December 2022 / MARKET OUTLOOK

Asia ex-Japan 2023 Market Outlook

Patiently Building Long-Term Positions

Key Insights

- We are relatively constructive on Asia ex-Japan equities. The short-term setup for China and North Asia is attractive, with cheap valuations and under-owned markets.

- Clear signs of China reducing COVID restrictions and providing more support to the property sector, if sustained, bode well for earnings in 2023.

- While valuations look stretched, India is on the cusp of a higher growth trajectory driven by the investment cycle. Southeast Asia can benefit from further foreign investment.

We remain relatively constructive on Asia ex‑Japan equities for 2023. The short-term setup for China and North Asia looks attractive: Valuations are at cyclically depressed levels, and the markets are very under-owned by global investors. We are seeing clear signs of China reducing COVID restrictions and providing more support to the property sector. This should bode well for earnings in 2023 should this direction of policy travel continue. We are also expecting inventory correction in the technology sector to bottom out in the first half of 2023, followed by an earnings rebound in the second half. Technology is a very important sector for North Asia.

In India and Southeast Asia, we are a little more cautious in the short term. Valuations, especially in India, look stretched in the short term. However, we believe India may be on the cusp of a higher growth trajectory driven by a new investment cycle and an improved ability to manage imported inflation pressures. Southeast Asia can benefit from further foreign direct investment (FDI) as some multinational companies look to diversify their supplier base away from China. Any market corrections are an opportunity to increase our exposure, especially to India.

Global Growth Challenges

The global economy faces a number of headwinds in 2023, including Russia’s invasion of Ukraine, rate hikes to contain inflation, a negative fiscal impulse as pandemic stimulus unwinds, the elevated U.S. dollar, and weak growth in China. Despite this broad mix of headwinds, few expect a deep global recession. Mainstream forecasts are for low but positive growth in 2023, with the International Monetary Fund projecting world gross domestic product (GDP) growth of 2.7%.

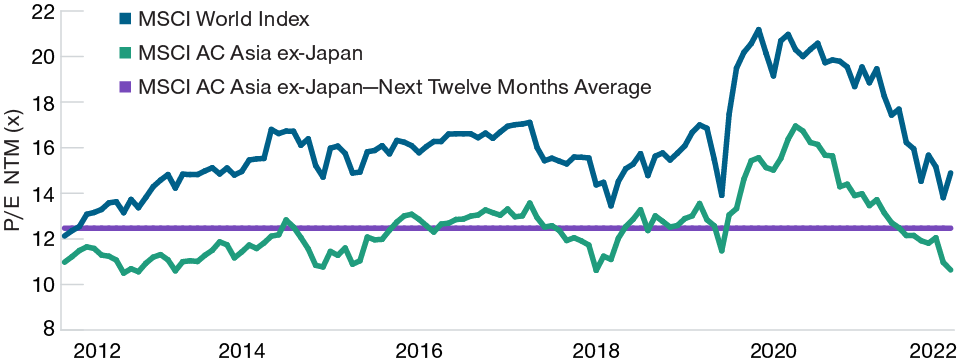

Asian Stocks Are Close to Their Long-Term P/E Ratio

(Fig. 1) Asia ex-Japan versus world forward price-to-earnings (P/E) ratio

As of October 31, 2022.

Source: MSCI via FactSet (see Additional Disclosure).

Overall, we see Asia as being relatively well placed to weather the global slowdown compared with other regions. A big reason for this is that we expect China to stage an economic recovery in 2023, which should support activity across Asia ex-Japan. China has the advantage of being at a very different stage of its business cycle compared to other major economies. Low inflation means there is room for China to expand credit and stimulate the economy after exiting from the zero-COVID policy. The post‑Congress announcement of 20 measures easing lockdown restrictions and 16 measures supporting residential property suggest a policy shift by Beijing from stability to growth.

In short, a recession in Asia ex-Japan in 2023 appears much less likely than for some other regions. Inflation in the region is not elevated compared with other major markets so there is less need for monetary tightening, while GDP growth forecasts for 2023 are clustered around 4.0%.

Ending China’s Zero-COVID Policy Is Crucial

When China ends its zero-COVID policy and fully reopens is crucial, not just for China but for the Asia ex-Japan region. The policy announcements on December 7 represent a significant easing of zero-COVID restrictions. They mark a clear turning point and signal that China intends to end the zero-COVID policy and reopen the economy as soon as conditions permit.

