30 June 2021 / U.S. FIXED INCOME

Treasury Yields Likely to Remain Range-Bound

Peaking economic data should contain yields for the near term.

Key Insights

- U.S. Treasury yields appear to have peaked for now and are likely to be range-bound for the next few months as economic growth decelerates.

- Longer-term yields are probably capped by economic data that recently have not exceeded expectations, ending the strong yield curve steepening trend.

- We likely will not know the true nature of the economy until this fall when jobless benefits lapse, kids are back in school, and parents return to work.

With economic growth still very strong but decelerating, U.S. Treasury yields appear to have peaked for now and are likely to be range-bound for the next few months. Longer-term yields are probably capped by economic data that recently have not exceeded expectations and by declining inflation momentum, bringing the strong yield curve steepening of the last several months to an end. Perhaps most importantly, Federal Reserve officials have begun to discuss talking about tapering their bond purchases, indicating that the central bank may be less willing to let the economy run hot than we expected. We anticipate that the 10-year Treasury yield will likely stay in the 1.45%–1.90% range over the next three months.

U.S. Economic Data Peaking

Growth expectations remain very firm with 5%–6% quarter-over-quarter gross domestic product expansion expected through this year and 4% in 2022 (measured as fourth quarter 2022 versus fourth quarter 2021), which is considerably stronger than in any period after the global financial crisis (GFC) of 2008–2009. U.S. economic data are currently peaking, however, and the data received in the second quarter have only been just meeting expectations. This dynamic has supported the trading range for Treasuries, with the 10-year yield generally trending between 1.50% and 1.75% since late March.

Survey-based economic data such as purchasing managers’ indexes (PMIs)—known as “soft data”—remain buoyant. On the other hand, the reopening-related combination of high prices, low inventories, long delivery times, and underwhelming hiring has been causing some dissonance with the strong headline figures. T. Rowe Price’s economics team has downgraded their convictions on global and U.S. growth given that the recent lofty pace of expansion will likely be difficult to sustain.

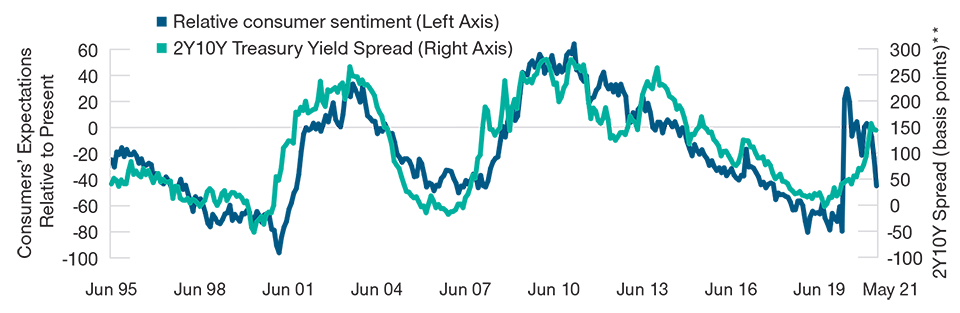

Yield Curve Has Tracked Consumer Mindset

(Fig. 1) Relative consumer sentiment* versus yield curve

As of May 31, 2021.

Past performance is not a reliable indicator of future performance.

Sources: The Conference Board for consumer sentiment indexes, Bloomberg for Treasury yields.

*Consumer expectations index level minus consumer confidence present situation index level.

**A basis point is 0.01 percentage point.

Inflation High but Stabilizing

Increases in the consumer price index (CPI) are likely to run at or above 3.5% into 2022, but we expect CPI gains to also peak at high levels in the second quarter. Inflation expectations have stabilized along with leading indicators of actual inflation, such as rents, energy prices, and surveys of prices paid. We tend to believe that, similar to growth, inflation will stay firmer for longer than most forecasters expect, as the post-GFC consensus “lowflation” mindset is hard to break. Also similar to growth, we will not have good visibility into longer-run inflation for the next few months. Market expectations for inflation, measured by Treasury inflation protected securities (TIPS) breakevens,1 have slipped from recent highs.

The TIPS market is signaling that inflation expectations may have topped out. Investments in inflation protected products are heavily skewed toward passive exchange-traded funds (ETFs), making them a meaningful factor affecting the balance between supply and demand in the market for TIPS and inflation swaps.2 Shares outstanding of the large passive ETFs appear to be near a peak or perhaps declining, and pricing of inflation swaps relative to consensus inflation expectations appears stretched. While this was not a deterrent for TIPS breakevens heading into an accelerating second quarter, we believe it holds more weight going into a decelerating third quarter.

Policymakers Thinking About Talking About Tapering

We expected the Fed to wait as long as possible before discussing the eventual tapering of bond purchases, so we were somewhat surprised when key Fed officials said that policymakers had begun “thinking about talking about tapering” even before the June Federal Open Market Committee meeting. The Fed is likely attempting to manage inflation expectations through the summer as they await clarity in the data this fall. This, at least temporarily, damages the Fed’s credibility on letting inflation run higher than the 2% target3 to offset past inflation undershoots and is likely to make it difficult for Treasury yields to exceed the top end of recent rate ranges.

