC fortnightly EBA data, average wage increase weighted by employees covered.

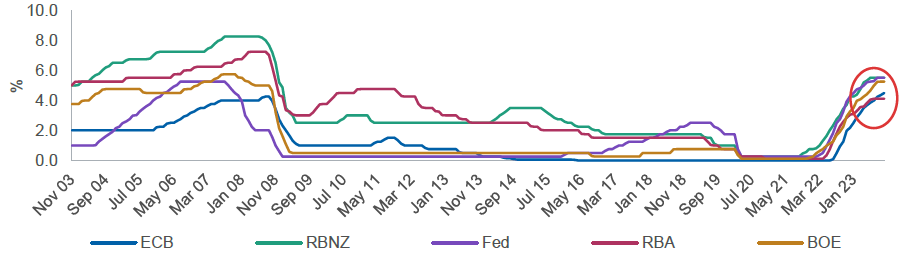

The RBA needs to play catch up

(Fig. 4) Major central bank policy rates

As of October 31, 2023.

Source: FactSet data. Financial data and analytics provider FactSet. Copyright 2023 FactSet. All Rights Reserved.

Market outlook

Investors are increasingly pricing in “peak rates” in many economies. While this makes some sense given progress in reducing inflation, the key issue for markets is “How long are higher rates needed to slow growth and get inflation close to central bank targets, typically around 2.0 per cent?” We think there is still a good deal of uncertainty over this issue. Labour markets in developed economies, including Australia, still appear too tight for comfort. They may be inconsistent with reaching inflation targets within a reasonable time frame.

The latter will most likely require growth to slow further and unemployment to rise. Resilience in economic activity and employment in 2023, while supporting equity markets, paradoxically creates the risk of a nastier downturn in 2024, forcing central banks to disappoint market expectations of interest rate cuts. The collateral damage from sustained high interest rates will include corporate earnings and we expect to see further downgrades in 2024. Whether or not we experience a mild recession or soft landing next year, it is highly likely that we will suffer a sharper fall in corporate profits as economies continue to gradually lose momentum.

The markets’ focus has changed to earnings risk from valuation risk. Cracks in consensus earnings expectation have started to appear in various sectors. We therefore continue to maintain a defensive posture in the portfolio whilst also looking for opportunities in oversold growth names. We expect the more cyclical parts of the Australian share market to come under greater earnings pressure in 2024, which should see quality, defensive and growth companies benefit as their earnings could prove more resilient.

Fortunately, we believe that Australia is relatively well-positioned for the new global investment regime that is unfolding. There are many good long-term investment opportunities even if the short-term macro environment remains challenging. We remain cautious toward businesses with low pricing power, those with significant cyclical exposure or that are vulnerable to higher yields, and the more extreme growth, long-duration stocks. We have more confidence in some of the GARP names with strong fundamentals, in quality, reasonably-valued defensives with pricing power and in defensives that are not well-owned. We are also encouraged by the recent improvement in Australia- China relations following Prime Minister Anthony Albanese’s visit to Beijing, which reached an agreement to review and likely remove China’s punishing import tariffs on Australian wine and other agricultural exports.

Valuation risk is coming back into markets

(Fig. 5) AU 10y yield vs ASX 200 NTM PE

As of October 31, 2023.

Past performance is not a reliable indicator of future performance.

Source: FactSet data. Financial data and analytics provider FactSet. Copyright 2023 FactSet. All Rights Reserved.

Earnings revisions have further to go

(Fig. 6) ASX 200 earnings revisions

As of September 30, 2023.

Past performance is not a reliable indicator of future performance.

Source: FactSet data. Financial data and analytics provider FactSet. Copyright 2023 FactSet. All Rights Reserved.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

December 2023 / GLOBAL MARKET OUTLOOK

Randal Jenneke is a portfolio manager and the head of Australian equities in the International Equity Division. He is a director of T. Rowe Price Australia Limited and a vice president of T. Rowe Price Group, Inc.