June 2022 / MARKET OUTLOOK

Managing Through Geopolitical Risks

Geopolitics will continue to be a key focus for investors in the second half, reinforcing the importance of diversification

Russia’s invasion of Ukraine has shaken the global political landscape. Beyond the destruction and human suffering inflicted by the war itself, the conflict threatens to worsen hunger in the world’s poorest countries, spur a new arms race, and block cooperation on problems like climate change and nuclear proliferation.

While those shocks could be felt for years, the consequences for global markets were more immediate:

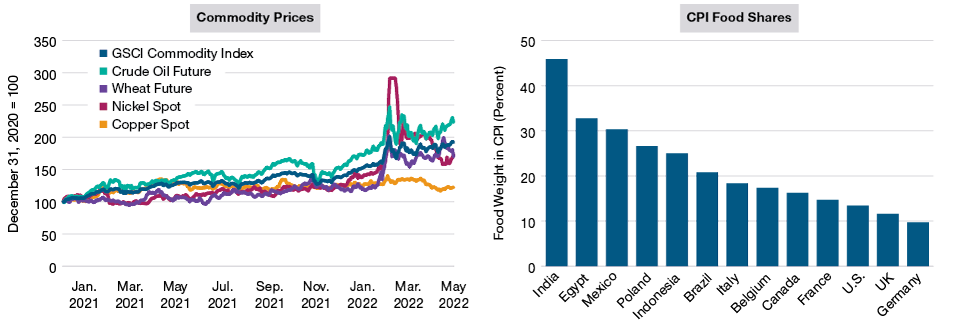

- Economic sanctions on Russia and the closure of Ukraine’s ports on the Black Sea sent prices of key commodities soaring (Figure 5, left panel).

- Fears about the impact on Europe’s economies pushed the euro and the British pound sharply lower against the U.S. dollar.

- Financial sanctions made Russian equities essentially uninvestable for foreign investors and pushed Russia’s foreign currency debt to the brink of default.

The war’s inflationary impact will be magnified in the developing world, where food products typically have a much heavier weight in consumer price indexes than in the developed world (Figure 5, right panel).

The War in Ukraine Is Feeding Commodity Inflation Worldwide

(Fig. 5) Price changes for select commodities and weight of food in national consumer price indexes

Past performance is not a reliable indicator of future performance.

Commodity prices from December 31, 2020, through May 31, 2022. Food price shares as of March 31, 2022.

Sources: Haver Analytics/J.P. Morgan (see Additional Disclosures) and T. Rowe Price analysis using data from FactSet Research Systems Inc. All rights reserved.

“Not only are Russia and Ukraine the breadbaskets of Europe,” Husain says, “but they export many of the chemicals that go into fertilizers and other agricultural inputs around the world.”

The war also has exposed Europe’s overdependence on Russia for oil and natural gas supplies, Thomson says. This will have implications not just for energy security, but for issues related to energy equity—such as consumer subsidies.

Disappointing financial performance in the oil and gas sector had led many equity investors to underweight energy stocks heading into this year, Thomson notes. But the Russian invasion was a wake‑up call.

“I think the market suddenly realized that energy is a strategically important sector and that we’ve probably been undervaluing it,” Thomson says. “A lot of portfolios are feeling the consequences.”

A Boost for Renewable Energy

Like most economic disruptions, the energy shock has the potential to create investment opportunities as well as risks. The transition to renewable energy sources, such as wind and solar, could be one of them, Thomson suggests.

“As the saying goes, the cure for high prices is high prices—in this case, high prices for hydrocarbons,” Thomson argues. “It reduces the relative costs of switching to other sources, so the transition to renewable energy should accelerate.”

Higher oil and gas prices also could spur investments throughout the energy supply chain, not just in renewable projects such as wind and solar farms, Thomson adds. This could include upgrading electrical grids and developing more efficient energy storage technologies—which in turn could boost demand for the raw materials used in those projects.

The Impact of Sanctions

The financial penalties imposed on Russia in response to the invasion could accelerate another longer‑term transition—toward a less centralized global financial system, Husain contends.

The initial round of sanctions included several unprecedented steps, such as freezing Russia’s foreign currency reserves at the Fed and other cooperating central banks and banning some Russian banks from the SWIFT (Society for Worldwide International Financial Telecommunications) financial messaging system.

While these measures have imposed heavy costs on Russia, they also could motivate other countries to seek alternatives to an international payments system dominated by the U.S. and the other major financial powers.

“Some countries may be looking at this and thinking, ‘We need to find another way of moving our money and transacting on a global basis,’” Husain says.

As long as sanctions remain limited to Russia and its closest allies, they appear to pose limited risks to the global economy. But that might not be the case if secondary sanctions were imposed on other countries, particularly China, in response to actions perceived as aiding the Kremlin’s war effort.

“The biggest unknown here for Chinese markets is geopolitical risk,” Thomson says. “If there is a further spillover from Russia’s invasion, and the Western democracies extend sanctions to China, then we would be in a very difficult situation.”

Although secondary sanctions on China appear to be a “tail” risk—i.e., a relatively low‑probability outcome—that risk is likely to weigh on Chinese equity valuations in the second half, Thomson adds.

Download the full 2022 Midyear Market Outlook insights

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.