November 2020 / INVESTMENT INSIGHTS

More Fallen Angels Ahead in Europe?

Downgrades have slowed, but indications are that the trend has further to run

Key Insights

- After roughly €70 billion of corporate bonds lost investment-grade status in Europe this year, the pace of ’fallen angels’ has slowed considerably, but risks remain.

- Issuers still looking vulnerable include some in the banking, auto and infrastructure sectors.

- More than a third of the Standard & Poor’s EMEA ratings universe currently remains on negative outlook.

- In the European high-yield market, defaults have been lower than in the US, partly for structural reasons.

- Defaults are likely to continue rising in 2021, depending largely on how well the impact of the coronavirus is managed.

European credit has not escaped the global waves of ‘fallen angels’ in the investment-grade market and defaults in the high-yield market. The question now, for both high-grade and high-yield investors, is whether we are over the worst of it. In both cases, indications are that the story has further to run.

The outlook for fallen angels

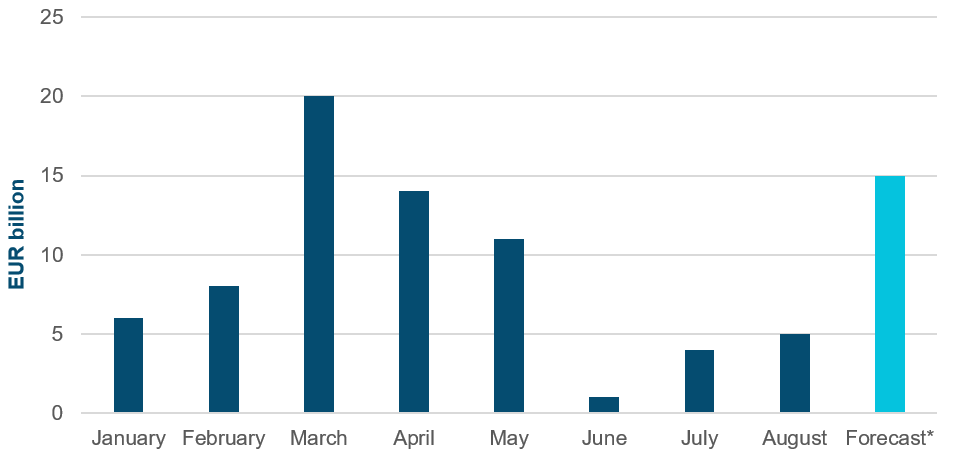

Globally, by the end of September 2020, 56 bond issuers had dropped out of the investment-grade universe, totalling US$216 billion of debt. In Europe, fallen angels totalled about €69 billion by the end of August, according to data from Credit Suisse, with the pace of downgrades declining significantly since mid-year (Display 1).

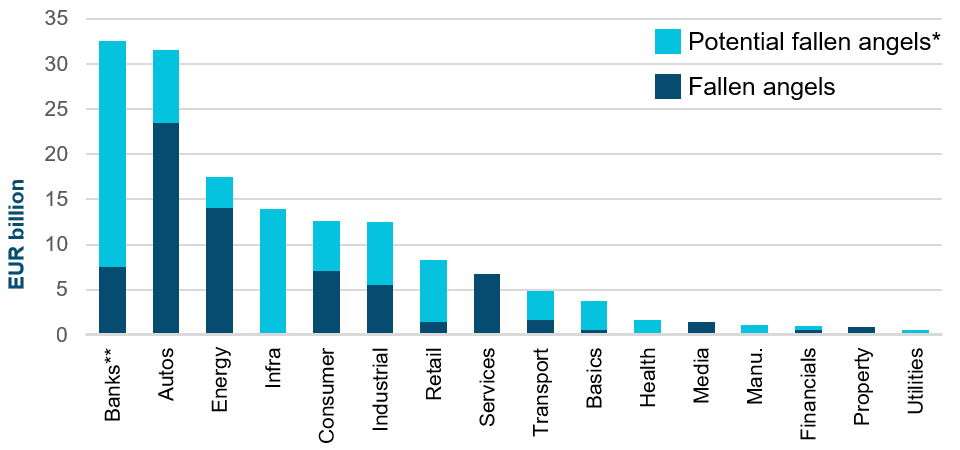

In Europe, the auto sector has been the biggest casualty to date (Display 2) – notably Ford, Renault and Valeo. Other downgrades include Atlantia (the toll road operator associated with the Genoa bridge collapse) and travel and aerospace-related names such as Carnival, Rolls-Royce, IAG and Lufthansa.

