December 2021 / GLOBAL MARKET OUTLOOK

Playbook for a Shifting Economic Landscape

Looking for Growth in Challenging Markets

Key Insights

- The global economic recovery appears on track, but policymakers may be challenged to restrain inflation without stifling growth.

- Equity valuations are vulnerable to rising interest rates. Slower U.S. earnings growth could favor less expensive, more cyclical ex-U.S. markets.

- Risk of central bank missteps could keep bond markets volatile in 2022. With U.S. credit spreads tight, investors may want to cast wider global nets.

- Investment in global supply chains, public infrastructure, and renewable energy development could benefit capital goods and related industries.

Looking for Growth in Challenging Markets

After back‑to‑back years of strong performance across most equity and credit sectors, global markets face more uncertain prospects in 2022, according to T. Rowe Price investment leaders. Investors will need to use greater selectivity to identify potential opportunities, they say.

Higher inflation, a shift toward monetary tightening, and new coronavirus variants all pose potential challenges for economic growth and earnings—at a time when valuations appear elevated across many asset categories.

On the positive side, household wealth gains, pent‑up consumer demand, and a potential boom in capital expenditures could sustain growth even as monetary policy turns less supportive.

“Over the next year, I think the bottom line is that we will face slowing growth, but still very high growth,” predicts Sébastien Page, head of Global Multi‑Asset.

But strong growth and rising wages also could put further upward pressure on U.S. commodity and consumer prices, which accelerated sharply in the second half of 2021.

Mark Vaselkiv, CIO, Fixed Income, worries that the U.S. Federal Reserve may have fallen behind in the fight against inflation. As of mid‑November 2021, interest rate futures markets indicated the Fed wasn’t expected to begin raising rates until mid‑2022.

“The Fed may already be behind the curve,” Vaselkiv warns. “That could be the biggest risk for 2022.”

Economic growth should continue to support corporate earnings and credit quality in 2022. But the earnings momentum seen in 2021 is unlikely to be repeated, suggests Justin Thomson, head of International Equity and CIO. “It seems highly unlikely that positive [earnings] revisions will be of the same level of magnitude as we’ve been seeing.”

This could make the interest rate outlook an even more critical factor for equity performance. “If U.S. rate expectations get brought forward, I think equity markets will take their cue from that,” Thomson says.

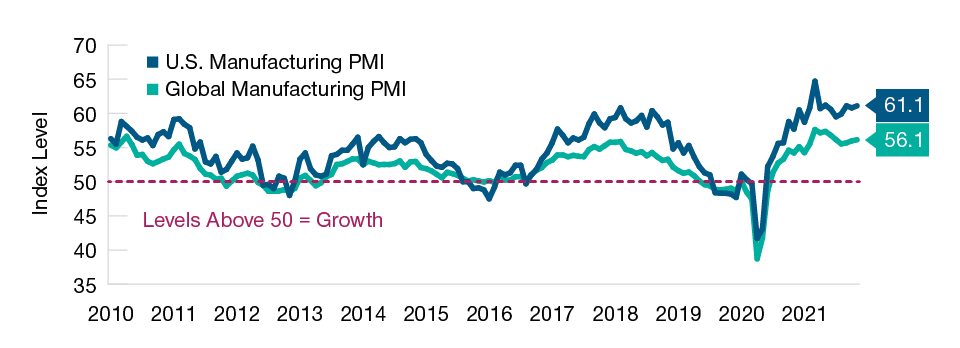

The Global Recovery Has Slowed but Still Appears on Track

(Fig. 1) U.S. and global Purchasing Managers’ Indexes (PMI) for manufacturing

As of November 30, 2021. Sources: Institute for Supply Management and J.P. Morgan/IHS Markit/Haver Analytics (see Additional Disclosures).

