November 2022 / MARKETS & ECONOMY

Strong Growth Now May Not Mitigate a Recession Next Year

Central bankers may have to rethink this key assumption

Key Insights

- Central bankers appear to believe that current growth momentum in Europe and the U.S. should provide some mitigation against a recession in 2023.

- However, an analysis of past recessions suggests a weak relationship between economic momentum and the severity of a subsequent recession.

- If central banks downgrade growth expectations, risk assets will likely underperform and the yield curve can be expected to flatten.

Current central bank policies seem to depend on the belief that growth momentum and robust labor markets in the U.S. and the eurozone should help to shield economies from a recession next year. Unfortunately, the reality is more complex than this.

In the first of a series of articles on recessions and recoveries, we examine the extent to which past economic performance can predict future outcomes.

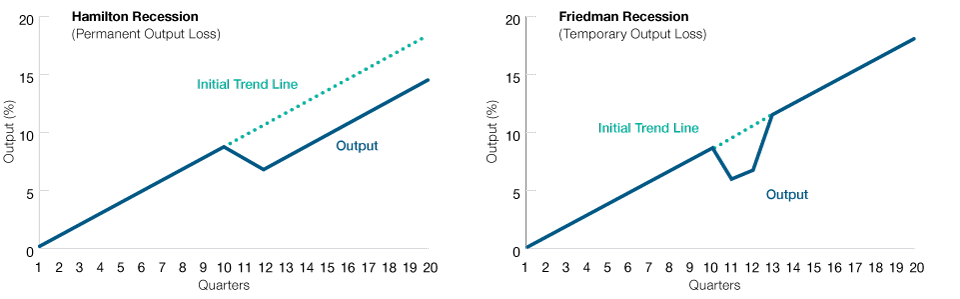

Two Types of Recession

Theoretically, there are two types of economic recession: a Hamilton recession (named after economist James D. Hamilton), where there is a permanent reduction in output from the pre‑recession level, and a Friedman recession (named after economist Milton Friedman), where the loss of output is temporary and the output returns to the pre‑recession level. The patterns of recovery following these two types of recession, which we’ll refer to as “Hamilton recoveries” and “Friedman recoveries,” are very different (Figure 1).

Hamilton and Friedman Recoveries Are Very Different

(Fig. 1) Hamilton recoveries have been common, Friedman recoveries have been very rare

For illustrative purposes only.

We analyzed real gross domestic product (GDP) data in 68 previous developed market recessions and their subsequent recoveries, focusing, in particular, on whether the level of real GDP converged to the path that was implied by the pre‑crisis economic growth trend. We discovered that during the vast majority of previous recessions, the level of real GDP remained permanently below the level that would have been achieved had the recession not occurred. In other words, the data clearly show that the majority of previous recoveries were Hamilton recoveries, with permanent effects on their output compared with before the recession. Notably, all of the deep recessions in developed markets were followed by Hamilton recoveries.

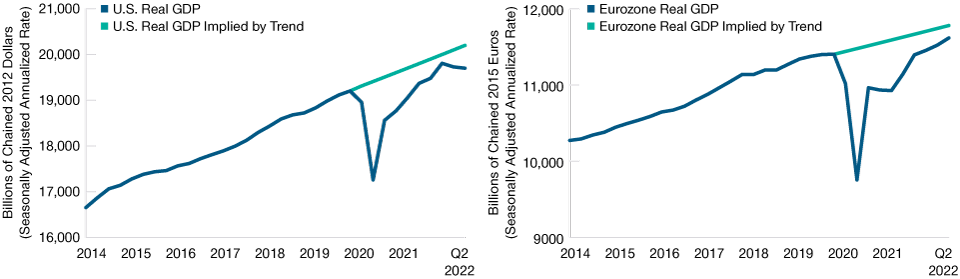

The U.S. and Eurozone Appear to Be Undergoing Friedman Recoveries

(Fig. 2) Growth momentum has been strong in both regions

As of June 30, 2022.

Real = Inflation‑Adjusted.

Sources: U.S. Bureau of Economic Analysis, Eurostat.

However, the current growth dynamics of both the eurozone and the U.S. more closely resemble Friedman than Hamilton recoveries. Growth momentum and labor markets have been strong in both economic areas—eurozone Q3 real GDP, for example, surprised consensus forecasts to the upside. As a result, the median Federal Open Market Committee (FOMC) member projects a growth rebound and a slightly rising unemployment rate in 2023, despite a significant tightening in monetary conditions.1 Similarly, the European Central Bank’s current base‑case scenario does not anticipate a 2023 recession for similar reasons.2

