July 2023 / INVESTMENT INSIGHTS

There are Reasons to Like European Bank Bonds

Attractive valuations and resilient fundamentals support the sector

Key Insights

- European banks and financials have underperformed, but we believe fundamentals are solid and that current valuations do not reflect the banking sector’s underlying resilience.

- European banks do not share the same risks as US regional banks, in our view, as the regulation, structure and level of market concentration is different.

- Technical factors should turn more favourable for European financials in the second half of this year and support the outperformance of the sector versus the rest of the market.

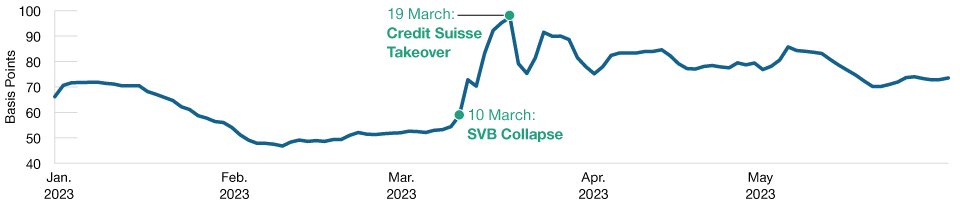

The European banking sector has been in the eye of the storm these last few months following the rescue merger of Credit Suisse with UBS and the write‑down to zero of its additional tier‑one bonds. These events, together with the high‑profile failures of some US regional banks, have undermined sentiment and led to the underperformance of European financials versus other sectors in the European investment‑grade corporate bond universe. We believe that the European banking sector’s fundamentals are solid, however, and that current valuations do not reflect its underlying resilience. Against this backdrop, we are finding attractive opportunities in the sector, which represented our largest overweight in the European Corporate Bond Strategy as of 31 May 2023.

European Bank Credit Spreads Are Attractive

European bank bond spreads initially widened out following the collapse of Silicon Valley Bank (SVB) and the rescue merger of Credit Suisse. On a relative basis, European financials have lagged nonfinancial sectors, such as industrials and utilities, for some time now (Figure 1). While some of this underperformance has been recouped, we believe there is more normalisation to go, especially considering the European banking sector’s solid fundamentals and likelihood that technicals turn more favourable in the second half of this year, which we detail later in the piece.

European Financials Underperform

(Fig. 1) Option‑adjusted spread differential between financials and nonfinancials

From 3 January 2023 to 31 May 2023.

Past performance is not a reliable indicator of future performance.

Index = Bloomberg Euro Aggregate—Corporate Bond Index.

Source: Bloomberg Finance L.P.

Why European Banks Are Different to US Regional Banks

One of the factors driving the underperformance is the belief that European banks carry similar risks to US regional banks, but there are key differences. First, is the level of concentration—Europe is much more concentrated than the US, where there are more than 4,000 banks.1 Generally speaking, markets with fewer banks are less susceptible to deposit flight as there are fewer options to move to.

Second, is structure—Europe is a collection of different national banking markets, and within each national market, champions tend to dominate. Their business mix and deposit base is typically broad, unlike in the case of SVB, where the deposit base was heavily concentrated in a particular sector. Furthermore, even though these European banks may be small in scale, from a national perspective, they may be one of the largest and could even benefit from a flight to quality. By contrast, a US regional bank is still likely to be small on a national basis, which leaves them potentially more vulnerable to deposit flight risk if confidence gets hit.

Third is regulation—Europe is subject to tighter rules than US regional banks. Europe, for example, has adopted a regulation known as ‘interest rate risk in the banking sector.’ This effectively limits European banks from having too much exposure to held‑to‑maturity investments because they are marked to market and their impact on capital from changes in fair value is capped. European banks also engage in more interest rate hedging because of this legislation.

Technical Factors Expected to Turn More Favourable

Turning attention to technicals, we expect these to turn more favourable for the financial sector vis‑à‑vis other sectors. First, banks frontloaded their issuance at the start of the year. This, combined with the likelihood that loan books will not grow as much due to the economy slowing down, means there is less need for banks to raise new debt in the second half of 2023. By contrast, nonfinancial sectors have issued less debt last year and during the first six months of 2023 so we expect them to issue more during the second half of this year to meet their debt funding needs. Nonfinancial sectors, such as industrials and utilities, will also lose a natural buyer when the European Central Bank starts to unwind its corporate bond programme from July. By contrast, financials were never part of the bond‑buying programme. In all, we believe these supply and demand dynamics should support the outperformance of financials versus the rest of the market in the second half of the year.

Importance of Security Selection

While we like the European financial sector, not all areas are attractive, and careful security selection is still required. For example, we are wary of banks with particularly high exposures to commercial real estate. By contrast, we like Icelandic banks, as they broadly have sound capital and liquidity positions and should benefit from solid economic growth this year as the tourism sector recovers. Elsewhere, we also find select Spanish banks attractive as the sector is highly concentrated and should benefit from a large share of housing loans being priced on variable rates.

Heading into the second half of the year, we feel that the conditions are ripe for the European financial sector to outperform peers as technicals look set to turn more favourable. Attractive valuations and broadly resilient fundamentals also support the sector, which is especially important in the face of an economic downturn and the challenge of higher rates.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.