August 2022 / INVESTMENT INSIGHTS

Why Active Duration Management Matters

As market dynamics twist and turn, a flexible approach delivers results

Key Insights

- Having the flexibility to shift duration within a wide latitude enables us to be dynamic and to adapt quickly to different market environments, such as rising rates.

- To uncover what we feel are the best opportunities for our clients, our country selection is supported by our global research platform, covering both developed markets and emerging markets.

- Since inception, our duration views, country selection, and yield curve positioning have been the largest positive contributors to performance.

Among absolute return strategies, we believe that the Dynamic Global Bond Strategy stands out as it seeks to provide not only regular returns in different environments but also diversification from risk markets. That means that during periods of volatility, when risky assets such as equities sell off, we strive to be a performance anchor. To help achieve this, we have a high‑quality bias—investing a large portion of our portfolio in high‑quality government bond markets where liquidity is typically better. But it’s not just a case of being long sovereign bond duration at all times as that simply won’t work when interest rates are rising like they did in the first half of this year. That’s why we manage duration actively and within a wide latitude—an approach that enables us to adapt to changing market conditions. This has been critical in 2022, so far, and we believe it will continue to be, given the likelihood that volatility persists as fixed income markets enter a new market regime without the liquidity support of central banks.

Flexibility Around Duration Management

We manage duration dynamically and within a wide latitude, implementing both long and short duration positions. This gives us the flexibility to adapt to different market cycles and environments, including when rates are rising. For example, when interest rates are rising, we could move to quickly cut the portfolio’s overall duration (as low as minus one year) to minimize potential losses. By contrast, when rates are falling, we can increase overall duration to as high as six years to maximize possible gains.

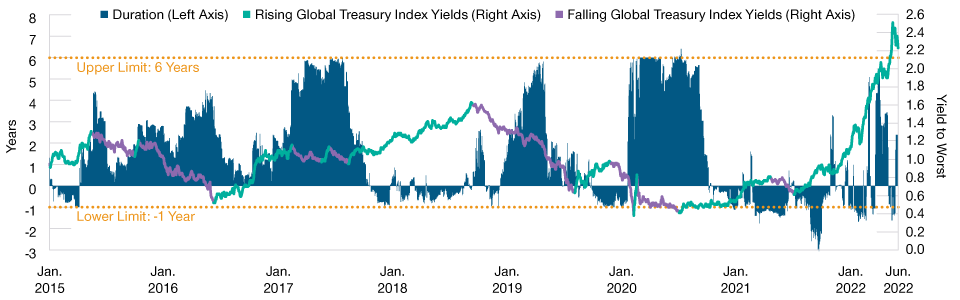

Active Approach to Duration Management

(Fig. 1) Historical duration of the Dynamic Global Bond (USD Hedged) representative portfolio

As of June 30, 2022.

Past performance is not a reliable indicator of future performance.

January 31, 2015 through June 30, 2022: Dynamic Global Bond (USD Hedged) representative portfolio. Index yield shown is for the Bloomberg Global Treasuries Index. Periods of rising and falling yields have been determined as periods of changes in yields of 15 bps or greater.

The representative portfolio is an account in the composite we believe most closely reflects current portfolio management style for the strategy. Performance is not a consideration in the selection of the representative portfolio. The characteristics of the representative portfolio shown may differ from those of other accounts in the strategy. Please see the GIPS® Composite Report for additional information on the composite.

Source: Bloomberg Index Services Limited. Please see Additional Disclosures for information on this Bloomberg information. Analysis by T. Rowe Price.

This dynamic approach to managing duration has been successfully applied during many changes in market trends and regimes since the strategy was launched:

2020—Concerns about pandemic and other risks to global economy

In 2020, for example, we kicked off the year with the portfolio’s overall duration in negative territory. We quickly pivoted in February and significantly increased duration as our health care analysts and economists flagged concerns about the spread of the coronavirus and the risks to the global economy. The changes—particularly moving from a short duration to a long position in U.S. duration—bolstered performance at a time of heightened volatility and a huge sell‑off in risk markets.

