November 2020 / MARKETS & ECONOMY

Why the Future Now Looks Brighter for Value Investing

Three scenarios that could propel a style rotation back to value

Key Insights

- The extreme valuation dispersion between value and growth stocks stands near historic levels. Economic recovery and improving corporate earnings are likely to benefit cyclical and value areas of the market most.

- A coronavirus vaccine is key to unlocking short-term performance, but long term, inflation is required to deliver a more sustained rotation.

- The narrow leadership and increasingly bifurcated nature of markets has created many opportunities for uncertainty and mispricing to be exploited.

The growth versus value style debate intensified as the dominance of “growth” accelerated during the coronavirus pandemic. Value investing has remained deeply out of favor, but we sense the dynamics are changing and the environment is now looking more favorable for value investing.

Three Factors Shaping the Year Ahead for Value

Vaccine, valuations, and greater focus on fiscal spending will favor value areas of the market

When regime changes happen, they are often swift and dramatic with large stock price movements, so positioning early is important. With many investors currently not positioned for a style rotation, we examine three scenarios that could favor value investing and help investors consider their allocations.

Post‑Coronavirus Economic Recovery Set to Drive Cyclical Stock Performance

We believe the global economy is currently in a mini “W‑shaped” recovery as we progress through the coronavirus pandemic. A brief recovery after the first wave has been interrupted by a resurgence in cases in the U.S. and Europe with PMIs1 softening. However, this is likely to improve as we enter the first quarter of 2021.

Virus cases could fall, or at least become more manageable, while recent news from Pfizer and Moderna of potential vaccines, along with others in the pipeline, could accelerate our way out of this pandemic. Initial optimism is exceedingly high right now, and that could fade, but ultimately, a vaccine that works effectively will help drive economic recovery, and that would favor cyclical parts of the market.

China is a great example of how a recovery scenario could potentially play out globally. China has had much more success in suppressing the virus, and its economy is benefiting. Consumer spending, car sales, and economic growth have all bounced back strongly from the depths of the pandemic back in March.

Globally, some of the most sensitive sectors to the pandemic have been industrials, materials, energy, real estate, and transportation. Year‑on‑year earnings comparisons from March 2021 onward are, however, likely to look much more favorable.

New Political Dynamics Shape a Favorable Fiscal and Monetary Backdrop

The victory of Democratic candidate Joseph Biden in the U.S. presidential election brings with it a range of potential value‑positive policy measures. Among the possible policy actions in play are the easing of trade uncertainty (reestablishing a pillar for global growth), increased fiscal stimulus, a potentially weaker U.S. dollar, and more substantial reflationary policies.

We expect President‑elect Biden to prioritize additional fiscal spending to stimulate the economy as it recovers from the steep downturn caused by the coronavirus pandemic. We also anticipate increased infrastructure spending alongside the possibility of higher corporate taxes. Higher taxes historically have been more detrimental to areas within the growth complex, however.

While a Biden administration is seen as supportive of corporate tax increases, it is far from certain that these would be enacted. There are many hurdles ahead for a Biden presidency, including a split Congress and the uncertain balance of the Senate, which may dampen prospects for spending and policy changes in the near term.

Arguments for more unconventional policy to bolster economic growth have also gained traction. This includes those who favor central bank balance sheets being put to work to provide tangible income for consumers in the form of fiscal handouts. We have already seen this approach, in part, to deal with the coronavirus pandemic.

Modern Monetary Theory, which holds that governments should use fiscal policy to generate full employment, is one variation on this line of thought.

