November 2022 / INVESTMENT INSIGHTS

Global High Yield-Managing Through Volatile Markets

Fundamental research is imperative as macro headwinds rise.

Key Insights

- Prices often become dislocated from fundamentals in volatile markets, which creates potential attractive entry points for investors.

- However, the macro backdrop is more challenging, so fundamental research and a risk‑aware approach are imperative as defaults could peak over the next few quarters.

- We favor European high yield over the U.S. and see attractive value opportunities in European cable and services companies.

Value is back in high yield, but rising macro headwinds are causing significant volatility in the asset class. To navigate this more challenging environment, it’s more important than ever to follow a disciplined and risk‑aware investment process that emphasizes rigorous research. Why? Because it’s not just about picking potential winning companies; avoiding losers is just as important, particularly in the current climate where defaults could pick up over the next few quarters due to the slowdown in growth.

Volatile Markets Demand Far‑Reaching Insights

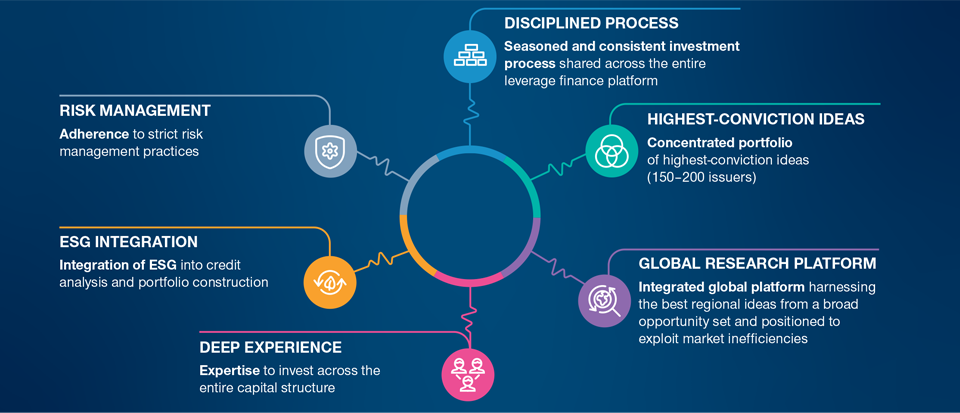

Credit‑intensive research is essential to fully understand a company and the potential risks and rewards involved with investing. This is at the heart of our approach, with a global team of more than 20 dedicated high yield analysts specialized by industry, region, and sector. This gives each analyst the in‑depth credit and structure analysis skills that are needed to accurately assess the optimal risk/return trade‑off. In addition, our analysts also leverage and collaborate with investment‑grade; sovereign; equity; and environmental, social, and governance (ESG) analyst teams, which allows for a holistic credit assessment of a company. This cross‑team effort combined with skilled active management helps inform decision‑making and prudent risk management, which we believe leads to better long‑term results.

As part of our process, analysts routinely stress test companies in order to develop a deep understanding of how companies might perform in a range of different market environments. Default scenarios are also constructed to identify the catalysts that could potentially trigger a credit event, as well as the likely effects thereafter. We conduct scenario analysis on an ongoing basis in order to identify both risks and opportunities to each individual security.

Global High Yield Investment Philosophy

(Fig. 1) Research at the heart of our approach

As of September 30, 2022.

Source: T. Rowe Price.

This year, our analysts have been undertaking deep assessments of how companies in their coverage area might be impacted by slower growth and an environment of higher interest rates and inflation. For example, will the company be able to pass potential increased input costs onto their customers? Could their margins be impacted? And, if so, what does that mean for future revenues and cash flow generation? Often, some of the impacts come with a lag, so it’s not just about evaluating what the conditions mean for a company now, but also how they might fare in 2023 and beyond.

In the current climate of heightened volatility, it’s important to stick to our stringent investment process that prioritizes fundamental research. This should not only enable us to potentially uncover great opportunities where prices have become dislocated from fundamentals, but also help us to avoid companies that might not survive the more challenging macro conditions.

Regional Views: Favor Europe Over the U.S.

Looking into areas where we are finding the best opportunities at present, we believe that Europe offers value despite its potential recessionary outlook—although selectivity is more important than ever. While we accept that Europe’s economy could suffer a deeper slowdown than its peers, the European high yield market should benefit from having less exposure than the U.S. to cyclical markets, such as commodities. Europe also has higher credit quality than the U.S., with more companies rated BB (70.7% in Europe versus 52.3% in the U.S.) and fewer companies rated CCC and below (5.5% in Europe versus 11.1% in the U.S.).1 Furthermore, Europe’s market is younger and less mature than the U.S., meaning it potentially offers more opportunities for price and information discovery, which we can potentially take advantage of with our research and active management.

Sector Picks: European Cable and Integrated Telecom Operators

Digging down further into sectors, we see value in European cable and integrated telecom operators. This industry is supported by long‑term trends in media consumption and stable, recurring revenue business models, which is important at a time when growth is slowing. We are also finding some value in the services sector. This is a large and highly diverse sector with lots of potential interesting opportunities on offer, but with rising prices, fundamental research is imperative.

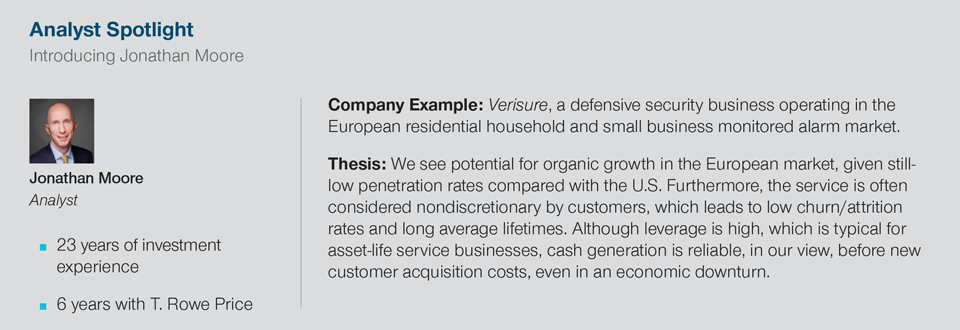

The specific security identified and described is provided for informational purposes only, does not represent a recommendation, and does not represent all of the

securities purchased or sold for advisory clients. No assumptions should be made that investments in the security identified and discussed was or will be profitable.

The foundation of our investment philosophy is the detailed understanding of the companies being considered. We seek to invest in companies that have strong and improving credit profiles within their industries. Equally important are the companies to be avoided. Our focus seeks to identify and avoid weak companies that are either run by poor management teams or contain situations that create an elevated expectation of default. The current climate of heightened volatility and macro headwinds offers potentially high rewards but also risks. Security selection is imperative, and key to that is fundamental research and a risk‑aware approach.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

November 2022 / INVESTMENT INSIGHTS