August 2022 / INVESTMENT INSIGHTS

Active Stock Choices Are Key in Volatile Times

Steering through complex dynamics within global equities

Key Insights

- We are using our experience separating the long‑term prospects of stocks from the short‑term narratives that are causing volatility in equity markets.

- Inflation and rising interest rates have resulted in marked underperformance for growth stocks. However, the power of companies that can compound long‑term earnings and cash flows should not be underestimated.

- Geopolitical and macroeconomic uncertainty will remain part of the near‑term environment, but long‑term stock prices are ultimately driven by fundamental earnings power and cash flow generation.

Markets have endured a tumultuous period over the last two years with an extraordinary period encompassing a pandemic, economic recovery, and now, military conflict in Europe. Stocks remain especially volatile given the shocking events occurring in Ukraine, adding uncertainty to an already complex backdrop of rising inflation and monetary tightening.

While the geopolitical and economic backdrop is dominating market movements, we have managed client assets through periods of uncertainty before. We are using our experience separating the long‑term prospects of stocks from the short‑term narratives surrounding equities in what is a highly unusual period. We have always believed, and continue to believe, that fundamental analysis and maintaining our time horizon will deliver the best outcome for our clients.

Regime Shifts and the Growth Versus Value Debate

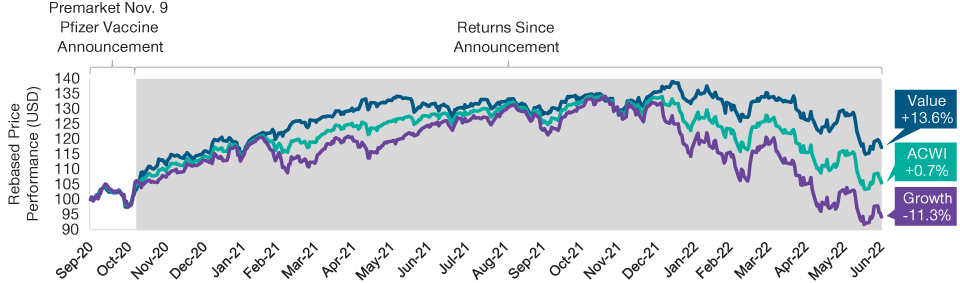

At a headline level, we believe 2022 marks a point of regime change for investors. A marked uptick in inflation and rising interest rates have contributed to equity market weakness and a very distinct change in investor sentiment. (Figure 1).

Stocks Struggle as Inflation Rises and Monetary Policy Tightens

(Fig. 1) Headwinds for growth stocks as inflation and rising rates negatively impact sentiment

As of June 30, 2022.

Past performance is not a reliable indicator of future performance.

MSCI ACWI price returns September 30, 2020, through June 30, 2022. Figures noted in chart (+13.6%, +0.7%, -11.3%) are performance measured from the period after the Pfizer vaccine announcement and ending June 30, 2022.

Source: T. Rowe Price analysis using data from FactSet Research Systems Inc. All rights reserved.

The emergence of inflation catalysts against a backdrop of supply chain constraints and tight labor markets is to be expected, but war has meant that inflation has accelerated faster than expected and is presenting a significant challenge for monetary policymakers.

While the sources of rising inflation are embedded in a complex mosaic of temporary and structural forces, the investor reaction has been clear: a significant repositioning into areas of the market that might benefit from monetary tightening, accelerated further by the consequences of the Russia‑Ukraine conflict, most notably the rise in commodity prices and further supply chain disruption. The shift in focus comes at the expense of long duration growth stocks that have experienced exceptional levels of volatility.

While we have witnessed adverse market conditions from time to time, the sheer size and speed of the market’s rotation has been exceptional. The moves have resulted in a magnitude of underperformance for growth stocks that we did not anticipate, especially in such a short period.

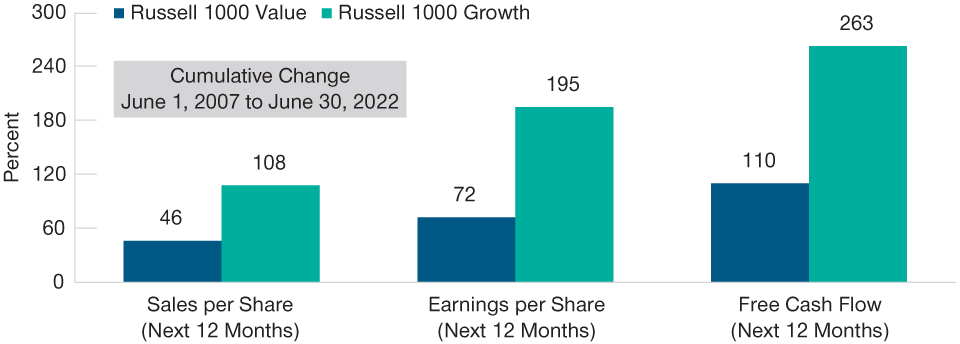

Superior Sales, Earnings, and Cash Flow Growth Have Been Forgotten in the Value Rally

(Fig. 2) Markets should begin to reward growth stocks as better earnings come through

As of June 30, 2022.

Past performance is not a reliable indicator of future performance. Actual outcomes may differ materially from estimates. Shows cumulative change in % terms.

Sources: FTSE Russell (see Additional Disclosures) and FactSet Research Systems Inc. All rights reserved.

