June 2021 / INVESTMENT INSIGHTS

Constructing a Chinese Equities Portfolio

Seek to exploit market inefficiencies and extract value from the investment universe

Key Insights

- Discovering the future winners early in their cycle and capitalizing on inefficiency can potentially lead to outsized alpha generation.

- China is a deep market, and it is crucial to go beyond the crowded top 100 names; 98% of the opportunity set is where the hidden gems are likely to be found.

- To fully leverage on inefficiency, investors need a multidimensional framework capturing different types of opportunities with the potential for compounding growth, nonlinear growth, and special situation characteristics.

China continues to undergo enormous change, and there are many factors to monitor in this massive and highly complex economy. Significant change continues in relation to China’s economic model, with concerted efforts to focus more on domestic growth drivers to help rebalance the economy. The rising power of the consumer, along with innovation and technology, are major dynamics driving economic growth.

Yet China remains substantially underrepresented within global indices. It makes up only around 5% of the MSCI All Countries World Index, while its economy represents a staggering 17% of total world gross domestic product (GDP) (Figure 1). This anomaly, however, is narrowing, and we expect China’s weighting in global indices to increase considerably over the next few years.

There are also major inefficiencies inherent within Chinese markets that active stock picking can try to take advantage of to find strong potential alpha opportunities. For example, the MSCI China Index is made up of just over 700 stocks with around 13% representation from A-shares, but the entire universe comprises more than 5,200 stocks with 65% of it in A-shares.1 The market is also heavily retail-driven, especially the A-share market, which means that market inefficiencies can occur. Currently, around 80% of the A-share market turnover comes from retail investors, with the average holding period being only 17 days.2 This has generated great velocity and liquidity in the market but also offers fundamental investors an opportunity to invest in potentially mispriced assets.

China Market is Underrepresented in Global Equity Indices

(Fig. 1) This is an anomaly and is starting to change

This is an anomaly and is starting to change")

*Figures for Global Equity Market Cap and Turnover Distribution are calculated using data for listed securities across all stock exchanges for the countries listed. Turnover: measurement of daily volume for listed securities traded on each country’s individual exchanges.

† Global GDP Distribution is to end 2019 as data for certain countries has yet to be calculated.

Sources: Goldman Sachs, MSCI, World Bank/Haver Analytics, and FactSet. Financial data and analytics provider, FactSet. Copyright 2021 FactSet. All Rights Reserved. (See Additional Disclosures.)

Here, we identify ways in which we believe active investors can exploit market inefficiencies and construct a Chinese equity portfolio:

Look Beyond the A-Share Market and Mega‑Caps—Adopt a Holistic and Active Approach

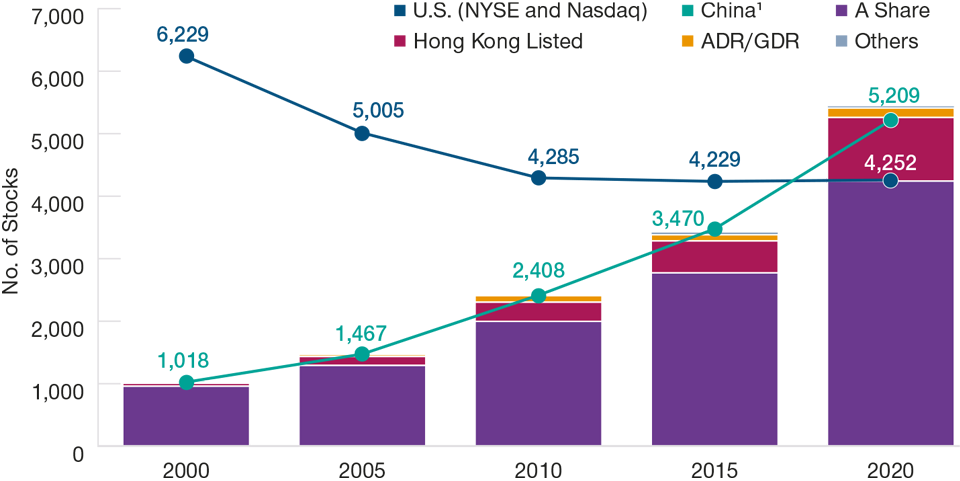

Many foreign investors think of China’s investable universe as being confined to the MSCI China Index or the A-share market (as represented by the CSI 300 Index), which features many of the large- and mega-cap companies. But there are huge potential opportunities outwith these markets that investors may be missing. In fact, the investable universe in China has grown fivefold in the last 20 years. In the first three months of 2021 alone, we saw around 300 IPOs, and China has now overtaken the U.S. in terms of stock listings (Fig. 2).

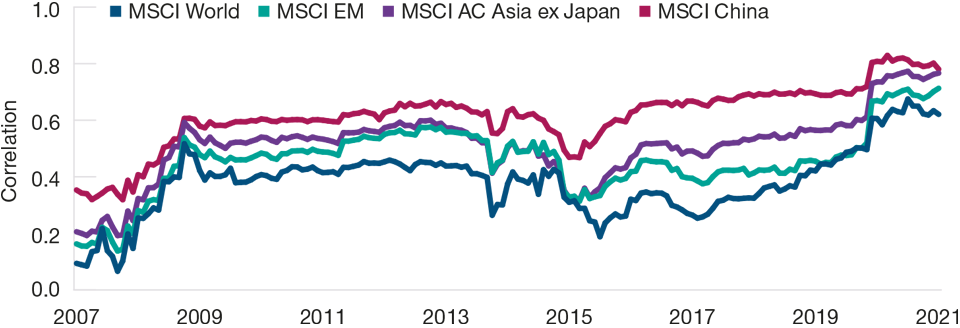

We would also argue that the A-share market no longer offers the same diversification benefits that were once heralded. The correlation of the China A-shares market with global indices has increased markedly since 2015 (Fig. 3). In particular, the correlation of the MSCI All Countries Asia ex-Japan Index and the MSCI China Index has become very high. This is primarily due to the increased participation of global investors, especially after the launch of the Stock Connect program in 2014. It proved to be a breakthrough for global investors seeking to invest in China, but it has contributed to the A-share market becoming more aligned to the performance of global markets.

