October 2022 / INVESTMENT INSIGHTS

In Volatile Times, Value’s Defensive Qualities Can Shine

Diversification and defensive attributes can prove attractive

Key Insights

- Value can potentially offer greater levels of defense in times of volatile markets.

- Inflation and rising interest rates are not prerequisites for value to succeed. Different types of value can be effective in a variety of market and economic conditions.

- Recent outperformance has been encouraging, but the entry point for investors remains attractive in our view.

Value as a factor has been enjoying a revival, and support is growing after many years in the investment wilderness. With inflation likely to remain elevated and central banks undertaking aggressive monetary tightening, the backdrop for value has improved.

Importantly, within value, investors can take advantage of diversification and defensive attributes. Higher exposure to financials, utilities, and cyclicals offers potential to mitigate the worst effects of inflation, while also offering greater levels of defense in times of rising rates and more volatile markets. Meanwhile, longer‑term trends of deglobalization, increased fiscal spending, the green transition, and a new investment/capex cycle building add a further defensive layer and support the longer‑term case for investment.

Regime Change That Remains in Its Infancy

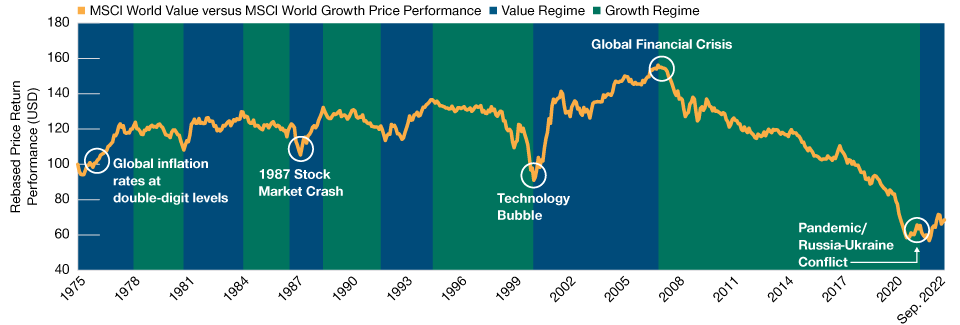

Concerns had grown about the sustainability of the outperformance of growth versus value stocks, which have proven justified. Following outperformance for value‑oriented areas of the market, the gap has narrowed slightly, but in historical terms, it is only moving from extremes (Figure 1). With our belief that markets exhibit regime changes, which can be sustained for long periods of time—the current value rally remains short compared with previous cycles (in blue).

We believe the pandemic and Russia’s invasion of Ukraine have set the wheels in motion for the next regime change. Bear markets also tend to be associated with a change in leadership. What has worked before is not necessarily going to work again.

Value’s Recent Outperformance Is Modest in the Longer‑Term Context

(Fig. 1) Investors still have time to balance their portfolio to potentially benefit from a shift to value

As of September 30, 2022.

For illustrative purposes only. Past performance is not a reliable indicator of future performance.

Performance rebased to 100.

Sources: MSCI and FactSet. Financial data and analytics provider, FactSet. Copyright 2022 FactSet. All Rights Reserved. (See Additional Disclosure.)

Inflation and Higher Interest Rates Provide a Supportive Backdrop for Value

Rising inflation is a significant feature of the regime change. For all the economic crises experienced over the past three decades, it’s safe to say that concerns about runaway inflation haven’t characterized any of them. From 1990 through to 2020, the average annual rate of change in the U.S. Consumer Price Index (CPI) was 2.4%, a far cry from the 7% run rate of the 1970s or around 6% levels of the 1980s. Fast forward to 2022, and the U.S. CPI stands at 8.2% (as of September 30, 2022), while other countries are reporting double‑digit inflation prints. The hopes that inflation was “transitory” have been categorically quashed.

Supply/demand pressures emanating from the pandemic started us on the path to decade‑high inflation numbers, but structural and long‑term inflationary pressures have also emerged. Wage demands are rising as workers seek to keep pace with the rising cost of living. Meanwhile, the geopolitical backdrop has worsened significantly, with the Russia‑Ukraine conflict prolonging and tensions between China and Taiwan (and subsequently China and the U.S.) intensifying. Consequently, agriculture and energy prices are likely to remain elevated and trade routes disrupted. This is likely to accelerate greater supply chain independence, further reversing the globalization trend that has driven prices down for much of the 21st century.

Greater fiscal spending and investment are also on the cards as authorities seek to bolster economies and support consumers. The coronavirus pandemic ushered in an era of government spending that we have never seen before, and we believe it will prove difficult for governments to deviate from that now. There is no shortage of things to spend money on. We expect more “helicopter money” to be directed toward consumers to help stave off rising prices, while further investment will also be made in infrastructure to stimulate economic growth and the green transition to meet carbon reduction commitments. The primary concern for markets is whether all these factors lead to marked increases in budget deficits, adding further to inflationary pressures.

Why “Value” Can Shine in This Tougher Environment

Higher inflation and higher rates have historically proven supportive for value stocks. The distinctive nature of value areas of the market means they can be better positioned to defend their earnings and retain profit margins during periods of price rises (utilities, industrials), while rising rates directly benefit financials.

At some point, inflation will peak as demand destruction takes hold and supply chain problems lessen. Even then, we expect inflation to settle back to higher levels than in the past. With central banks seeking to bring inflation back to within 2% target ranges, we therefore expect interest rates to remain higher, albeit from an ultralow base.

Higher inflation and higher rates, however, are not a prerequisite for value to outperform. Different types of value can be effective across a variety of market and economic conditions. Although many parts of the value universe are economically sensitive, such as banks and “high cyclical” industrials, it also includes a healthy representation of defensive areas, such as utilities and other traditional industries with strong pricing power. We have seen this in 2022 as consumer staples, health care, and utilities have outperformed the market (excluding energy stocks).

Equity Markets Remain Complex, but Our Focus Remains Unchanged

Our focus remains on finding the best companies at the right price and right time in their cycle. The environment remains complex, and there are many hurdles to negotiate. With inflation at such high levels, companies face poor visibility in terms of future costs of input. Corporate earnings are becoming more difficult to predict. Meanwhile, investors question whether the Fed can orchestrate a soft landing or only a modest recession as they hike rates.

Amid these challenges, stocks and portfolios that feature a buffer against the worst of inflation and offer diversification can potentially provide a useful counterbalance. With many value stocks offering a low bar to overcome in terms of valuations, and assuming the U.S. and the global economy do not fall into a deep recession, value offers an attractive risk/reward opportunity, in our view.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.