March 2022 / INVESTMENT INSIGHTS

Long-Dated Credit Can Boost Returns in a Tightening Environment

Shorter-dated bonds are typically hit harder by rising inflation and low growth.

Key Insights

- Last month the U.S. Federal Reserve reiterated its intention to begin raising interest rates this month.

- Higher policy rates make corporate borrowing more expensive, which is negative for corporate bond spreads.

- However, longer-dated have tended to outperform shorter-dated credit in tightening environments.

Last month, the U.S. Federal Reserve reiterated its intention to begin raising interest rates this month. Since then, Russia has invaded Ukraine, injecting a heavy dose of uncertainty into the economic outlook. The ongoing war will have an inflationary consequence globally via, for example, reduced supply of energy and perishable commodities such as wheat. While the increased uncertainty complicates the economic picture, these inflationary developments are unlikely to derail the Fed’s monetary tightening path. For investors, then, the challenge of how to position their portfolios for a rising rate environment remains a pressing one.

The Fed’s announcement last month was hardly a surprise. Stubborn inflationary trends caused by post‑pandemic easy monetary policy, supply chain disruptions, and rising energy prices have been a source of anxiety in markets for some time. Looming inflation puts pressure on central banks to tighten policy, which causes trouble for credit investors in two ways: first, rising bond yields have typically hit corporate bonds hard because of the duration embedded within them; and second, corporate bond spreads tend to be adversely affected by tighter financial conditions. In this article, we’ll focus on the latter.

Higher policy rates generally make corporate borrowing more expensive as investors demand a premium over the policy rate when they lend to corporates. Rising borrowing costs eat into corporate profits, which is negative for corporate bond spreads.

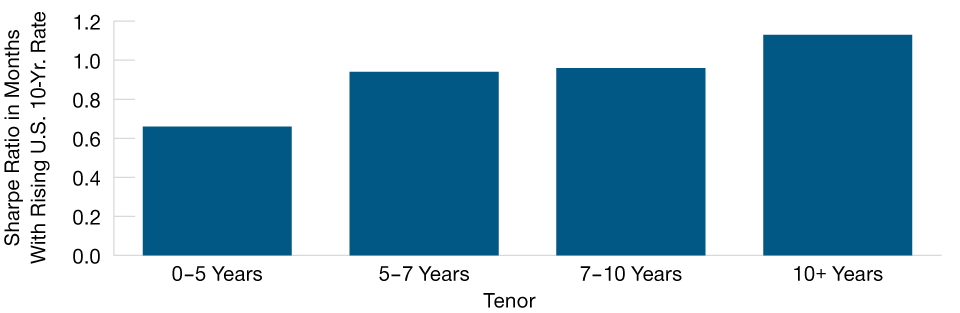

Not all corporate bonds are equal, though. Monetary policy tends to normalize in the long term as growth slows and/or inflation subsides. Aware of this, the markets tend to price in the fact that shorter‑term bonds will be heavily exposed to short‑term risks while longer‑dated bonds will likely benefit from a normalization of conditions. This is evidenced by the fact that, historically, the Sharpe ratios (a measure of risk‑adjusted returns) of longer‑dated U.S. investment‑grade (IG) corporate bonds have been higher than shorter‑dated IG bonds when yields rose (Figure 1). This suggests that credit investors may be able to boost performance in the period ahead by allocating more to longer‑dated credit.

Longer‑Dated U.S. IG Credit Has Outperformed During Periods of Rising Yields

(Fig. 1) Markets price in the normalization of policy in the long term

As of February 28, 2022.

Past performance is not a reliable indicator of future performance.

Based on monthly credit excess returns data between January 2000 and February 2022.

We take monthly credit excess returns for each of the four tenors above. For each month, we calculate the change in the U.S. 10‑year rate. We then take the subset of the months where the U.S. 10-year rate has gone up. On that subset, we calculate the annualized excess returns and volatility for each tenor. Sharpe ratio is calculated as the ratio of annualized excess returns divided by annualized excess return volatility.

Sources: Bloomberg Indices, Bloomberg Finance L.P.

It’s worth noting that the current tightening conditions differ from previous ones in a way that spells more risk for corporate bond spreads. Over the past 40 years, the Fed’s main goal with tightening has been to slow growth and prevent economic overheating; this time, it is trying to control inflation. This means that unless inflation falls back, the Fed is likely to continue tightening, even if growth is weaker than during previous tightening periods, which would hit shorter‑term credit harder than longer‑dated credit. An extended war in Ukraine could exacerbate this still further given that wars are invariably inflationary.

Positioning at the long end of the credit curve has the additional benefit of being cash‑efficient. Long‑dated bonds tend to have higher “duration times spread” (a measure of the credit volatility of a corporate bond) per dollar invested. This means that a target risk level can typically be achieved with a smaller cash outlay. Allocating to longer‑dated corporate bonds, therefore, should allow investors to unlock cash that may then be used in other ways to generate yields, such as purchasing Treasury inflation protected securities (TIPS).

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

March 2022 / INVESTMENT INSIGHTS

March 2022 / MARKETS & ECONOMY