The Fed talking about tapering focuses market expectations for the timing of the first rate hike because the sequence of taper to liftoff is well engrained in market consensus. The market widely anticipates that tapering will begin about six months after policymaker discussions start, followed by approximately 12 months of gradually reducing bond purchases before the first rate hike. Additionally, talking taper now solidifies the market’s current expectations for the next cycle of rate increases, including the terminal rate where the Fed pauses, which limits the upside potential in long-term yields because an earlier start to tightening would limit the magnitude of rate hikes.

Adding Some Duration Exposure

In response to our evolving outlook, we added some duration4 to the core bond strategy while keeping it slightly short of the benchmark, given that yields are near the lower end of the expected range. In the inflation protected strategies, we have less conviction in further widening of TIPS breakeven spreads but still have positioning based on a somewhat less hawkish view of the Fed. In both strategies, we removed positioning that would have benefited from a steeper yield curve. It is important to note that inflation does not necessarily mean that investors should shed duration, given that inflation can weigh on growth.

Factors That Could Impact Outlook

We continue to monitor several key factors that could cause us to modify this positioning. Signs of an increase in growth expectations, whether from political negotiations supporting a larger-than-expected fiscal stimulus package or simply hard data consistently outperforming expectations, could indicate that yields may move higher in the near term. Indications of a delay in Fed policymakers solidifying their tapering plans could have similar effects.

The interaction of wages and aggregate prices is another key indicator that could affect positioning in the core bond and inflation protected strategies. So far, consumer price inflation has run much higher than wage growth, which has implications for both consumer spending and economic growth. Aggregate prices are rising, but aggregate wage growth has not kept pace—at least not yet. If wages rise to meet prices, the resulting longer-term inflation could lead us to shorten duration. If prices fall to meet wages as consumers cut back on spending, we would tend to lengthen duration, with all else equal.

True Nature of Economy Likely Not Clear Until the Fall

We likely will not know the true nature of the post-pandemic economy until this fall when unemployment benefits lapse, kids are back in school, and many people go back to work in person. The Fed is trying to manage through this transition period, but in our view, policymakers are reducing their “run it hot” credibility in the process. More clarity should arrive this fall when fourth-quarter data come into view. In the longer term, we continue to believe yields will likely push higher amid a very strong economic backdrop.

What We're Watching Next

The price of the U.S. dollar relative to other major currencies can affect U.S. inflation because a weaker dollar makes imported goods more expensive. We are monitoring the dollar’s reaction to the Fed’s signals about tapering its bond purchases and eventually moving toward rate hikes, which, with other factors equal, could support the dollar.

IMPORTANT INFORMATION

This material is being furnished for general informational purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, and prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

Canada—Issued in Canada by T. Rowe Price (Canada), Inc. T. Rowe Price (Canada), Inc.’s investment management services are only available to Accredited Investors as defined under National Instrument 45-106. T. Rowe Price (Canada), Inc. enters into written delegation agreements with affiliates to provide investment management services.

© 2023 T. Rowe Price. All rights reserved. T. ROWE PRICE, INVEST WITH CONFIDENCE, and the bighorn sheep design are, collectively and/or apart, trademarks or registered trademarks of T. Rowe Price Group, Inc.

22 July 2021 / INVESTMENT APPROACH

Steve Bartolini is a portfolio manager in the Fixed Income Division. He manages the US Core Bond Strategy and US Investment Grade Core Bond Strategy. Steve is a member of the Investment Advisory Committees for the New Income Fund, Inflation Protected Bond Fund, Limited Duration Inflation Focused Bond Fund, QM U.S. Bond Index Fund, and Total Return Fund. He also is a member of the Investment Advisory Committees for the U.S. Treasury Funds, Inc., and Retirement Funds, Inc. He co-heads the Global Interest Rate and Currency Strategy team and is a member of the portfolio strategy team for the Core/Core Plus bond strategies. He also is a member of the Asset Allocation Committee. Steve is a vice president of T. Rowe Price Group, Inc., T. Rowe Price Associates, Inc., and T. Rowe Price Trust Company.

Mike Sewell is a portfolio manager in the Fixed Income Division. He is the lead manager for the US Inflation Protected and US Treasury Strategies. He is the president and chairman of the Inflation Protected Bond and the Limited Duration Inflation Focused Bond Funds; an executive vice president and chairman of the U.S. Limited Duration TIPS Index Fund; an executive vice president of the U.S. Treasury Funds, Inc., and Index Trust, Inc.; and a vice president of the Fixed Income Series, Inc., Short-Term Bond Fund, and Exchange-Traded Funds, Inc. Mike is the chairman, the cochairman, and a member of the Investment Advisory Committees of the U.S. Limited Duration TIPS Index Fund, U.S. Trust Limited-Term Index Funds , and U.S. Treasury Funds, Inc., respectively. He also is a member of the Global Interest Rate and Currency Strategy team. Mike is a vice president of T. Rowe Price Group, Inc., and T. Rowe Price Associates, Inc.