Seek to Uncover the Future Winners

With the majority of flows being directed toward the 100 largest stocks in China (which only represent 2% of the total investment universe), we believe there is a huge opportunity for active managers to invest in the underresearched and under-owned today. It is important to be style‑agnostic, however, and focus on a bottom-up fundamental approach to help identify potential future winners early in their cycle, before they have potentially grown into the mega‑caps of tomorrow. That way, investors can focus on idiosyncratic alpha generation, which also means that returns may have a lower correlation with macro factors and overall market returns.

China’s Growing Investment Universe

(Fig. 2) Steady increase in the opportunity set that has surpassed the U.S.

As of December 31, 2020.

1 China total represents all listed stock. Dual listed ADR/GDR excluded to avoid double counting.

Sources: Bloomberg Finance L.P. and FactSet. Financial data and analytics provider, FactSet. Copyright 2021 FactSet. All Rights Reserved.

Diversification Benefits Have Become More Limited for Chinese A-Shares

(Fig. 3) Steady increase in correlation with global markets since 2015 on increased global investor participation

Past performance is not a reliable indicator of future performance.

As of March 31, 2021.

Sources: MSCI (see Additional Disclosures) and FactSet. Financial data and analytics provider, FactSet. Copyright 2021 FactSet. All Rights Reserved.

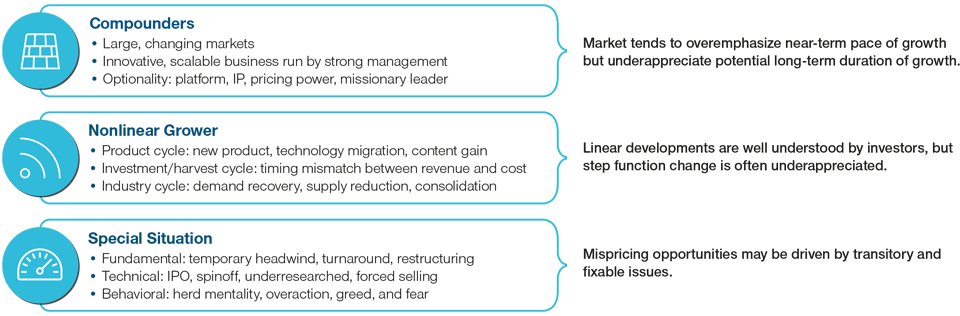

Encouragingly, China offers a number of companies with a long runway for growth. These potential “compounders” or “secular growers” can be attractive for long‑term investors as often their potential is not recognized by the short-term nature of market participants. Allocation to these, however, should be balanced with other areas, such as nonlinear growers and what we call special situation stocks. Nonlinear growers are companies that may be about to experience a positive product, industry, or harvest cycle following investment. Meanwhile, special situations are stocks that may be experiencing a temporary headwind or have been sold down due to a technical issue, such as forced selling following a spinoff, perhaps.

Focus on Key Areas and Themes That May Offer the Greatest Potential for Future Growth

In managing our portfolio we are focusing our efforts on finding value in sectors that are not correlated to macro factors, where we can use our stock‑picking skills. We believe that we are well positioned to take advantage of the changes that are happening in China as the focus shifts from “growth at any price” to “quality growth.”

A Multidimensional Framework

Three areas of focus in aiming to capture the best opportunity set

Consumption is an important pillar of growth for Chinese policymakers. Here, we are concentrated on companies that we believe can offer compounding growth opportunities but also ones where there is currently a positive product cycle. The shift of domestic demand from foreign brands to local brands is also important. We believe that many of these homegrown businesses can eventually take a leap further and expand into global leaders.

China is also striving to build a robust health care system for its 1bn+ population, and homegrown players are integral to that plan. We are also increasingly seeing ways to potentially benefit from China’s goal of becoming a greener economy. The transition away from a carbon-intensive economy to a more sustainable economy offers a tailwind to industrialization, with support being gradually shifted from traditional sectors such as oil and gas to modernized industrial and business services sectors.

Finally, we highlight “consolidation,” which is gaining increased momentum. Many sectors, from hotel chains and restaurants to offline pharmacies, are gaining market scale and becoming the main low-cost producers in their field. Importantly, this trend has nothing to do with how the macroenvironment is behaving, and it also doesn’t even matter if the underlying industry is growing or not. If the consolidation tailwinds are strong enough, they can prove beneficial.

Positive Backdrop Provides Robust Reasons for Investment

For many investors, Asia likely offers the greatest potential right now, and China is at the heart of that. We believe it is a highly inefficient market, making it ideal for alpha generation. We also expect the underrepresentation of China within global indices to materially change in the next few years. We encourage investors to explore the full opportunity set to find the best opportunities.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution retail investors in any jurisdiction.

June 2021 / INVESTMENT INSIGHTS