August 2022 / INVESTMENT INSIGHTS

Attractive Income Bolsters High Yield Bonds

Recent downturn may also offer price appreciation opportunities

Key Insights

- High yield bonds have had a difficult 2022 from a performance perspective, but we are finding unique opportunities in the current environment.

- We believe that much of the value of the asset class is realized by staying invested and benefiting from the compounding effect of its relatively high coupon payments.

- Historically, some of the best opportunities in high yield bonds have come on the heels of pronounced downturns in the asset class.

Like many asset classes, high yield bonds have had a difficult start to 2022 from a performance perspective. In fact, high yield bonds had their worst-ever performance in the first half of a year. In times like these, it is natural for investors to question their investments; however, we continue to view the asset class as a strategic long-term investment and a mainstay allocation as part of a diversified portfolio. Historically, some of the best opportunities in high yield bonds have come on the heels of pronounced downturns in the asset class.

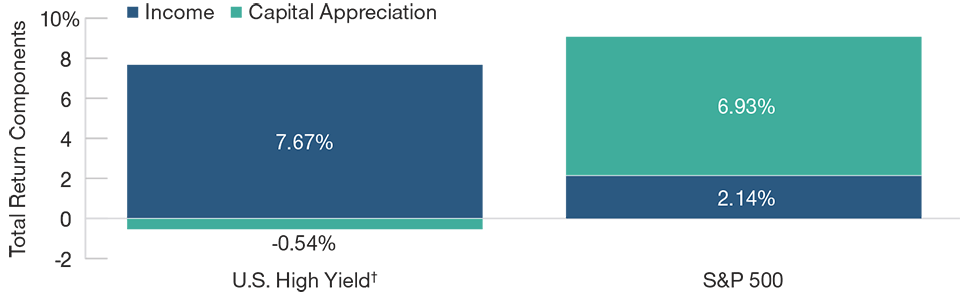

Income Has Been the Key Driver of Long-Term Return*

(Fig. 1) Compounding of coupon payments can be meaningful.

Past performance is not a reliable indicator of future performance.

As of June 30, 2022.

Source: FactSet Research Systems, analysis by T. Rowe Price.

*20 years ended June 30, 2022

†ICE BofA U.S. High Yield Constrained Index.

Income as Key Source of Return

An analysis of historical sources of return shows that, unlike stocks, high yield bonds typically derive their long-term returns from income rather than capital appreciation. Their relatively high and generally consistent coupon payments are a key reason why high yield bonds have historically exhibited lower volatility when compared with equities, and this trend has continued to hold true so far this year. For long-term investors, much of the value of the asset class is realized simply through clipping coupons. Figure 1 uses data over a 20-year time period, which includes both the global financial crisis and the current downturn, so this concept of income as the key driver of returns has held true even during periods that include major market drawdowns.

Capital Appreciation Opportunities

However, opportunities to benefit from additional returns through price appreciation do exist and can serve as attractive entry points for investors. Looking back at historical prices for the ICE BofA U.S. High Yield Constrained Index for January 1, 2010 through June 30, 2022, 87% of the time, the high yield index traded at a dollar price of USD 95 or above. These levels leave little room for capital appreciation; thus, returns during these time periods tend to be heavily driven by income.

However, 8% of the time, the index traded below USD 95, and 5% of the time, it was below USD 90. These discounted levels, though often short-lived, can provide attractive entry points and create more potential for capital appreciation as average dollar prices move back toward par. That said, low dollar price levels typically are accompanied by periods of significant market stress, which can make it more difficult to stomach putting money to work. While it is virtually impossible to accurately predict a market bottom, timing the bottom does not necessarily need to be perfect to benefit from this dynamic.