2022—Inflation pressures on the rise

Heading into 2022, we held the portfolio’s overall duration close to zero, anticipating that major central banks would become more hawkish to combat rising inflation pressures. Specifically, we saw potential for the withdrawal of liquidity support, which could mark the end of quantitative easing and the start of a new regime in fixed income markets. As such, we felt comfortable holding short duration positions in select developed market countries, such as the U.S. and UK, which worked well with global bond yields rising materially in the first half of this year as central banks responded to inflation by tightening monetary policy.

Crucial to our success in capturing changes in trends and regimes is the research of our senior economists and analysts, helping to identify inflection points in monetary policies and economic cycles.

T. Rowe Price Fixed Income Capabilities

(Fig. 2) Dedicated experts in the U.S., Europe, and Asia

As of June 30, 2022.

*Includes investment professionals for T. Rowe Price Associates, Inc. and its investment advisory affiliates, including T. Rowe Price Investment Management, Inc.

Source: T. Rowe Price.

Tactical Opportunities vs. Long‑Term Investment

Our global research platform is the engine that powers our investment ideas. Our deep research capabilities enable us to uncover inefficiencies and exploit opportunities across the full fixed income investable base. Since inception, the portfolio’s investments have ranged from major government bonds to lesser‑known developing country bonds rated below investment grade.

The strategy is designed so that we can be nimble and take advantage of short‑term opportunities. In order to gain a holistic view of a country, analysts conduct in‑depth research into the following key areas: fundamentals, valuations, and technicals. At different times, any one of those factors may hold sway. For example, compelling valuations may lead us to implement a long position, while at another time, we might initiate a short position based on concerns over deteriorating fundamentals. Getting the timing right on what feature is likely to influence bond prices the most is essential. Italy is an example of a country where we have tactically gone short and long at different times during the strategy’s life.

Taking a long‑term investment view is also important. In smaller and less developed countries, in‑depth knowledge and research can go a long way. Taking the time to gain a deep understanding of a country’s economic prospects, politics, and policymaking can open up potential attractive long‑term investment opportunities that others miss or avoid because they do not have the resources to analyze the market properly. For example, we have been invested in local Serbian government bonds in the strategy since March 2015.

Since inception, our duration views, country selection, and yield curve positioning have been the largest positive alpha contributor in the strategy. Our ability to express these views on a range of different countries and be tactical in managing duration to capture trend changes and regime shifts has been the driver of this. That is why it is so important that we continue with this approach—particularly in the current environment, where volatility is likely to remain elevated as central banks tighten monetary policy at a time when growth is slowing.

PERFORMANCE TABLE

Dynamic Global Bond (USD Hedged) Composite

Periods Ended June 30, 2022. Figures Are Calculated in U.S. Dollars.

Past performance is not a reliable indicator of future performance.

Gross performance returns are presented before management and all other fees, where applicable, but after trading expenses. Net of fees performance reflects the deduction of the highest applicable management fee that would be charged based on the fee schedule contained within this material, without the benefit of breakpoints. Gross and net performance returns reflect the reinvestment of dividends and are net of all non‑reclaimable withholding taxes on dividends, interest income, and capital gains.

*Effective May 1, 2021, the benchmark for the composite changed to ICE BofA US 3‑Month Treasury Bill Index. Prior to May 1, 2021, the benchmark was the 3 Month LIBOR in USD Index. Historical benchmark representations have not been restated.

† The Value Added row is shown as Dynamic Global Bond (USD Hedged) Composite (Gross of Fees) minus the benchmark in the previous row. Please see Additional Disclosures for information about this ICE BofA information.

‡ Since Inception January 31, 2015, through December 31, 2015.

GIPS® DISCLOSURE

Dynamic Global Bond (USD Hedged) Composite

Period Ended December 31, 2021. Figures Shown in U.S. Dollars.

*January 31, 2015, through December 31, 2015.

