November 2021 / MARKET OUTLOOK

How ESG Helps Make Us Better Value Investors

Advantages of incorporating ESG factors into company analysis

Key Insights

- There are distinct challenges for value investors as many industries within the universe fall foul of some of the fundamentals of ESG investing. However, we believe that there is massive change ahead, and with this comes opportunity for active stock pickers.

- We believe identifying change and gaining conviction of ESG improvements can prove to be a powerful tool in the stock selection process.

- Estimating the intrinsic value of a company and buying mispriced stocks is at the core of value investing. ESG analysis has become a crucial factor in that process.

Momentum around integrating environmental, social, and governance (ESG) factors as features of investment decision‑making continues to build. Investors are increasingly alert to the impacts of environmental events linked to climate change, social issues such as diversity and employee treatment—and the influence of regulatory change related to these and other ESG factors. The upcoming UN Climate Change Conference (COP26) in Glasgow, Scotland is set to further highlight the need for global regulators, communities, and investors to accelerate action toward meeting the goals of the Paris Agreement and the UN Framework Convention on Climate Change.

For value investors, this brings distinct challenges. Indeed, some would suggest that the very nature of value investing, and the characteristics of the investment universe fall foul of some fundamentals commonly associated with ESG objectives. Many of the industries that feature heavily in the value investment universe can screen negatively on ESG factors, especially in areas like energy, materials, and utilities, which are historically high carbon emitters. But we will not achieve CO2 emissions reductions goals without their improvements. There is massive change ahead, and with this comes opportunity.

By integrating ESG factors into decision‑making, new stock opportunities or risks not fully appreciated by the market can be uncovered. Sometimes, the very features of stocks or sectors that make them laggards in the ESG space also mean that they have the potential to make a powerful contribution as they develop technologies, unlock resources, and channel finances that can help drive change. We believe ESG and active value investing can go hand in hand, and through engagement, we can gain insights into management’s thinking and potentially influence behavior.

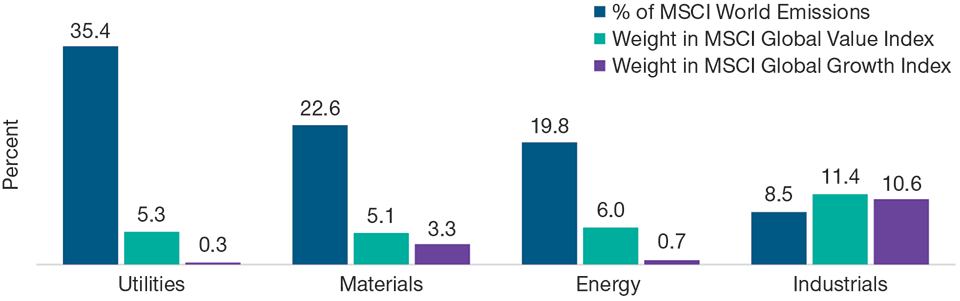

Value and ESG in Context—Potential in the Universe

Relative to some other sectors or styles in the market, a greater proportion of ESG laggards exist within the value space. Utilities, energy, industrials, and materials—sectors that typically rank poorly in terms of environmental characteristics—make up for almost 90% of the carbon footprint of the MSCI World Index, according to our internal models (Figure 1).

Value‑Oriented Sectors Have a Higher Exposure to Carbon‑Intensive Industries

(Fig. 1) But they have also more to gain from change, and offer investors potential opportunities to benefit from ESG improvements

As of September 30, 2021.

Sources: T. Rowe Price Responsible Investing Indicator Model (RIIM), MSCI, and FactSet. Financial data and analytics provider, FactSet. Copyright 2021 FactSet. All rights reserved (see Additional Disclosures).

RIIM is a proprietary tool developed to enhance research and aid better decision making.

But while the companies that mine and generate energy may be responsible for much of the pollution we are trying to combat, they are also integral to the transition process. As value investors we are in a unique position to help push for change. Rather than divest from extractive industries (e.g., mining and energy) we can guide and support change. Starving companies of capital is not the answer. Our job as fundamental stock pickers is to find companies that can thrive in this new world of cleaner energy.

Why as Active Investors We Can Add Value

At T. Rowe Price, we have the benefit of significant resources, which allows us to carry out thousands of company engagements every year. Discussing ESG helps us to understand companies’ management’s thinking, as well as giving us an opportunity to voice concerns and encourage positive behavior. We always try to invest with management teams that think and act as owners, often choosing stocks to invest in where management are incentivized by stock awards, as we believe there is a strong correlation between employee shareholding and stock performance.

At the same time, it is important not to shy away from potential controversy but to seek to fully understand the potential implications for a stock, both negatively and positively. We have found that if you identify change and gain conviction that improvements are underway, then this can potentially prove a good entry point for investment. Sometimes, that will mean taking a contrarian approach, especially during times of controversy, but one of the key foundations to our investment success in recent years has been the ability to stay engaged with stocks during periods of distressed sentiment to help us potentially benefit from the transition to a better outlook. While it is always tempting to wait for patterns of recovery to be established, history reflects that the early identification of fundamentals stabilizing, or the “stop getting worse” point, can be crucial to return generation.

Why ESG Integration Makes Us Better Investors

We have long taken ESG considerations into account when investing in stocks. As part of our fiduciary responsibilities, it is our job to analyze risk and reward, and we can only do this to the best of our ability if we consider all the potential risks around any investment. As shareholders, relationships with companies are of crucial importance when thinking about the sustainability of a company’s profit margins, for example. If a business is paying too low a tax rate, underpaying its staff, or squeezing its suppliers, then fundamental economics suggest that associated risks can potentially increase.

