February 2022 / EMERGING MARKETS

Making the Case for Emerging Markets

Five factors supporting EM equities on a tactical and structural basis.

Key Insights

- Emerging market (EM) equities are currently out of favor, but we have identified five factors that we believe can support them going forward.

- Depressed valuations, improving earnings, and the turning of the Chinese equity cycle offer short‑term tactical reasons, while long term, the structural reasons for investing in EM equities remain compelling.

- We see the current environment as an opportunity for long‑term investors to potentially benefit from an attractive entry point.

The outlook for emerging market (EM) equities looks more promising in 2022. After poor performance last year, especially against developed markets (DMs), and U.S. equities in particular, we see greater potential for EM equities this year.

EMs have faced strong headwinds over the last couple of years with the coronavirus pandemic shuttering economies as slower vaccination rates delayed reopenings, while disappointing corporate earnings and a stronger U.S. dollar also buffeted markets. China proved to be the main drag on equity performance as regulatory actions across several industries ignited investor concern around the government’s priorities and caused Chinese equities to sell off sharply. While some concerns remain over the shorter term, we believe there are both tactical and structural reasons why EM equities look attractive.

Five Factors Supporting EM Equities on a Tactical and Structural Basis

Tactical factors support short‑term performance, while structural factors provide the case for long‑term investment

For illustrative purposes only.

Tactical

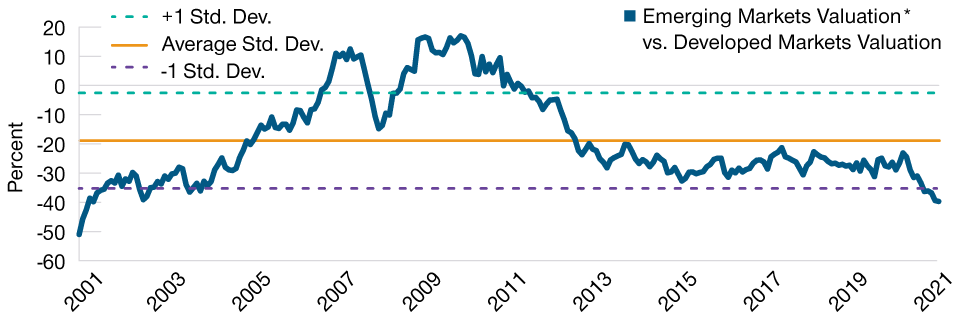

1. Depressed valuations overdiscount investor concerns, providing a catalyst for potential rerating

With valuations now sitting at a full one standard deviation below developed market equities (see Figure 1—the last time this happened was almost 20 years ago), we believe that the chances of a rotation into cheaper asset classes, like EM equities, has risen. Much of the differential can be attributed to the spectacular performance of U.S. equities over the last decade as stimulus and better corporate earnings, especially from the major technology companies, have combined to propel U.S. equities as an asset class above every other region. Many individual EM countries have seen positive returns, but upside has been limited. However, with valuations across the developed world unlikely to expand further, investors may refocus their attention back to emerging markets, particularly if their economies and markets begin to stabilize and improve, as we expect.

EM Equities Trade at Deep Discount to Developed Markets Equities

(Fig. 1) Potential rotation into cheaper‑valued assets with valuations across developed world unlikely to expand

As of December 31, 2021.

*12‑months forward price‑to‑book basis.

Source: HSBC.

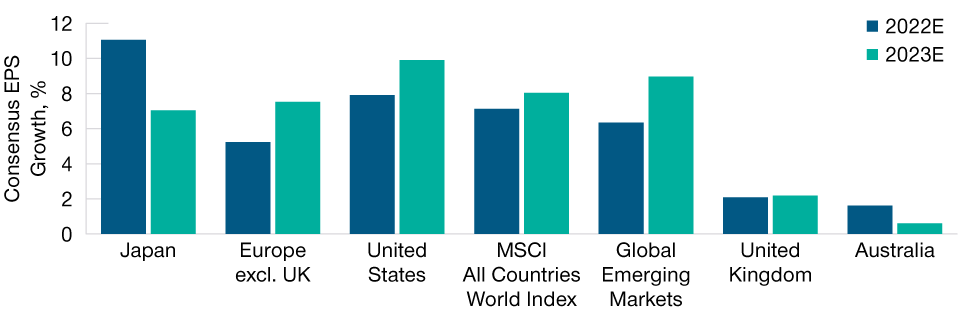

Profits growth is also likely to be the main driver of equity returns this year as stimulus fades and central banks tighten monetary policy. Current valuations in EMs overdiscount what could be more modest earnings in the first half of the year but more importantly do not reflect the improvement we expect later in 2022 and into 2023. Earnings per share (EPS) growth is expected to be only behind the U.S. in 2023 (Figure 2).

Turnaround in Earnings Growth Should Provide Further Catalyst for Markets

(Fig. 2) Markets predicting profits growth to accelerate in 2023

As of December 31, 2021.

