July 2023 / INVESTMENT INSIGHTS

Where Now for Global Equity Markets?

Five forces defining the equity cycle

Key Insights

- Equity markets are already focusing on when monetary tightening will be reversed. History suggests this will only occur when inflation falls sustainably below interest rate levels.

- With the era of stimulus behind us, equity return patterns are likely to differ from the past. This implies the need for breadth, and at times, a contrarian approach.

- Finding companies able to withstand margin pressures and maintain earnings growth through the next stage of the equity cycle will likely be rewarded.

Equity markets have performed well this year, but much of the gains have been concentrated in US mega‑cap technology stocks. Meanwhile, the US Federal Reserve (Fed) appears determined to stay the course until inflation shows real signs of decline. With the complexity of equity markets reaching new heights, investors are having to deal with a series of extremes that are both unusual, but highly influential. Below, we address five forces that will be key in shaping the next stage of the equity cycle.

The End of Stimulus

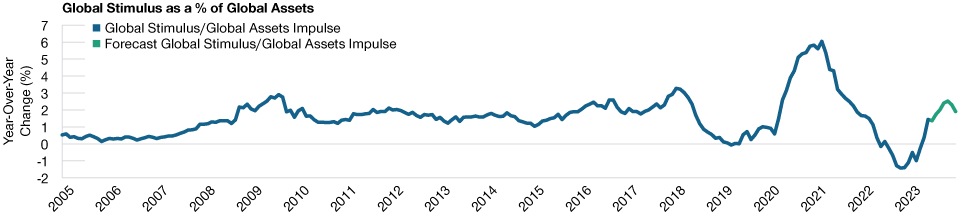

With the US Federal Reserve and other central banks tightening monetary supply (Figure 1) to deal with the inflationary hangover of the coronavirus pandemic, it is extremely unlikely that we will return to a stimulus‑driven world, given the clear risks posed by rising prices. This matters because stimulus has played such a large part in raising asset prices over the past decade. It also matters because the market is anticipating material interest rate cuts as we move into 2024.

The challenge for central banks is playing out via recent equity market strength. Despite the Fed aggressively trying to suppress inflationary pressures through the removal of stimulus and one of the fastest rate hike cycles in history, there is so much money in the global economy that there remains ample liquidity to create asset price inflation. The level of policy aggression has set the scene for risk events to emerge, such as the recent US banking collapses. But, despite a decelerating economy and worries over credit risk, we have seen investor bullishness replace extreme bearishness in a very short space of time. Regardless of the risks of rapid liquidity withdrawal, the Fed appears committed to deflating the economy. Its ability to manage inflation down in a smooth fashion may be tested in the next stage of the cycle, however.

Five Forces Defining the Global Equity Cycle

Investors are having to deal with a series of extremes

For illustrative purposes only.

Source: T. Rowe Price.

Economic Deceleration and a Hard or Soft Landing

One unusual feature in this market cycle has been the lack of synchronicity. Monetary policy tightening “normally” forces a deceleration in investment, spending, and hiring in unison, with the overall effect being broad‑based deflation. However, in this cycle, wages have continued to rise and consumption trends have remained solid, even as the economy decelerates.

Separately, we haven’t seen any meaningful credit cycle, and while there are some small signs that unemployment is on the rise, corporate sentiment remains relatively robust given the strength of balance sheets entering the tightening cycle. This means we have a labor market that is remarkably tight, despite the Fed trying to induce higher unemployment. This lack of synchronicity is partly the reason why the US economy is faring so well in the face of such aggressive monetary tightening. But this may mean more inflation—or at least more sticky inflation—as we move through the coming quarters.

Dramatic Decrease in Stimulus

(Fig. 1) Stimulus is back on a downward path after the recent U.S. banking crisis

As of May 31, 2023.

Global Assets Impulse = Global central bank and fiscal liquidity injections divided by the Total size of global financial markets.

There is no guarantee that any forecasts made will come to pass. Actual results may vary.

Sources: Bloomberg Index Services Limited. Bloomberg Finance L.P. U.S. Federal Reserve, U.S. Department of the Treasury, European Central Bank, Bank of Japan, and Bank of International Settlements. Data analysis by T. Rowe Price.

While the consequences of driving down inflation will potentially lead to lower economic growth (Figure 2), this has clearly become the Fed’s most favoured option when choosing between the “rock” and the “hard place.” However, the softness at which the landing is taking place, thus far, is acting as a soother for equity markets.

Download the full insight here: (PDF)

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

July 2023 / INVESTMENT INSIGHTS

July 2023 / INVESTMENT INSIGHTS

Scott Berg is the portfolio manager for the Global Growth Equity Strategy in the International Equity Division. In addition, he is an Investment Advisory Committee member of the Global Impact Equity, Institutional International Disciplined Equity, and International Disciplined Equity Funds. He is an executive vice president of T. Rowe Price Global Funds, Inc., and T. Rowe Price International Funds, Inc. In addition, he is a vice president of T. Rowe Price Group, Inc.