Good corporate citizens can also make good value creators, and there are many factors where ethical and financial performance are in step. Diversity within a business brings in different perspectives and reduces groupthink. Companies that treat their employees well are more likely to have a more loyal and motivated workforce, while those that manage their environmental impact may also help to reduce any legal or reputational risk.

Improving ESG profiles can also potentially improve the investment thesis (Figure 2). One part of our investment philosophy centers around identifying opportunities where uncertainty has caused a security to be temporarily mispriced. If you can identify opportunities or risks that are being misinterpreted by the market, then that has the potential to prove beneficial.

In the past we have identified areas where ESG risks have been insufficiently discounted, or on the flip side, where a company’s share price has been punished for bad behavior historically despite evidence of better behavior and progress toward improvement. We find that companies that are working to better their ESG standards will often eventually benefit from improved investor sentiment.

From a more defensive perspective, an appropriate awareness of ESG risks can also be an additional weapon against the value manager’s ubiquitous enemy, the “value trap.” Many companies can appear very cheap and have solid long‑term upside potential based on traditional financial factor analysis. However, by also including analysis of nonfinancial ESG factors, it can become clear that some companies are cheap for good reason.

While potential value traps may be prevalent, it is not always appropriate to assume the worst. It can often be a matter of disclosure, with company management not really understanding why ESG factors are of such interest to investors. Encouragingly, more and more, we are seeing an increasing appetite for engagement among companies’ management and a willingness to learn more about ESG.

ESG Has Become a Crucial Part of Reaching the Right Investment Decision

Our philosophy is to choose stocks that trade at a significant discount to our estimate of intrinsic value. ESG data represent an important source of information to help us accurately estimate this intrinsic value, even if it has not been factored in by the market. Identifying change amid controversy can also potentially create opportunity. But understanding how improvement and transition will work in terms of timing and necessary investment is key to understanding the impact on profitability.

Ultimately, value investing is about buying mispriced stocks where we think the potential reward is greater than the risks. In analyzing the risk part of that trade‑off, we consider everything that helps us reach the most considered conclusions, and ESG has become a crucial part of that process.

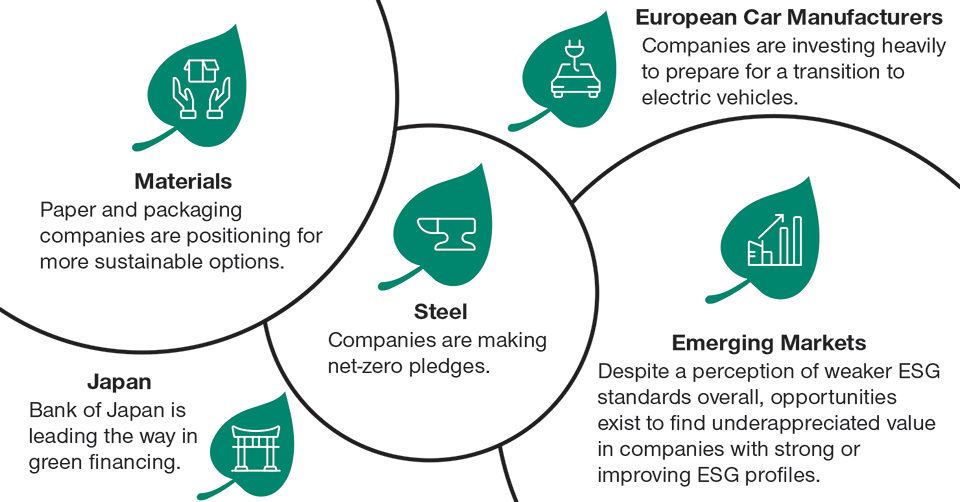

Uncovering Favorable ESG Profiles in the Global Value Space

(Fig. 2) Areas where we have identified improving ESG profiles that can potentially

improve the investment thesis

As of October 2021.

For illustrative purposes only.

European Car Manufacturers: Car manufacturers have historically screened badly on an ESG basis. Our forward‑looking analysis has identified how some of these companies are investing heavily to prepare for the transition to electric vehicles.

Materials: The last few years have been some of the hottest on record, and catastrophic weather events are demonstrating the reality of climate change. Paper and packaging companies are well positioned for the shift from plastics to more sustainable materials, particularly as e‑commerce becomes increasingly commonplace. Some companies in this space have access to forestry assets, which can play a further role in addressing climate change through carbon capture and storage.

Steel: There are many companies making net zero pledges, but some are ahead of others. For example, in Japan, one of the steel companies that we invest in has clearly stated that its top priority is to develop and practically implement breakthrough technologies to realize zero‑carbon steel. But changing processes to less carbon‑intensive ones is expensive, and “greening” the industry is likely to mean that only the largest companies can afford to do this. This creates barriers to entry, which has historically created a more favorable environment for established companies.

Japan: Japanese corporate governance standards have improved hugely, and corporate sector reform has been a key influence in the rise in Japanese company earnings and profitability in recent years. Japan’s central bank, the Bank of Japan (BoJ), has also been leading the way in terms of green financing. In what we believe to be the first of its kind, the BoJ has initiated policy to reward banks that finance green, decarbonizing investments by allowing them to shift their reserves on deposit with the BoJ from lower‑paying to higher‑paying interest categories.

Emerging Markets: Given the general perception of weaker ESG standards within emerging markets and the size of the universe, there are good opportunities to find underappreciated value in those companies with strong or improving ESG ratings.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution retail investors in any jurisdiction.