E = Estimates. Actual outcomes may differ materially from estimates.

Source: FactSet. Financial data and analytics provider, FactSet. Copyright 2022 FactSet. All Rights Reserved.

We also anticipate a possible rotation within EM equity performance. A massive divergence between style factors was evident in 2021, with the MSCI EM Growth Index falling 8.4%, while the MSCI EM Value was up 4.5%. Sector returns were similarly spread out, with energy returning double‑digit returns as the oil price doubled, while consumer discretionary, real estate, and health care lost almost a quarter of their value.

We believe that companies offering growth at a reasonable price could be back in favor—where growth is not hot enough to drive the deepest cyclicals and not cold enough to need the defensiveness of highflying growth companies. Reasonably priced, higher‑quality companies that find themselves in the “core” of the market now look far more attractive, in our opinion.

More specifically, on a sector basis, we have long‑favored financials, and especially EM banks. There is a significant long‑term structural growth runway for credit and insurance penetration in EMs, while EM banks currently trade at moderately cheap valuations and enjoy higher return on equity (RoE) and higher credit growth than developed market banks.

Elsewhere, we expect consumer spending to rebound as economies and employment recover. Vaccine penetration has been catching up with rates in developed markets. This should result in fewer future restrictions on activity, enabling bottlenecks to be addressed and reducing disruption to manufacturing and logistics in 2022. This would prove beneficial to consumer‑related areas of the market.

2. Resilience against rising U.S. interest rates

Global stimulus in response to the pandemic has already started to fade, and with decade‑high inflation numbers causing concern, global central banks have started to tighten monetary policy. The U.S. Federal Reserve (Fed) is predicted to hike rates three or even four times in 2022. In the past, this would have caused much concern for EMs due to the high level of U.S.‑denominated debt they owed, but we believe many EMs are much more resilient when compared with the last Fed hiking cycle. External accounts are generally in good shape, recent capital inflow has been less “hot” than in 2013, and EM currencies are generally looking cheap. In addition, compared with developed markets, many EM fiscal and current account positions have improved during the coronavirus pandemic.

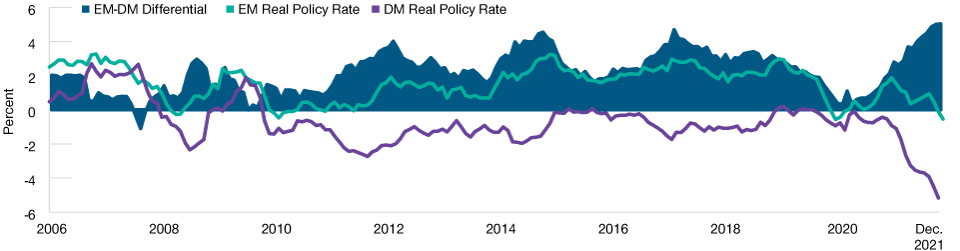

EM central banks have also acted earlier to tackle rising inflation. In contrast to developed market central banks, which were initially reluctant to raise interest rates to tackle inflationary problems, EM central banks have been ahead of the curve and willing to follow more orthodox policy. This should give confidence to investors that EM central banks are serious about keeping inflation under control. Many EM countries also have positive real rates, which gives them more scope to cut rates when conditions allow (Figure 3). China has already started to ease monetary policy in some areas.

EM Central Banks Have Been Disciplined and Tackled Rising Inflation Early

(Fig. 3) Scope for monetary policy easing when conditions allow

As of December 31, 2021.

Source: HSBC.

3. China’s equity cycle is turning

China suffered an onslaught of credit and regulatory tightening across several sectors last year to cap off its worst year since the global financial crisis. A string of regulations introduced in pursuit of common prosperity goals cast skepticism about prospective return on invested capital, reinvestment rates, and total addressable markets, prompting a protracted sell‑off in many of the market favorites, with consumer services, software, health care, real estate, and insurance losing more than a third of their value. More recently, we believe we have seen a potential inflection point in terms of policy prescription away from new regulations and toward one that should be more supportive of growth. We expect China, which was a drag on EM equities last year, to be a positive catalyst in 2022.

