March 2022 / INVESTMENT INSIGHTS

A Determined Federal Reserve Prepares for Tightening Cycle

We anticipate continued Treasury yield curve flattening

Key Insights

- The Fed is preparing to begin an aggressive tightening cycle, completing its pivot away from the ultra‑accommodative policy initiated in March 2020.

- The Fed’s goal is relatively simple: actively tighten financial conditions to slow inflation.

- We think that rate hikes will push short‑term Treasury yields higher, while moderating growth expectations will limit yield increases in longer maturities.

Amid some of the highest inflation readings since the early 1980s, the Federal Reserve is preparing to begin an aggressive tightening cycle in March, completing its pivot away from the ultra‑accommodative monetary policy initiated at the onset of the pandemic two years ago. The market has even begun to price some chance of starting with a hike of 50 basis points (bp)1 instead of a 25 bp move. While a 50 bp increase in March is not our base case, it is not out of the question. We expect this monetary policy transition to create volatility in financial markets, creating opportunities in mispriced fixed income securities.

At the January Federal Open Market Committee (FOMC) meeting, policymakers made clear that this tightening cycle will be very different from the previous one, which began slowly in December 2015 before picking up pace in 2017 and 2018. The Fed gave itself the freedom to not just hike 25 bp every quarter as it did from late 2017 through 2018. Instead, the pace of tightening in this cycle will be highly data dependent, and each FOMC meeting will be “live”—policymakers could announce a rate change at any meeting. This transition has freed the bond market’s imagination to consider the potential for a rate hike at each of the seven FOMC meetings through the end of the year, a scenario that we think is possible.

Fed’s Goal: Tighten Financial Condition

The Fed’s goal is relatively simple: actively tighten financial conditions—measured by Treasury yields, credit spreads,2 stock prices, and the price of the U.S. dollar—to slow inflation. We anticipate that the Fed will hike rates at every FOMC meeting while evaluating the impact on financial conditions as well as on the real economy in terms of inflation and the strength of the labor market. When financial conditions become restrictive enough to bring inflation down meaningfully, the central bank will reevaluate the pace and timing of rate increases.

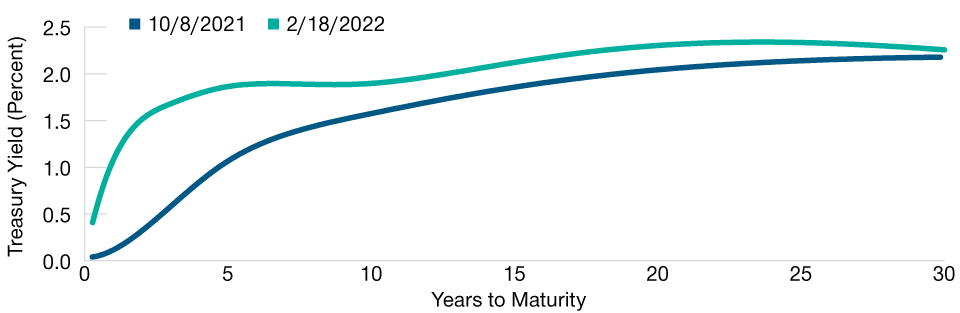

U.S. Treasury Yield Curve Flattens

Short‑maturity yields have increased markedly

Past performance is not a reliable indicator of future performance.

Past performance is not a reliable indicator of future performance.

As of February 18, 2022

Source: Barclays Live.

Risk markets like equities and credit are an essential component of financial conditions. In our view, this makes financial markets appear more vulnerable to Fed rate hikes than the real economy. Aside from expecting volatility in risk assets, it is unclear how they will react to Fed rate hikes, but we see little that could stop the central bank from actively trying to achieve its goal.

Fed May Look Through Growth Slowdown

That’s not to say that economic growth doesn’t matter to the Fed. Rather, we believe that the bar is set high for the Fed to capitulate on tightening policy due to concerns about high inflation. First‑quarter U.S. gross domestic product growth is already looking like it will be far lower than the 6.9% annualized rate in the fourth quarter of 2021. While it could be nearly flat or even slightly negative, we think that the Fed would be unfazed by that outcome, attributing it to temporary factors related to the omicron variant of the coronavirus. We anticipate a meaningful pickup in second‑quarter growth, but the risk in that forecast appears to be skewed toward the downside. Barring a major contraction, we think that some growth weakness will not slow the Fed’s tightening.

We are confident that inflation will decline, primarily as a result of calculating price changes from 2021’s relatively high base. However, inflation will probably remain much higher than the Fed’s target of 2% core personal consumption expenditures (PCE) inflation. Unlike growth, we see inflation risks as skewed to the upside. As opposed to lower‑than‑expected growth, it will be difficult for the Fed to ignore higher‑than‑expected inflation, which could lead to faster tightening.