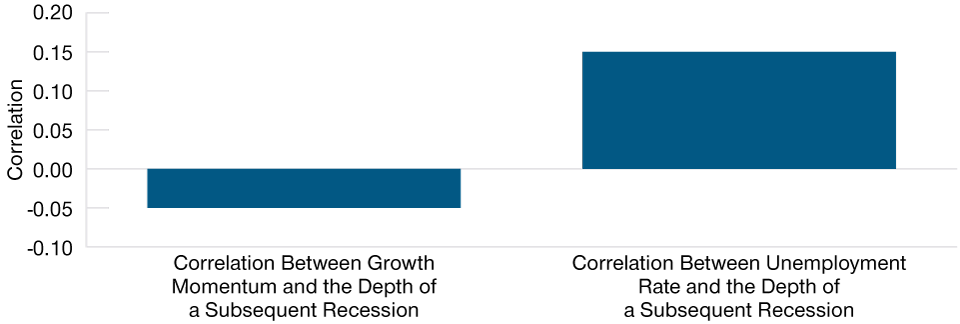

In a further analysis of previous developed market recessions and their subsequent recoveries, we examined whether growth momentum, defined as growth in the two years before the recession, is correlated with the subsequent depth of the recession. We also analyzed the relationship between the reduction in the unemployment rate in the two years prior to the recession and the depth of the subsequent recession. While we can make some inferences in both cases, these correlations were very low (Figure 3), indicating there is no statistically significant relationship between growth momentum and the depth of a subsequent recession.

The Correlation Between Growth Momentum and Subsequent Recession Depth Is Very Small

(Fig. 3) The correlation between the unemployment rate and subsequent recessiondepth is only slightly larger

Analysis as of September 30, 2022.

Sources: IMF/Haver Analytics and OECD. Analysis by T. Rowe Price. We analyzed 58 recessions andsubsequent recoveries in 12 developed countries from December 1, 1948 to December 31, 2019.

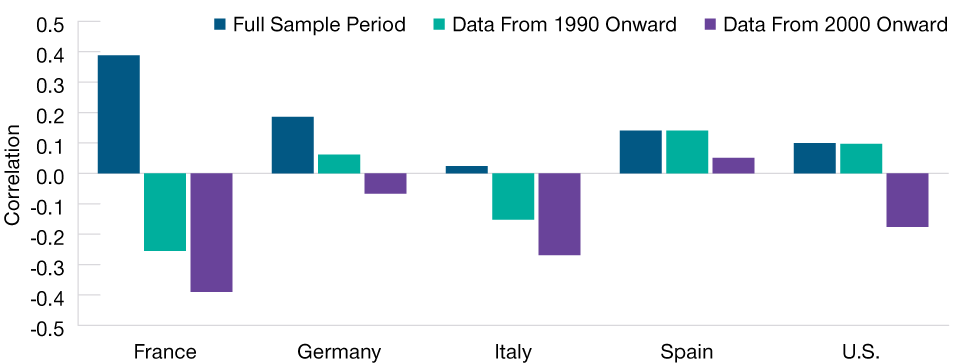

There are two important caveats to our analysis. First, the current recoveries in the U.S. and the eurozone are clearly unusual by historical standards, so comparing them to previous recoveries may be of limited value. Second, our analysis so far has examined whether economic momentum can mitigate output loss during recessions; it does not show whether momentum could prevent a recession. To address these caveats, we considered the correlation of yearly GDP growth with the following year’s GDP growth in the U.S. and major European economies (Figure 4).

Strong Growth Today Has Low Predictive Power for the Future

(Fig. 4) GDP growth in consecutive periods was weakly correlated

As of December 31, 2021.

We analyzed the correlation of yearly GDP growth and the year following in 5 countries from 1950 to2021. Note: Spanish GDP data are recorded from 1998.

Sources: IMF/Haver Analytics and OECD. Analysis by T. Rowe Price.

Our analysis shows that the correlation between economic momentum from one period to another, whether prior to a recession or not, is low across most economies, particularly in recent history. This does not mean that strong growth momentum today will not lead to a milder recession/slowdown in the future; rather, it implies that it is hard to make this prediction based on growth data alone. This is important for both markets and investors.

At present, monetary policymakers in both the eurozone and the U.S. rely on the narrative that strong growth momentum and a robust labor market will help their economies avoid a recession and achieve a soft landing, respectively. It is, of course, possible that this is the right assessment. However, historical analysis suggests that current economic strength is not a reliable guide to the future. There is therefore a significant risk that monetary policymakers could still change their minds with respect to their main economic narrative.

Such a change in the narrative, if accompanied by bearish real economic data, would have important consequences for asset markets. Yield curves would likely flatten as markets would begin to price in an end to the hiking cycle or perhaps even the start of a cutting cycle. The exchange rate move would be highly dependent on the size of the relative interest rate move. However, given the additional shocks that hit the eurozone economy, it is likely that the euro would depreciate further against the dollar. Risk assets would also likely underperform as real growth data would disappoint expectations.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

November 2022 / INVESTMENT INSIGHTS