† Investment return and principal value will vary. Past performance is not a reliable indicator of future performance. Monthly composite performance is available upon request.

‡ Effective May 1, 2021, the benchmark for the composite changed to the ICE BofA US 3‑Month Treasury Bill Index. Prior to this change, the benchmark was the 3 Month LIBOR in USD Index. The change was made because the firm viewed the new benchmark to be a better representation of the investment strategy of the composite. Historical benchmark representations have not been restated.

§ Preliminary—subject to adjustment.

Dynamic Global Bond (USD Hedged) Composite—Objective and Risks Objective

The Dynamic Global Bond (USD Hedged) Composite seeks to deliver consistent fixed income returns through a flexible, dynamic, and diversified allocation to debt instruments from around the world. The strategy adopts a holistic and rigorous approach to risk management to protect clients on the downside and particularly seeks to provide adequate diversification at times of equity markets’ correction. (Created January 2015; incepted January 31, 2015)

Risks—the following risks are materially relevant to the portfolio:

ABS and MBS—Asset‑backed securities (ABS) and mortgage-backed securities (MBS) may be subject to greater liquidity, credit, default, and interest rate risk compared with other bonds. They are often exposed to extension and prepayment risk.

Contingent convertible bond—Contingent convertible bonds may be subject to additional risks linked to: capital structure inversion, trigger levels, coupon cancellations, call extensions, yield/valuation, conversions, write-downs, industry concentration and liquidity, among others.

Credit—Credit risk arises when an issuer’s financial health deteriorates and/or it fails to fulfill its financial obligations to the portfolio.

Currency—Currency exchange rate movements could reduce investment gains or increase investment losses.

Default—Default risk may occur if the issuers of certain bonds become unable or unwilling to make payments on their bonds.

Derivative—Derivatives may be used to create leverage, which could expose the portfolio to higher volatility and/or losses that are significantly greater than the cost of the derivative.

Emerging markets—Emerging markets are less established than developed markets and therefore involve higher risks.

High yield bond—High yield debt securities are generally subject to greater risk of issuer debt restructuring or default, higher liquidity risk, and greater sensitivity to market conditions.

Interest rate—Interest rate risk is the potential for losses in fixed income investments as a result of unexpected changes in interest rates.

Issuer concentration—Issuer concentration risk may result in performance being more strongly affected by any business, industry, economic, financial, or market conditions affecting those issuers in which the portfolio’s assets are concentrated.

Liquidity—Liquidity risk may result in securities becoming hard to value or trade within a desired time frame at a fair price.

Prepayment and extension—Mortgage‑ and asset‑backed securities could increase the portfolio’s sensitivity to unexpected changes in interest rates.

Sector concentration—Sector concentration risk may result in performance being more strongly affected by any business, industry, economic, financial, or market conditions affecting a particular sector in which the portfolio’s assets are concentrated.

Total Return Swap—Total return swap contracts may expose the portfolio to additional risks, including market, counterparty, and operational risks as well as risks linked to the use of collateral arrangements.

General Portfolio Risks

Counterparty—Counterparty risk may materialize if an entity with which the portfolio does business becomes unwilling or unable to meet its obligations to the portfolio.

ESG and sustainability—ESG and sustainability risk may result in a material negative impact on the value of an investment and performance of the portfolio.

Geographic concentration—Geographic concentration risk may result in performance being more strongly affected by any social, political, economic, environmental, or market conditions affecting those countries or regions in which the portfolio’s assets are concentrated.

Hedging—Hedging measures involve costs and may work imperfectly, may not be feasible at times, or may fail completely.

Investment portfolio—Investing in portfolios involves certain risks an investor would not face if investing in markets directly.

Management—Management risk may result in potential conflicts of interest relating to the obligations of the investment manager.

Market—Market risk may subject the portfolio to experience losses caused by unexpected changes in a wide variety of factors.

Operational—Operational risk may cause losses as a result of incidents caused by people, systems, and/or processes.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.