Curve Flattening Set to Continue

We anticipate that Fed rate hikes will push short‑term Treasury yields higher, while moderating growth expectations will limit yield increases in longer maturities. This would cause the yield curve to continue to flatten. The spread between the yield on the two‑year and 10‑year Treasury notes has already decreased from almost 130 bp in early October 2021 to around 50 bp in mid‑February,3 and we see this narrowing further.

In our view, this spread could easily become meaningfully negative in 2022 as the yield curve inverts. An inverted yield curve has historically been a fairly reliable indicator of an imminent recession. However, we think that the unusual environment of the Fed exiting the extreme levels of accommodation implemented at the beginning of the pandemic has reduced the accuracy of this signal, and we do not expect a recession.

Favor Curve Flattener, Lower‑Duration Assets

In many of our fixed income strategies, we have been focusing on tactics that would benefit from the changes that we anticipate as the Fed tightens:

1. Positioning for further curve flattening. Our core bond strategies have been underweight short‑maturity Treasuries and overweight longer‑maturity Treasuries in seeking to benefit from further curve flattening. In terms of overall duration4 exposure, we have been more cautious by staying fairly close to benchmark duration. Because we think that slowing growth will limit increases in medium‑ and longer‑term Treasury yields, we have more conviction in the curve flattening position than in maintaining a meaningfully short overall duration exposure.

2. Added floating rate instruments. In many of our multi‑sector fixed income strategies that allow below investment‑grade exposure, we continue to favor exposure to bank loans, which have very little duration as a result of their coupon payments that periodically reset in line with a floating base interest rate. Some segments of securitized credit5 also have floating interest rates, and the performance of many bonds in this attractively low‑beta asset class could benefit from ongoing consumer strength.

3. Trimmed investment‑grade corporate bonds. We have also reduced exposure to investment‑grade corporate bonds because of their high duration and relatively expensive valuations, which expose the sector to high market volatility.

Rapid Tightening to Create Volatility

Aside from a major sell‑off in risk assets or a prolonged growth contraction, there is little else to keep the Fed from hiking rates at each of the seven FOMC meetings between now and the end of the year. The central bank is content that it has met the full‑employment part of its mandate and is now fully focused on taming inflation to meet the other part of its mandate. The public also seems to be focused on inflation—in particular, rising oil and energy prices—rather than the labor market, which looks so tight that it is unlikely to be derailed by higher rates. As a result, Fed policymakers do not appear concerned about the potential for overtightening.

In short, we think that there is little that could derail the Fed’s rate increases in 2022. Adding the potential for the Fed to move once in an increment of 50 bp, the central bank could even tighten the equivalent of eight 25 bp moves this year. Although this pace is obviously much faster than in the post‑global financial crisis tightening cycle, the economy appears resilient enough to withstand a more aggressive pace of rate increases.

While the economy should be able to weather rate hikes, we anticipate that the rapid tightening will create volatility in financial markets, particularly in risk assets. This volatility should help generate opportunities in various fixed income sectors to buy bonds at relatively attractive valuations. Overall risk levels in our core bond portfolios are running near the low end from a historical perspective, and we are maintaining liquidity in our portfolios so that we can add exposure to these opportunities when they arise.

WHAT WE’RE WATCHING NEXT

The Fed typically focuses on core inflation, which excludes volatile food and energy prices. However, with consumers alarmed about skyrocketing prices of some groceries as well as stubbornly high oil and gasoline prices, these items are drawing attention from the central bank in this cycle. As a result, we are closely monitoring food and energy prices as well as consumer sentiment indicators.

General Fixed Income Risks

Capital risk—the value of your investment will vary and is not guaranteed. It will be affected by changes in the exchange rate between the base currency of the portfolio and the currency in which you subscribed, if different.

Environmental, social, and governance and sustainability risk—may result in a material negative impact on the value of an investment and performance of the portfolio.

Counterparty risk—an entity with which the portfolio transacts may not meet its obligations to the portfolio.

Geographic concentration risk—to the extent that a portfolio invests a large portion of its assets in a particular geographic area, its performance will be more strongly affected by events within that area.

Hedging risk—a portfolio’s attempts to reduce or eliminate certain risks through hedging may not work as intended.

Investment portfolio risk—investing in portfolios involves certain risks an investor would not face if investing in markets directly.

Management risk—the investment manager or its designees may at times find their obligations to a portfolio to be in conflict with their obligations to other investment portfolios they manage (although in such cases, all portfolios will be dealt with equitably).

Operational risk—operational failures could lead to disruptions of portfolio operations or financial losses.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

March 2022 / MARKETS & ECONOMY

March 2022 / INVESTMENT INSIGHTS