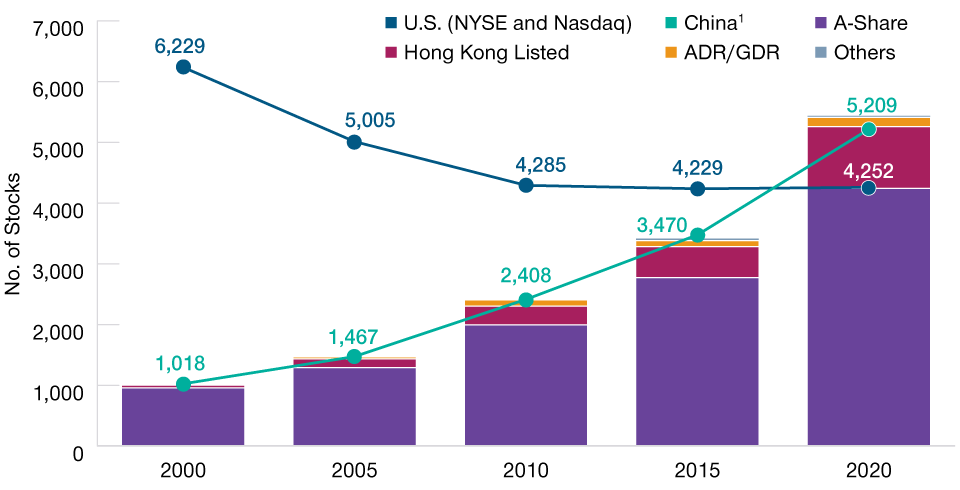

China’s Growing Investment Universe

(Fig. 4) Steady increase in the opportunity set that has seen it surpass the U.S.

As of December 31, 2020.

1 China total represents all listed stock. Dual‑listed ADR/GDR excluded to avoid double counting.

Sources: Bloomberg Finance L.P. and FactSet. Financial data and analytics provider, FactSet. Copyright 2022 FactSet. All Rights Reserved.

More generally, the dynamism, size, and depth of Chinese stock markets continues to excite us. Many foreign investors think of China’s investable universe as being confined to those companies whose American Depositary Receipts trade on the U.S. exchanges or that trade in Hong Kong. But domestic Chinese stocks, or A‑shares, feature many exciting and what we believe are undiscovered businesses. In fact, the investable universe in China has grown fivefold in the last 20 years and now exceeds the U.S. in terms of number of offerings (Figure 4). This rapidly expanding opportunity set offers real opportunity for long‑term fundamental investors to deliver alpha.

Structural

4. Long‑term drivers remain, but investors need to recognize change and be more selective

EMs, led by China, remain the most important engine of incremental global economic growth. Their dynamic economies, growing share of world trade, and increasing importance to asset markets are fundamental trends with long‑term significance. Add longer‑term aspects like urbanization, productivity, and, for many EM countries, more attractive demographics than developed markets, and it is easy to see why EMs should be attractive for investors.

Importantly, the EM universe has changed largely for the better. It is less reliant on commodities and is more diversified by sector and number of stocks. Looking at the sector weights within the MSCI Emerging Markets Index, we see that energy now makes up only 5.6% of the total index (as of December 31, 2021) versus 14.0% a decade ago. Meanwhile, materials have also fallen sharply, replaced by an increase in consumer discretionary, health care, and communication services stocks. However, the largest beneficiary of change and innovation has been in the technology sector, which now makes up almost a quarter of the index.

Because of these changes we need to adjust our assumptions about what environments could be most beneficial. Falling oil prices may be a catalyst for poor performance within Brazil or Russia but may also mean that consumers in China and India have more disposable income to spend on food, travel, or entertainment—areas that are now more heavily represented within EMs.

This ongoing change represents both a challenge and an opportunity. The playbook for allocating to EM equities is no longer solely cyclically driven. In the past, we used to ask questions like: Do you think global growth will be healthy? Do you think commodity prices will be strong? Do you think EM currencies will be stable? If the answer to all these questions was yes, then EMs were very likely to outperform other regions. Now one must concede that it is much more complicated. Macro factors like global growth, commodity prices, and currency markets are still important, but they are now part of a much broader mosaic of factors.

5. Emerging markets remain a rich source of alpha

In our view, the alpha component for EM equities remains strong, especially during the early and mid‑cycles of a recovery.1 In compressed absolute return environments, the relative value of available alpha has also typically risen. If consensus predictions of lower absolute equity returns in 2022 are to be believed, then exposure to EM equities should prove beneficial.

In addition, EMs tend to be less efficient and research coverage lower than in the developed world, making them an even more fertile hunting ground for investors to identify alpha opportunities.

There is also much more information asymmetry, emotion and fear, and greed at play. China is a great example where the market is heavily retail‑driven, especially the A‑share market, which means that market inefficiencies can occur. Currently, around 80% of the A‑share market turnover comes from retail investors, with the average holding period being only 17 days.2 This has generated great velocity and liquidity in the market but also has offered fundamental investors an opportunity to invest in mispriced assets.

Best Investment Approach? Increase Exposure on a Measured Basis

With investors’ disenchantment with EMs having become abnormally high, we see now as an opportune time for long‑term investors to potentially benefit from an attractive entry point. At the same time, we shouldn’t ignore the legitimate concerns some investors have for EMs, especially in the short term. We would therefore encourage investors to consider increasing their exposure on a measured basis through 2022, using periods of weakness and volatility to add exposure.

IMPORTANT INFORMATION

Where securities are mentioned, the specific securities identified and described are for informational purposes only and do not represent recommendations.

This material is being furnished for general informational purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date written and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

February 2022 / ASSET ALLOCATION VIEWPOINT