February 2023 / MARKETS & ECONOMY

The Mild Winter Will Delay Europe’s Recession, Not Prevent It

Other risks will likely weigh on the Continent later this year

Energy prices soared last winter after Russia’s invasion of Ukraine, then rose even higher during the summer amid fears of gas shortages. A large rise in energy prices has historically been a reliable predictor of eurozone recession—but unseasonably warm weather in recent months resulted in gas prices falling back to pre‑Ukraine war levels. With gas storages now topped up, does this mean that recession can be avoided?

The short answer is “no.” Although gas prices have come down, other risk factors have emerged that we expect will weigh on the eurozone economy later in the year. So while the fall in gas prices will support a rebound in the short term, I believe a recession in the second half of the year is still likely.

Many forecasters, myself included, expected the recession to begin in the fourth quarter of last year. We didn’t know then that a record‑warm winter would cause energy prices to tumble. Gas storage remains close to full, and a gas shortage this winter is now highly unlikely. This positive development, together with the normalization of supply chains, has boosted business confidence and enabled many gas‑intensive sectors to restart production again. This will likely result in an improvement in eurozone economic activity in the short term, making a gas‑driven recession unlikely this winter.

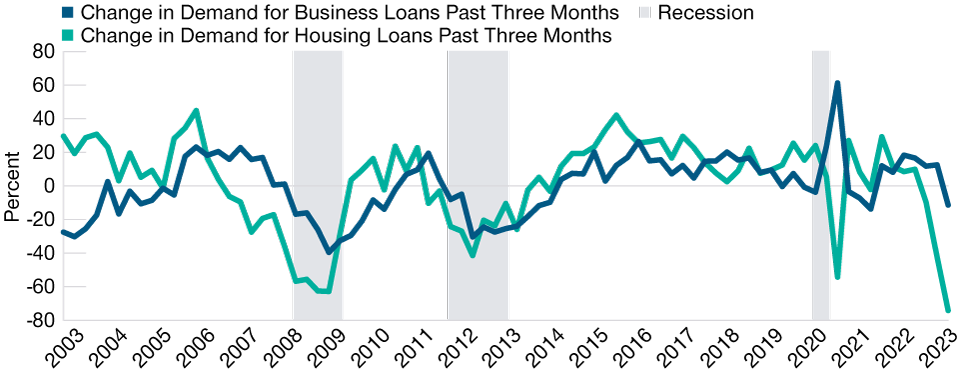

However, the gas price shock is not the only economic challenge the eurozone faces. In response to the rise in inflation and the fear of second‑round effects, the European Central Bank (ECB) has recently begun to tighten monetary policy at an unprecedented pace. This has meant that the cost of capital for firms, which was already very high before the ECB started tightening has risen to levels last seen during the eurozone sovereign debt crisis.

Similarly, monetary and financial conditions for households and firms, which were already tight, have been tightened further by the ECB’s hawkish monetary policy announcement and forward guidance of additional measures. Governments, firms, and households became more indebted during the era of low interest rates, which makes them more susceptible to these financial shocks. Since monetary policy works with a lag, it is likely that its negative effects will only be visible in the data by the fourth quarter.

Demand for Housing Loans has Plummeted

(Fig. 1) ECB tightening is having an impact

As of January 31, 2023.

Source: ECB Bank Lending Survey.

As an export‑dependent bloc, the fate of the eurozone is heavily tied to that of the global economy—and the news here is not good either. The global manufacturing Purchasing Managers’ Index (PMI) has been sliding into recession territory in the past couple of months, while in the U.S.—an important market for the eurozone—both the services and manufacturing PMIs have clearly entered recession territory. Importantly, order backlogs at German factories are now at five months compared with three months in normal times. This suggests that they will be able to weather this global weakness in demand in the short term but not in the medium term.

In the short term, eurozone activity will continue to be resilient as a result of lower gas prices, normalizing supply chains, and full order books. However, in the medium term, global economic weakness and the effects of monetary policy will likely result in a eurozone recession. Indeed, sticky core consumer price index (CPI) inflation, alongside resilient real activity, will support the ECB’s strong commitment to further monetary tightening. This will likely reinforce recessionary dynamics later in the year.

Falling Economic Activity Signals a Likely Recession

(Fig. 2) The global manufacturing PMI has been declining

As of December 31, 2022.

Source: S&P Global/Haver Analytics.

This view has several market implications. In the short term, sticky core CPI inflation and resilient activity will enable the ECB to continue its very hawkish path. Consensus forecasts will also likely move away from a recession scenario because of lower gas prices this year. Overall, we believe this will lead to a deepening inversion of the bund yield curve and a stronger euro in the next three months or so.

However, once the medium‑term factors take effect and recession looms, probably beginning in early summer, we expect the bund yield curve to steepen and the euro to fall.

T. Rowe Price cautions that economic estimates and forward‑looking statements are subject to numerous assumptions, risks, and uncertainties, which change over time. Actual outcomes could differ materially from those anticipated in estimates and forward‑looking statements, and future results could differ materially from historical performance. The information presented herein is shown for illustrative, informational purposes only. Forecasts are based on subjective estimates about market environments that may never occur. The historical data used as a basis for this analysis are based on information gathered by T. Rowe Price and from third‑party sources and have not been independently verified. Forward‑looking statements speak only as of the date they are made, and T. Rowe Price assumes no duty to and does not undertake to update forward‑looking statements. These statements reflect the views of the author. These views may differ from those of other T. Rowe Price group companies and/ or associates.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

February 2023 / INVESTMENT INSIGHTS