March 2024 / INVESTMENT INSIGHTS

The case for value

Reasonable valuations could provide an upside surprise

Key Insights

- U.S. growth stocks have significantly outperformed value stocks over the past year, but we believe this dynamic could shift as near-term challenges fade.

- T. Rowe Price’s Asset Allocation Committee has moved to overweight U.S. value stocks, as earnings expectations appear to leave room for an upside surprise.

Over the past year, U.S. growth stocks have significantly outperformed value stocks, driven by the so-called Magnificent Seven.1 Given this uneven market advance, many investors may wonder if growth stock dominance will continue or if a broader market rally, led by value stocks, could be on the horizon.

Elevated valuations for U.S. growth stocks reflect high earnings growth expectations for the sector. More subdued earnings expectations for value stocks leave room for an upside surprise. This difference in expectations is particularly noticeable at the sector level (Figure 1).

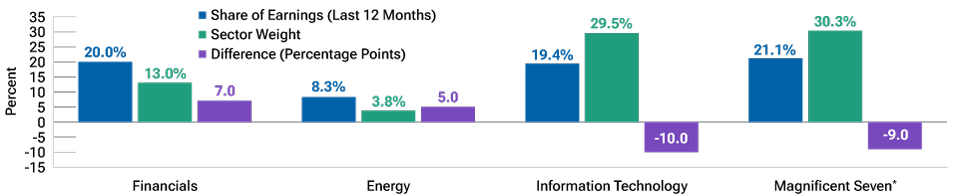

Low expectations for financials and energy sectors

(Fig. 1) S&P 500 Index sector weights versus share of index earnings

Data represent the 12-month period ended February 20, 2024.

Past results are not a reliable indicator of future results. Actual outcomes may differ materially from forward estimates.

Sources: T. Rowe Price analysis using data from FactSet Research Systems Inc. All rights reserved. S&P 500 Index. GICS. See additional information.

* The “Magnificent Seven” stocks are Apple, Alphabet, Amazon.com, Meta, Microsoft, NVIDIA, and Tesla. The specific securities identified and described are for informational purposes only and do not represent recommendations. Not representative of an actual investment. There is no assurance that an investment in any security was or will be profitable.

On a sector-weight basis, expectations for the extremely growth‑oriented information technology sector are meaningfully elevated relative to the tech’s share of S&P 500 Index earnings. Meanwhile, sentiment toward the financials and energy sectors—both heavily tilted toward value—is notably depressed.

Despite near-term challenges, a steepening yield curve could drive up profits in the financials sector if the Federal Reserve cuts short‑term rates. Peaking oil rig productivity and/or further elevated tensions in the Middle East could push oil prices higher, boosting energy earnings.

U.S. value stocks also could benefit from higher real (after inflation) interest rates. The near-zero real interest rates seen from 2008 to 2019—the post-global financial crisis period commonly referred to as the “New Normal”—were actually quite abnormal relative to historical norms, and a repeat of the extremely accommodative monetary policy that held rates so low for so long appears unlikely going forward.

While stock valuations, represented by price-to-earnings (P/E) ratios, have tended to fall when real rates are high, value stocks typically have fared better than growth stocks in such environments (Figure 2). Still, it is important to note that recent excitement about artificial intelligence has made U.S. growth stock valuations seemingly impervious to the impact of higher interest rates.

(Fig. 2) Real rate impact on stock valuations

(Fig. 1) S&P 500 Index sector weights versus share of index earnings

Data represent the 10 years ended January 2024.

Past results are not a reliable indicator of future results. Actual outcomes may differ materially from estimates.

Sources: T. Rowe Price analysis using data from FactSet Research Systems Inc. All rights reserved. Bloomberg Finance L.P. and Russell Indexes. See additional information.

NTM = next twelve months

* The artificial intelligence excitement began in late 2022, with the launch of ChatGPT.

U.S. value stocks have trailed growth stocks considerably over the past year, and we believe this dynamic could shift. As a result, the Asset Allocation Committee recently moved to an overweight position in U.S. value equities.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

March 2024 / INVESTMENT INSIGHTS

March 2024 / INVESTMENT INSIGHTS