Since the global financial crisis (GFC), outperformance of growth stocks has been the dominant feature of equity markets, one accelerated by the coronavirus pandemic. While it is important to recognize that extended valuations and shifting inflation have played a part in the recent correction, it is also crucial to note that the outperformance of growth stocks has been built on a prolonged and persistent fundamental advantage—that of superior sales, earnings, and cash flow growth (Figure 2). Against a backdrop of valuations that have reset lower and the likelihood that inflation will peak as demand destruction takes hold, we believe that stocks delivering superior earnings over the next few years will be prized by investors.

Inflation Uncertainty

While we remain comfortable in our search for stocks with superior earnings prospects and more enthusiastic about valuations after the sell‑off, inflation has clearly emerged as an unpredictable risk in the near term. Alongside monetary tightening bringing down demand, supply chain normalization is crucial to easing pressure points, and while much of the world is learning to live with COVID‑19, the spread of the virus in China has ramifications for an extension of supply chain disruptions and inflation.

Despite legitimate concerns of policymakers and investors alike, we believe that inflation is likely to peak in the coming quarters as interest rates move progressively higher and as policymakers shift their focus away from economic support toward price stability. Demand destruction, together with a normalization of supply chains, may afford policymakers some leeway to move more slowly on monetary tightening into 2023, even with near‑term inflation figures implying aggressive action. This could provide a more positive backdrop for equity markets later in the year.

Balancing Risk and Capitalizing on Attractive Opportunities

In an environment of rapidly changing and powerful economic/geopolitical factors, we acknowledge heightened uncertainty and believe it is a period that requires pragmatism, not overconfidence. The setup for markets changed dramatically in the first half of 2022; we have responded by creating stronger portfolio balance across sectors and re‑underwriting each position in the portfolio. Our focus remains on asymmetric, idiosyncratic, bottom‑up stock picking, primarily in durable “special” growth compounders.

As interest rates have moved meaningfully and supply chain stress proves tougher than expected, the outlook for some of our higher‑valuation companies has deteriorated. This includes some of our tech and internet retail companies that are suffering from factors including recession fears, cost inflation, and challenges obtaining inventory. Amid a huge shift in market sentiment, we strive for setting a higher bar for higher‑valuation, longer‑duration growth stocks but retaining those truly advantaged, disruptive businesses we believe can deliver outsized market share gains and accelerating economic returns over the medium term. We are also seeking to capitalize on market capitulation, where we believe “baby out with the bathwater” scenarios can create attractive entry points for truly special, long‑term growth businesses.

As commodity supply/demand dynamics have tightened, we have reduced our underweight, primarily via diversified exposure within materials, to help the portfolio in an environment of higher inflation and to ensure we are maintaining appropriate portfolio balance. Within materials, we are diversified across metals, chemicals, and packaging, but overall we remain underweight commodities while maintaining an energy underweight.

Elsewhere, our faith in our ability to find good stock ideas in emerging markets remains steadfast. The prospects of higher U.S. interest rates and the subsequent knock‑on impact of funding costs for emerging markets have seen the asset class underperform materially versus developed markets. Countries with higher levels of debt have been impacted most, as was the case during 2013’s “taper tantrum,” despite the reality that the debt structure of most countries has changed materially over the course of the past two decades.

We believe comparisons of corporate earnings growth versus developed markets in 2023 should help, but we have increasingly seen more examples of self‑help by individual companies. During a period of crisis, there are a growing number of examples of companies focusing more intensely on cost control, efficient capital expenditure, and improving shareholder returns. We feel that valuations are also attractive and remain at a discount relative to developed markets.

At this stage of the equity cycle when overall economic growth is more scarce, being able to find profit growth is essential, in both a defensive and an offensive portfolio strategy. Irrespective of the near‑term rotation in markets, fundamental growth in earnings and cash flow remains the most powerful driver of stock prices over the long term, in our view.

While it is important to debate risks and to understand the fundamentals underpinning potential periods of change, we remain focused on idiosyncratic, fundamental stock drivers recognizing, but not being driven by, top‑down macro factors.

Complexity Levels Remain High, But Experience Can Guide Us

After an outstanding period for equity investors since the GFC, higher inflation, tightening liquidity conditions, armed conflict, and the unwinding of pandemic‑era extremes imply higher risks and ongoing market fluctuations going forward. The challenge that many investors have today—separating long‑term expected returns from short‑term narratives and concerns—is not new.

There are obvious concerns around the terrible events happening in Ukraine, but outside of these geopolitical concerns, we believe the world will be more like its pre‑pandemic self than not. While some of the forces that have supported economic recovery have shifted, our base case remains that supply chains will normalize as we learn to live with COVID‑19 and that inflation will peak and eventually ease to a more manageable level.

Importantly, volatility historically has proven to present opportunities, and while we live in highly unusual times, we continue to apply our investment process as we have during other crises. Indeed, we are observing a broader opportunity set than we have for some time. Innovative, high‑growth companies are trading, in our view, at much more reasonable valuations, while idiosyncratic stock ideas not tied to broader market direction are also a focus.

Geopolitical and macroeconomic uncertainty will remain part of the near‑term environment, but long term, stock prices are ultimately driven by fundamental earnings power and cash flow generation. We believe that focusing on this is the best way to help navigate through one of the most complex market environments investors have experienced.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

August 2022 / INVESTMENT INSIGHTS