Explore our four themes:

| Themes | Description | Link |

| Growth Delayed, Not Derailed | The global economic recovery appears on track, but policymakers may be challenged to restrain inflation without stifling growth. | Click to view |

| Focus on Fundamentals | Equity valuations are vulnerable to rising interest rates. Slower U.S. earnings growth could favor less expensive, more cyclical ex‑U.S. markets. | Click to view |

| Navigating Policy Shifts | Risk of central bank missteps could keep bond markets volatile in 2022. With U.S. credit spreads tight, investors may want to cast wider global nets. | Click to view |

| Path to Global Sustainability | Investment in global supply chains, public infrastructure, and renewable energy development could benefit capital goods and related industries. | Click to view |

Summary

For the better part of the past two years, the global market outlook has been dominated by COVID‑19. While the omicron variant—and the possibility of renewed lockdowns—are still threats, the primary economic focus for 2022 has shifted to the risks that higher inflation and interest rates could pose for growth and asset returns.

Those concerns have put the spotlight squarely on the world’s central banks, particularly the U.S. Federal Reserve.

So far, the Fed’s go‑slow approach to tightening has avoided a repetition of the 2013 “taper tantrum.” But it looks increasingly out of step with the inflation fundamentals, Vaselkiv argues. “I think the probabilities of major policy mistakes are very high.”

Policy uncertainty is highlighted by a stark contrast between an accelerating U.S. consumer price index and nominal bond yields that as of mid‑November 2021 appeared to reflect much more benign expectations. How—and when—that contradiction is resolved could determine the performance of sovereign and investment‑grade credit sectors in 2022.

“It’s hard to disagree that bond valuations look stretched when real rates are near all‑time lows,” Page contends. “The bond market appears to have priced in an extremely dovish Fed and a sharp deceleration in growth.”

Barring a return to widespread pandemic lockdowns, the coming year could offer relatively favorable prospects for global equity and credit investors, T. Rowe Price investment leaders say, if pent‑up consumer demand, stabilization in China, and a potential upswing in fixed investment can—as they expect—sustain economic growth.

But, even if growth remains strong, it would be a mistake to assume the impressive U.S. earnings momentum seen in 2021 will extend into 2022, Thomson warns:

- There appears to be little room for margin expansion—especially if wage costs continue to rise quickly.

- While some industries, such as aerospace, airlines, hotels, and cruise lines, have lagged in the earnings recovery so far—potentially leaving room for positive momentum—they account for relatively small shares of S&P 500 capitalization.

Continued cyclical expansion, but with slower U.S. earnings growth, could bring to an end an exceptionally long period of U.S. equity outperformance over ex‑U.S. equities, Thomson suggests.

As noted by Page, negative real U.S. interest rates have lent critical support to historically stretched equity valuations. But in periods of rising rates, Thomson warns, “high valuations can become an albatross.”

Accordingly, Thomson argues, relative valuation considerations could favor less expensive, more cyclically exposed markets in 2022—such as Japan and the emerging markets, including China—that appear positioned to benefit from stronger global capital spending.

In an uncertain policy environment, asset allocation could be especially crucial for managing investment risk going forward, Page says. But that may require a more dynamic diversification approach than the traditional 60/40 stock/bond portfolio—and a broader mix of fixed income sectors than the typical “core” investment‑grade bond allocation.

“With real rates this low, we have to acknowledge that bonds may not diversify stocks as well as they have in the past,” Page says. “My view is that the 60/40 portfolio needs to be reoptimized for the current environment.”

2022 Tactical Views

1 For pairwise decisions in style and market capitalization, boxes represent positioning in the first asset class relative to the second asset class.

The asset classes across the equity and fixed income markets shown are represented in our multi-asset portfolios. Certain style and market capitalization asset classes are represented as pairwise decisions as part of our tactical asset allocation framework.

This material is provided for informational purposes only and is not intended to be investment advice or a recommendation to take any particular investment action.

IMPORTANT INFORMATION

Where securities are mentioned, the specific securities identified and described are for informational purposes only and do not represent recommendations.

This material is being furnished for general informational purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date written and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.