The path from here could still prove bumpy, though a lot of downside equity risk is likely priced in judging by the cheap valuations. On the negative side, the increased emphasis on vaccinations could mean Beijing is bracing itself for a major omicron variant outbreak during the winter flu season. The recent rise in new daily cases to around 23,000 nationally is not encouraging in this regard.

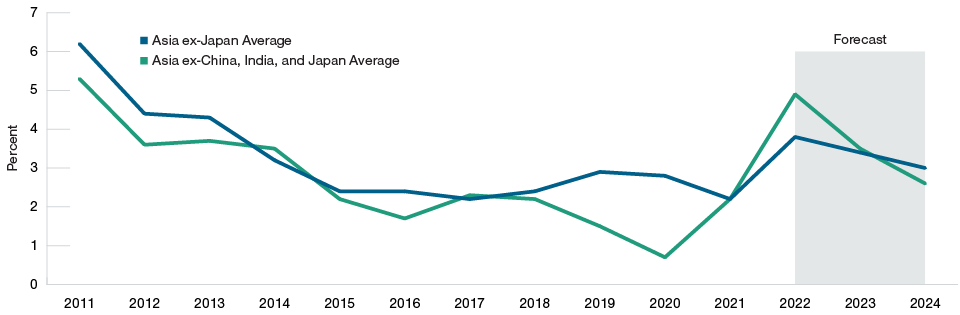

Asia Has Less Inflation Pressure

We believe that Asia ex-Japan is relatively well placed with regard to inflation, which appears to have peaked for a number of countries during the third quarter. The early inflation peak is because regional economies refrained from massive monetary and fiscal easing during the pandemic. Asian economic policies did not stoke inflation pressures in the same way that the developed economies did, and Asian central banks are closer to the end of their rate hike cycles. We have seen an improvement in Asia’s inflation trend relative to the U.S. and Europe, with a key reason being that Asia has no serious labor shortages. The lack of inflation in China will enable the country to focus on growth policies going forward.

Asia ex-Japan Inflation Expected to Cool in 2023

(Fig. 2) Headline consumer price index % year on year

As of September 30, 2022.

Source: HSBC Global Research forecasts (nominal GDP purchasing power parity weights).

The strong U.S. dollar was a significant headwind for Asia ex-Japan equities in 2022. While major currency inflection points are very hard to call, the current period of dollar strength has lasted for around 11 years and looks quite stretched by historical standards. With U.S. interest rates appearing closer to the peak, inflation starting to improve, and rising U.S. recession risk, the probability of the U.S. dollar peaking appears higher today. If it does, it will remove what has been a headwind to Asian equity performance in 2022.

Deglobalisation Risks Limited

We believe that the risks to Asia ex-Japan economies posed by deglobalisation are limited in the short term. There has been no post-pandemic rush to shorten global supply chains, despite much debate on the subject. The U.S. remains China’s largest merchandise goods trading partner, and China remains the largest supplier of merchandise imports to the U.S. and the third-largest export market. In China’s case, total FDI (Foreign Direct Investment) rose to a record level in 2021 and continued to grow even in the difficult conditions of 2022. Nonfinancial sector FDI equaled USD 138.5 billion over January to September according to China’s Ministry of Commerce. Historically, many U.S. and other foreign investors have reinvested a large share of their China profits.

Many foreign companies have invested in China to supply the domestic market. They are there for the long haul and are unlikely to change their plans simply because of one or two years of subtrend growth on account of COVID. Others use China as a production base to supply overseas markets. Those that have relocated some manufacturing operations away from China have tended to favor destinations like ASEAN, Mexico, and India. So at the regional level, there will be both winners and losers from deglobalisation. Net-net, the impact on Asia ex-Japan may be fairly small in the short term, with the negative to China offset by positive spillovers to ASEAN countries like Vietnam, Malaysia, and Indonesia.

