October 2022 / INVESTMENT INSIGHTS

Value Has Returned to High Yield

Fundamentals are strong, and spreads are attractive.

KEY INSIGHTS

- Volatility has pushed high yield bond spreads to extreme levels, but we believe the asset class’s fundamentals are stronger than valuations suggest.

- Recent history has shown that once European high yield spreads have reached more than 600bps, strong returns have typically followed.

- Market prices do not reflect the credit stability enjoyed by many high yield issuers on the back of lower borrowing costs.

Volatility has propelled high yield bond spreads to extreme levels, but we believe the asset class’s fundamentals remain solid, however, and that current valuations do not reflect its underlying strength. This suggests that high yield bonds are cheap by historical standards-and offer a compelling buying opportunity for investors seeking consistent income in the uncertain period ahead.

Anxiety over rising inflation, interest rate hikes, the war in Ukraine, and low growth have sent asset prices tumbling this year, and high yield bonds have been no exception. At the end of September, the effective yield of the ICE BofA Euro High Yield Index had risen to 8.1% from 2.8% at the beginning of the year. Over the same period, the spread on the index had widened from 3.3% to 6.3%.

The Buffer Is Back

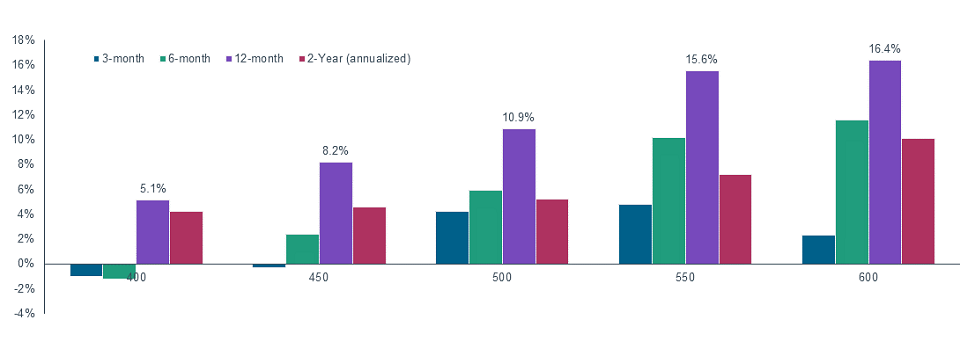

A unique feature of high yield debt is the yield “buffer” that it offers. High coupons should provide consistent and meaningful income, which helps dampen price volatility and has delivered attractive risk-adjusted returns over time. This year’s jump in yields has meant that this buffer is back again, providing investors with a powerful compounding effect. September’s yield to maturity of 8.53% compared with an average of 4.55% over the past 10 years.1 Recent history has shown that once European high yield bond spreads have reached levels of more than 600bps, strong returns have typically followed in subsequent periods (Figure 1). At the end of September, the spread-to-worst of European high yield debt was 639bps.

Performance Has Typically Bounced Back After Lows

(Fig. 1) Strong returns have followed stretched yield‑to‑worst levels

Past performance is not a reliable indicator of future performance.

As of September 30, 2022.

The date range is January 1, 2012 to September 30, 2022. The frequency of calculations is daily. Source: ICE BoA (see Additional Disclosure). Analysis by T. Rowe Price.

But are these stretched valuations merely reflective of higher expected default rates? It is certainly true that many high yield debt issuers face a difficult operating environment in the period ahead. On the one hand, rising energy, wage, fuel, and supply chain prices are pushing up input costs across the board; on the other, central bank rate hikes are increasing borrowing costs, which will reduce consumer demand-and this may ultimately lead to recession.

Firms facing higher costs and falling demand are at greater risk of default at the end of September, the market was pricing in a default rate of just under 5% in 12 months’ time. However, the current default rate is just 0.01%.2 Are the challenges firms face so formidable that the default rate is likely to rise from virtually zero to almost 5% within the next 12 months?

We do not think so. As a result of the refinancing wave of 2020-2021, most firms currently have high levels of cash relative to debt on their balance sheets. They have been able to borrow at very low rates for a long time, enabling them to extend maturities, reduce borrowing costs, and optimize capital structures. Given these positive fundamental factors, we expect a default rate of 1.5% over the next 12 months and 2.5-3% during 2023. JP Morgan is forecasting even lower default rates of 1% in 2022 and 2.5% in 2023. Both of these are much lower than the 20-year average default rate of 2.8% and the 4.8% priced in by the market.

Markets Are Driven by Fear, Not Fundamentals

In our view, the market is pricing in a much higher default rate because it is being largely driven by macroeconomic fears and is failing to recognize the stability that low borrowing costs brought to many high yield debt issuers. In other words, it is ignoring the fundamentals. Spreads could, of course, rise further as the U.S. Federal Reserve remains hawkish, vowing to continue hiking until inflation cools meaningfully which could push the U.S. into a recession.

However, even if spreads do widen further, we believe the probability of losing money over the next 12 months remains low. As Figure 1 shows, when spreads have reached 600bps over the past 10 years, investors have gained positive average returns over the subsequent three-month, six-month, 12-month, and two-year time horizons.

While equities are primarily driven by economic growth, high yield bonds are mainly about credit stability. The key questions for investors are whether they will receive their coupons and their principal back and how likely the firm is to default. Because the coupons on high yield bonds contribute a much higher proportion of total returns than dividends contribute for stock returns, the income profile is much smoother. For investors willing to take on a bit of risk in their portfolios, high yield bonds may therefore be a smart choice in the period ahead.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.