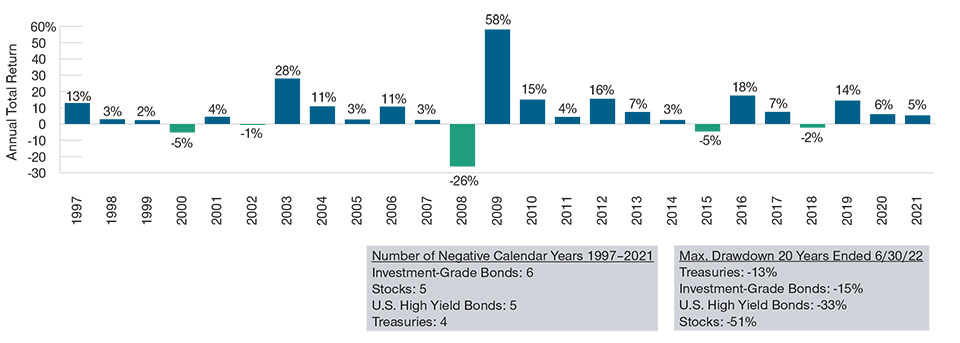

Patience Has Paid Off Historically

Looking at index calendar year returns over the last 25 years, there have only been five years with negative returns and, for investors that had the patience to stay invested, negative return years typically have been immediately followed by outsized positive return years. Though it can be difficult to stay the course during market corrections, remaining invested rather than liquidating positions at what is often the worst time to do so is likely a prudent approach and can potentially better position investors to benefit from future returns.

Low Dollar Prices Present Opportunities

(Fig. 2) U.S. high yield par-weighted* dollar price

Past performance is not a reliable indicator of future performance.

As of June 30, 2022.

Source: FactSet Research Systems, analysis by T. Rowe Price. Gray-box stats provided are based on month-end prices over the time period from

January 1, 2010–June 30, 2022.

*ICE BofA U.S. High Yield Constrained Index weighted by bond face amount outstanding.

Why Now?

The high yield market has been weighed down this year by an evolving narrative that has shifted focus from inflation and rising rates to concerns over slowing growth and the potential for a recession. However, with average high yield bond prices in the 80s, USD, the market is already pricing a fairly large probability of a recessionary outcome. We believe these prices have created an interesting opportunity set for investors if and when things improve. Though the exact timing around when market conditions will improve remains to be seen, there are several things the high yield market has going for it today:

- As rates have risen year-to-date, yields today are higher than they were at the start of the year, and, thus, prospects for income have improved. This should serve as a current benefit to income-oriented investors.

- The year-to-date sell-off has resulted in cheaper valuations and created unique opportunities within the high yield bond market. We have taken advantage of this dynamic and invested in what we view to be good companies at attractive dollar prices across the credit ratings spectrum. We have found compelling opportunities within lower dollar price BBs as well as within higher beta1 parts of the market where risk has sold off indiscriminately.

- Credit fundamentals remain supportive. Credit spreads2 have widened year-to-date, ending the second quarter at levels that are wider than their historical averages. Meanwhile, defaults remain well below their long-term averages as many companies refinanced their debt during the period of extremely low rates, thereby extending maturities. Though defaults may tick slightly higher from here due to inflation and a more hawkish Fed, we expect they will remain well below average for the foreseeable future given the lack of near-term bond maturities.

- Technicals remain supportive as year-to-date outflows industrywide have been met with a relatively quiet new issue calendar. Additionally, yields and bond prices are reaching attractive levels, which may begin to lure investors back into the market.

- The overall quality of the high yield market has improved in recent years, as the proportion of BBs—many with the potential to be upgraded to investment grade—has increased. At the same time, the proportion of CCCs—the segment of the market that is most likely to default—has decrease

Drawdowns Have Been Followed by Strength

(Fig. 3) Historical calendar year returns, U.S. high yield

Past performance is not a reliable indicator of future performance.

As of June 30, 2022.

Source: FactSet Research Systems, analysis by T. Rowe Price. U.S. high yield bonds represented by ICE BofA U.S. High Yield Constrained Index; investment-grade bonds by Bloomberg US Corporate Investment Grade Index; stocks by S&P 500 Index; Treasuries by ICE BofA US Treasury Index.

Though our outlook for high yield is still constructive, risks remain. We continue to look to invest in companies that are better positioned to withstand inflation and rising rates. Also, given the increased risks around the potential for a recession, we continue to stress-test credits for their potential resilience in such an environment.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

July 2022 / MARKETS & ECONOMY