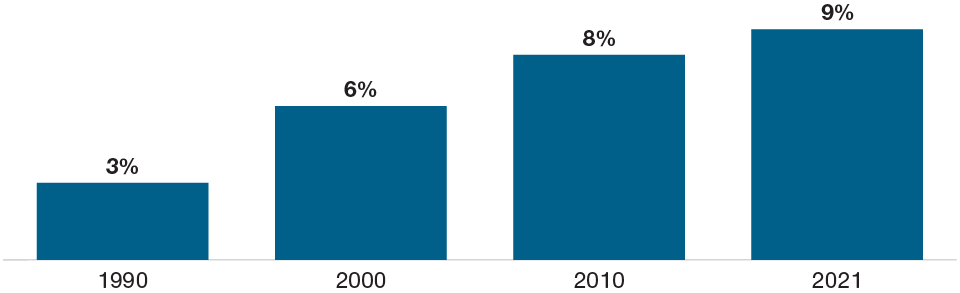

Regional Integration to Deepen

We believe China’s economic upgrading could lead to further regional integration with Asia ex-Japan. Intra-Asian exports have grown as a share of world exports, albeit more slowly over the past 10 years than in previous decades (Figure 3). China actively seeks closer economic ties with the ASEAN countries of Southeast Asia. A key aim will be to keep supply chains and markets open for a regional trade pact, where annual merchandise trade is close to USD 900 billion.

Asian Regional Economic Integration to Continue

(Fig. 3) Intra-Asian exports as a share of world exports

As of September 30, 2021.

Source: Haver Analytics.

Trade between China and several of the larger ASEAN economies expanded rapidly in 2022, despite the ongoing COVID disruption. China is a major foreign investor in Southeast Asia, accounting for around 8% of total FDI flows to the region in 2016—2020, a 65% increase over 2011—2015. China has long sought to move more of its lower-value-added exports to neighboring countries with lower wage costs. China’s exports to Vietnam rose 40% over 2019 to 2021, with much of it being inputs and components for Chinese-owned export factories in Vietnam.

Investment Outlook for 2023

Performance in 2022 was much weaker versus our original expectations due to higher inflationary pressures caused by the Russia-Ukraine conflict, while China continued to persist with its zero-COVID policy and limited support to the property sector. However, we believe the 2023 outlook should be more promising. Investors in Asia ex‑Japan equities should be patient, as we believe many of the positive long‑term trends for Asia ex-Japan that we identified in our 2022 outlook remain valid, including environmental protection, the green energy transition, industrial and infrastructure upgrading, import substitution, the rapidly developing internet ecosystem, and deeper regional integration.

These trends can help to provide some guidance as we search for attractive bottom-up investment opportunities across the region. The substitution of imports with local products and services, strong domestic consumption, and consolidation in select consumer‑facing businesses are among the trends that we believe can continue to yield attractive investment opportunities in Asia ex-Japan.

As ever, we seek a balanced exposure to these longer-term growth trends in Asia, without wishing to take strong short-term macro-directional bets. In the current depressed market environment, we have sought to strike a good balance between finding near-term “mean reversion” opportunities, or stocks that we expect to rebound from oversold levels, and companies held for the longer term with good growth prospects supported by strong policy tailwinds.

China

We are cautiously optimistic regarding China, where a slowing economy, the property market downturn, rising geopolitical risks, and concerns for private business have reduced the valuations of Chinese equities to historically low levels. The Communist Party Congress that concluded in October has not altered Beijing’s push toward innovation and the green energy transition, in our view. Aside from Chinese companies with good secular growth and policy support, we also have exposure to attractively valued businesses that have been hit by policy headwinds–such as online companies, consumer names, and property-related firms–where we see significant potential for industry consolidation.

India and Southeast Asia

We can find good investment opportunities in south Asia and Southeast Asia. India’s equity market showed surprising resilience in 2022, buttressed by domestic investors, a post-pandemic recovery in domestic consumption, and the relative weakness of Chinese assets. In the short term, valuations are our main concern for India after such strong outperformance. Should valuations return to more reasonable levels, we would view India as a fertile hunting ground for new opportunities, as it has the region’s best demographics and long-term growth prospects. Southeast Asia is another regional bright spot as economies reopen after the pandemic while inflation risks have been relatively well managed.

South Korea and Taiwan

The electronics downturn is currently well advanced, and a rebound is expected in the second half of 2023, which should bode well for the tech-oriented markets of Taiwan and South Korea. With their innovation-driven economies supported by continuous upgrades in technology, both countries continue to offer attractive growth opportunities. In the case of Taiwan, we think the market has deeply discounted the geopolitical risks. We regard TSMC as having a strong position in the global semiconductor industry due to its continued innovation in advanced node chip manufacturing.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

November 2022 / INVESTMENT INSIGHTS