Credit Suisse is forecasting roughly another €15 billion of fallen angels this year, which is largely in line with our view. Issuers that are currently on thin ice with the rating agencies include auto maker Nissan, as well as Spanish toll road operator Abertis. Italian sovereign-linked issuers such as banks and utilities saw their near-term risk of fallen angel status reduced when Standard & Poor’s – somewhat surprisingly, in our view – moved Italy’s credit rating to ‘stable’ from ‘negative’ at the end of last month.

One potential swing factor for fallen angel risk is Deutsche Bank, which currently has a chunk of its subordinated debt sitting on the edge of investment grade at Baa3/BBB-. Deutsche had a reprieve from Moody’s Investors Service in early November (from negative to stable) following the publication of its results. If Deutsche did drop a notch into high yield, we estimate that €19 billion of additional debt could fall below the line.

The risk with the outlook for fallen angels – and default rates, for that matter – is that despite the improving trend, much uncertainty remains. While downgrades and the upgrade-to-downgrade ratio have improved since the trough, 37% of S&P’s EMEA ratings universe remains on negative outlook. This signals that there are still risks out there, and that a slower-than-expected recovery in 2021, or a rapid removal of government and central bank support (policy errors), could make this figure volatile.

Display 1: Total downgrades to high yield

EUR billion

As of 31 August 2020

*Year-end forecast

Source: Credit Suisse and Bloomberg Finance LP. Please see Additional Disclosures.

Display 2: Fallen angels by sector

EUR billion

As of 31 August 2020

*BBB- Neg outlook/one HY rating, not including hybrids

**Relevant tiers

Source: Credit Suisse and Bloomberg Finance LP. Please see Additional Disclosures.

The outlook for European default rates

Global default rates are rising and likely to continue into 2021. But we think the full impact may be muted by the significant fiscal and monetary intervention seen from governments and central banks.

According to Moody’s data, the US speculative grade (sub investment-grade) default rate stood at 8.5% end of the third quarter – its highest in 10 years – with a forecast peak of 11% in March 2021. In Europe, defaults have been significantly lower, and Moody’s are not forecasting a very high peak under their baseline assumptions: 5.7% in March 2021 compared with 4.3% at the end of October 2020 (Display 3).

Structural factors may help explain the lower default rates in Europe. For example, there is a higher proportion of BB-rated debt in Europe whereas the US is more of a single-B market. The US has a bigger high-yield oil and gas sector, which suffered from this year’s oil price slump. And from a legal perspective it is somewhat easier to declare bankruptcy under Chapter 7 and Chapter 11 in the US than it is to seek bankruptcy protection in Europe.

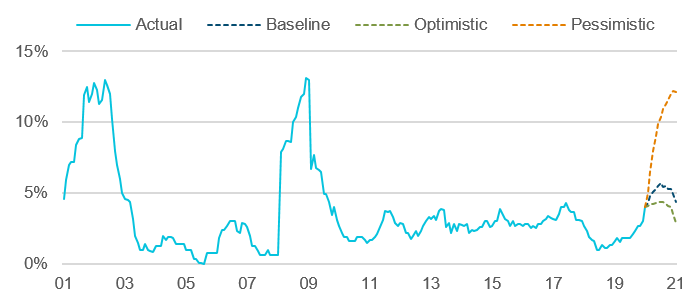

That said, we note that there is a wide range between Moody’s optimistic and pessimistic forecasts – from less than 3% to about 12% by September 2021 (Display 4). The downside is being driven by the outlook for pandemic containment and/or vaccines, and the potential for fiscal stimulus (notably in the US). In our view, both of these outlooks have worsened since the analysis, so we suspect that the baseline might be creeping back up.

Display 3: Moody’s baseline forecast speculative-grade default rates

Trailing 12-month default rates (%)

As of September 30, 2020

Source: Moody’s Investors Service. Please see Additional Disclosures.

Display 4: European speculative-grade default rates (actual and forecast)

As of September 2020

Source: Moody’s Investors Service. Please see Additional Disclosures.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.

November 2020 / MARKETS & ECONOMY

November 2020 / INVESTMENT INSIGHTS