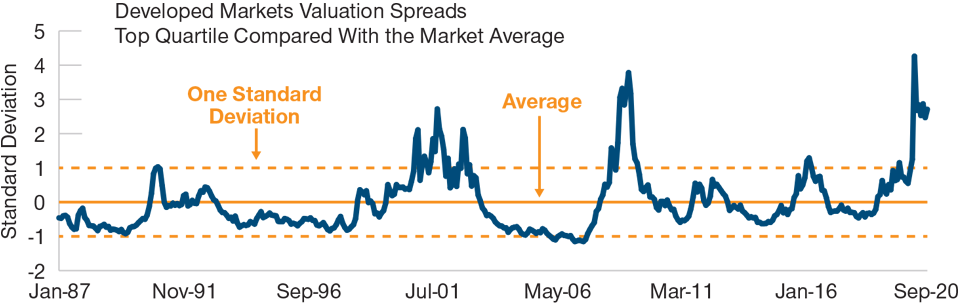

Valuation Spreads Between Value and Growth Remain Near Historic Levels

When spreads widen, opportunities arise for value investors to exploit

January 1987 to September 2020.

Source: Empirical Research Partners Analysis.

Nobody has yet demonstrated that delegating monetary policy to elected politicians will bring about better economic outcomes than the current method of allowing central banks to manage it, but helicopter money has gained traction. The gradual erosion of central bank independence means that the current environment is probably more conducive to helicopter money than it was just a few years ago.

Shifting Market Dynamics Put Focus on Valuations

Value stocks have come under huge pressure as economic uncertainty has prompted investors to shorten their time horizons, pile into secular winners, and avoid cyclicals. Fear and uncertainty have also meant investors have favored well‑understood growth stories during the recovery rally without regard to valuation.

However, the market’s extreme and singular focus on secular growth and an extreme aversion to cyclical risks have contributed to the narrowing in market leadership. The FAANGs2 have become the market. This market concentration has become a concern, and we expect a broadening away from this narrow group of mega‑cap market leaders.

With the MSCI World Value Index having a meaningful overweight to financials, energy, and utilities and underweight exposure to technology and consumer discretionary—value sectors have the potential to benefit from an economic recovery and any revision to the overconcentration profile currently evident.

This is not to call a turn in the growth/value performance cycle, especially a sustainable reversion. We are also not signaling a uniform downturn for growth stocks. Indeed, many with the best growth profiles will likely continue to generate high free cash flow margins.

However, the idea that today’s biggest companies—primarily U.S. technology companies—will continue to dominate the next decade should be viewed with caution. Seldom do the same companies, or even economies, manage to sustain such dominance.

Better Times Ahead

Although many of the trends driving growth outperformance may endure, we believe value stocks offer significant upside potential at this time. The maturity, narrowness, and magnitude of the current growth cycle, along with the gathering debate about the scope for a more inflationary and interventionist world, suggest that a change may be afoot. Key to unlocking short‑term performance is a coronavirus vaccine, while a more prolonged style rotation will likely need inflation.

Importantly, with valuation spreads between value and growth currently at extreme levels, a sustained regime change is not essential to see improved investment returns for value stocks. Crucially, we believe that the quality and quantity of the opportunity set available to value investors right now is as compelling as it has ever been.

T. ROWE PRICE BEYOND THE NUMBERS

The Art of Value—Pinpointing the Underappreciated

Trying to deliver alpha in value areas of the market has been difficult over the last decade, as growth outperformance has been so strong. But we believe in the power of value investing, which has, at times, meant adopting the contrarian trade.

Our focus has always been on finding companies that we believe are trading below their intrinsic values, usually because of some short‑term dislocation that our fundamental research suggests could be resolved.

We are not looking for the cheapest stocks, but instead for the most compellingly valued names relative to their long‑term prospects. For example, banks have faced deep secular challenges ever since the global financial crisis back in 2008–2009. With unprecedented suppression of interest rates and quantitative easing (QE), banks have been deeply out of favor.

But our analysis paints a much better picture for the sector. For some banks, the secular headwinds remain, but many now have much better capital ratios and less leverage on their loan books, with some also actively looking to increase their loan growth going forward. Even if we remain in this ultralow interest rate environment, which is highly likely in the near term, we believe there are still areas within the sector that offer opportunities, especially those with investment banking or asset management arms.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources’ accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction.