November 2021 / MULTI-ASSET STRATEGY

Benchmark Aware or Agnostic?

A practical guide on which investment approach may best suit you.

Key Insights

- There are various investment techniques to pursue predefined return and risk objectives. For multi-asset investors, the choice starts with the role of the benchmark in portfolio construction.

- A benchmark-aware approach provides more transparency on portfolio outcomes as most of the portfolio’s risk and return comes from the benchmark.

- A benchmark-agnostic approach can narrow the possible outcomes around the desired objectives but is more dependent upon the skills of the investment manager.

Trends in Multi-Asset Investing

While investors may not have changed their objectives much over the years, asset managers have evolved the techniques they use to deliver on those objectives. For investors who look for a superior return than bonds but lower risk than equities, multi-asset solutions come in handy with a diversified profile that can be customized to any desired risk targets in between those of equities and bonds. To be more explicit on the objectives of the portfolio, a benchmark made of x% of equities and y% of bonds was typically used. At first, the original intent of this benchmark was clear: It was an investible version of defined return and risk objectives over a certain time frame. For example, a 60% equity and 40% bond benchmark has been used by investors looking for a 5% to 7% return target with a 6% to 8% volatility level. In practice, a portfolio manager is likely to measure his or her success on how well the portfolio is doing relative to this benchmark instead of the nominal risk and return objectives. This is the benchmark-aware approach. However, some investors might still be evaluating the results compared with the nominal risk and return objectives. This created some misalignments for some when the investible benchmark’s results were far from the anticipated numerical risk and return objectives. A solution has been developed to skip the definition of an investible benchmark (the so-called 60/40) and to only focus on the desired risk and return numbers. This is the benchmark-agnostic approach.1

While an investor might be clear on his or her risk and return objectives, the question he or she needs to ask their manager is: “Is a benchmark-aware or a benchmark-agnostic approach better to meet my objectives?” In this note, we aim to provide some guidance on how to evaluate the pros and cons of each approach. Like everything in life, there is no “one size fits all” answer. The answer is: It depends on each investor’s experiences and preferences.

Value Added From a Multi-Asset Manager

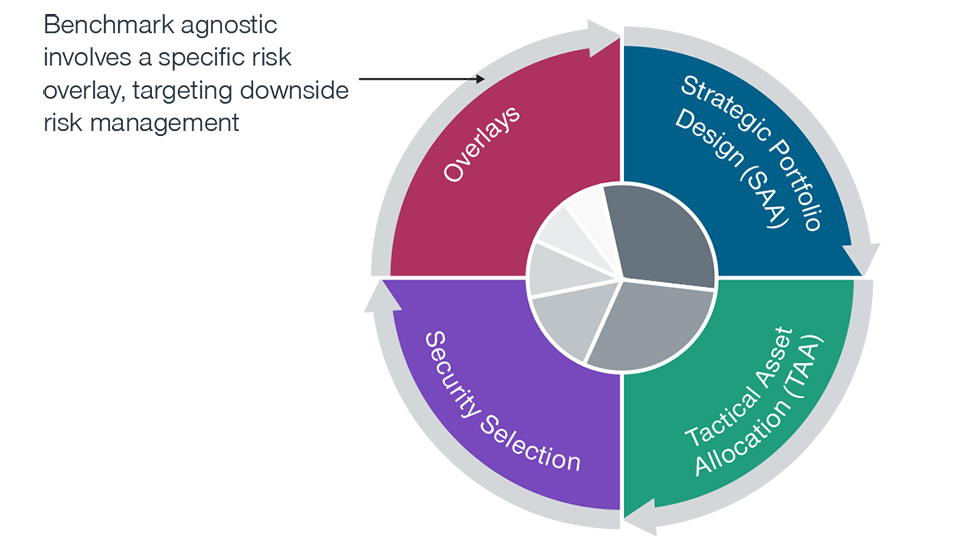

The usual task of global multi-asset portfolios is to try to deliver a customized risk-adjusted return in a consistent manner. Multi-asset managers typically deliver potential value added, or alpha, through multiple sources with appropriate risk management strategies a key consideration throughout the investment process. In Figure 1, we illustrate the main building blocks of an actively managed global multi-asset portfolio, showing the major sources of potential added value from a multi-asset manager.

Global Multi-Asset Portfolios

(Fig. 1) Investment process and potential sources of value added

Source: T. Rowe Price. For illustrative purposes only.

We begin with the top-right quadrant, the strategic design of the portfolio that in turn leads to an appropriate strategic asset allocation (SAA). An important first step will be the choice of asset classes that can be included. Traditionally, many investors opted for a relatively straightforward combination of global stocks, bonds, and cash. A typical strategic asset allocation design would often be framed around a mix of equities and bonds. For example, 60% equity and 40% bond is the classic “global balanced” portfolio. More recently, investors have been comfortable adopting a wider set of strategic assets that includes alternatives such as real assets, real estate investment trusts, commodities, and hedge funds.

At this step of the process, it is important for the client to think very clearly about the portfolio’s investment horizon, its longer-term goals, important guidelines or constraints, and risk tolerance and how these might be represented by a particular choice of SAA. Together with the portfolio manager, the client should consider the implications of varying the SAA parameters using a range of analysis such as historical simulations or more forward-looking scenarios. Indeed, empirical research demonstrated that the SAA represents the dominant driver of any multi-asset portfolios’ risks.

Moving down to the next quadrant in Figure 1, we have tactical asset allocation (TAA). TAA is that part of the investment process where the portfolio manager moves away from the agreed strategic asset allocation in order to try to take advantage of perceived relative valuation opportunities over time horizons that are shorter than the investment horizon of the portfolio. For example, the TAA decision within equities might be to overweight the emerging market versus developed market equities. In the absence of leverage, a decision to tactically overweight an asset class necessarily means the portfolio will be tactically underweight in some other asset class (or classes). While TAA decisions typically take center stage in any multi-asset portfolio review, their impact varies significantly depending on the flexibility that one manager may have. Flexibility in the implementation of the TAA decisions is a key difference between the benchmark-aware and the benchmark-agnostic approaches.

The third quadrant of Figure 1 refers to security selection. This is an important quadrant as implementation may vary significantly from one manager to another. There are some multi-asset managers, including some of the more quantitative funds that are macro driven, focusing only on the asset allocation decision. Typically, they will employ passive or indexed funds for each bond or equity sleeve within the global portfolio, limiting the contribution of security selection. However, we believe that this excludes an additional, independent source of potential alpha for the global multi-asset portfolio—actively managed security selection. Investors might consider choosing a global multi-asset manager that also has a strong bottom-up stock-picking capability. Our specialist portfolio managers oversee and manage each sleeve of the multi-asset portfolio, with an emphasis on actively managed stock or bond selection that should benefit from T. Rowe Price’s experienced team of global credit and equity analysts.

The three quadrants of Figure 1 that we have considered so far—strategic asset allocation, tactical asset allocation, and security selection—are the building blocks for a traditional “benchmark aware” global multi-asset portfolio. In practice, the preferred strategic asset allocation is likely to define the largest part of overall portfolio risk, say 80 % to 85%, with around 15% to 20% of portfolio risk determined by tactical asset allocation and security selection decisions.

The final quadrant of Figure 1 represents the portfolio overlay that is a key characteristic of the “benchmark agnostic” manager. This typically involves a risk overlay that aims to limit portfolio drawdown or control the overall volatility. This may be achieved cheaply and efficiently via index futures, foreign exchange, and/or options. These are employed to quickly raise or lower exposure to a specific market within the global portfolio without disturbing underlying holdings. The overlay decision is another potential source of portfolio return: Your portfolio wins by not losing. Its contribution is better evaluated in the context of risk attributes rather than return.

Benchmark-Agnostic or -Aware Strategy: What Can Investors Expect?

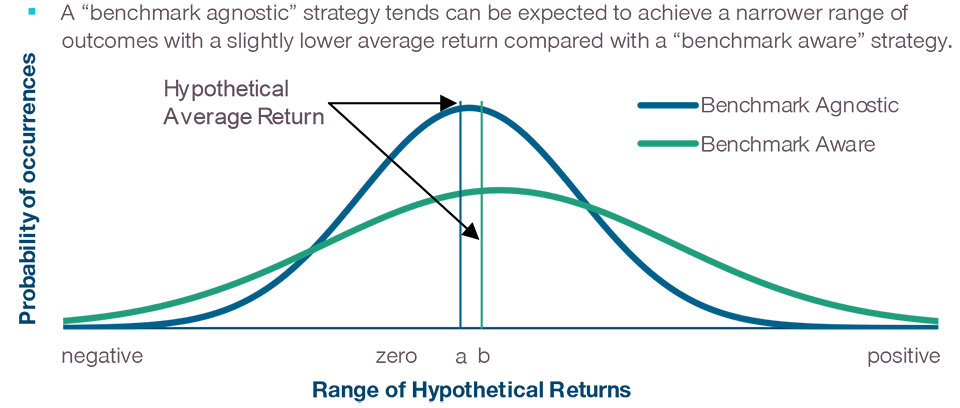

In Figure 2, we compare illustrative return distributions for two hypothetical portfolios. Both hypothetical portfolios have the same risk and return objectives. However, their investment approaches differ. One portfolio follows a benchmark-agnostic strategy that targets a long-run return of “cash + x%” regardless of benchmark performance (blue line). The second portfolio’s mandate specifies an agreed benchmark based on strategic asset allocation weights that aim at generating the same cash + x% return under certain assumptions (green line).

Objective of the Portfolio Mandate—What to Expect?

(Fig. 2) Illustrative return distribution

Source: T. Rowe Price. This analysis is hypothetical and for illustrative and informational purposes only. The illustration is not based on actual portfolios nor does the illustration represent actual returns. Actual outcomes and returns may differ materially from the illustration provided.

In practice, the portfolio return distribution for the benchmark-agnostic strategy can be expected to achieve a narrower range of outcomes than the more constrained benchmark-aware portfolio. Thus, it is shown in Figure 2 as being rather more peaked in the neighborhood of the mean. We have also portrayed the benchmark-agnostic hypothetical portfolio as having a slightly lower average return than the benchmark-aware portfolio. This is because in a scenario where markets are rallying, once the target return of cash + x% has been achieved, there will be an incentive for the benchmark-agnostic manager to begin dynamically reducing risk at the margin.

The main payoff or potential benefit from the benchmark-agnostic hypothetical portfolio is the much-reduced left-hand tail risk or chance of a large negative outcome and loss of wealth. This is illustrated in Figure 2 by the region where the blue line falls below the green line in the left-hand tail of the two return distributions. This is due to the explicit use of a risk overlay program that is designed to manage absolute risk rather than relative risk to a benchmark. Against this, there is the opportunity cost of a lower chance of achieving a high return in the case where markets rally strongly, as the blue line falls below the green line in the right-hand tail of the two return distributions.

Impact of the Investment Mandate: Who Owns What?

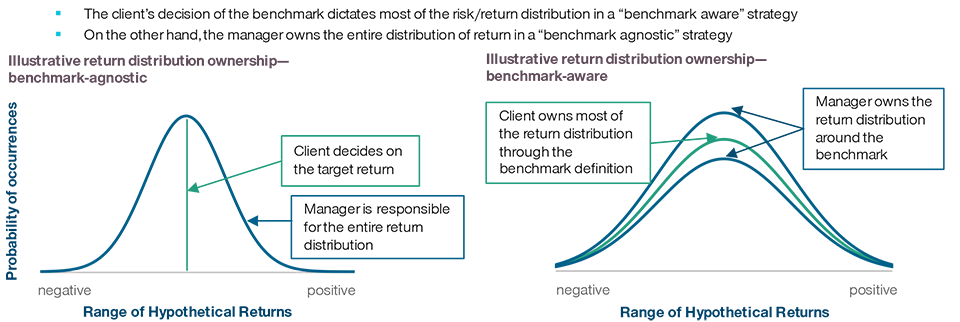

In Figure 3, we consider the impact on the “ownership” of the decision-making, again with the help of an illustrative distribution of hypothetical portfolio returns. Under a benchmark-aware mandate, the client chooses his or her benchmark composite and sets the target for relative return and risk levels. The choice for the benchmark effectively dictates much of the risk/return distribution in a benchmark-aware strategy, which is more closely tied to market direction, or beta. The portfolio manager, whose aim is to beat the benchmark over time via active management, can be regarded as “owning” the return distribution in a region or band around the return of the benchmark. It is clear that in a benchmark-aware approach, the client owns the majority of the decision of how the portfolio will evolve over time.

Objective of the Mandate—Who Owns What?

(Fig. 3) Illustrative benchmark-agnostic and benchmark-aware return distributions

Source: T. Rowe Price. This analysis is hypothetical and for illustrative and informational purposes only. The illustration is not based on actual portfolios nor does the illustration represent actual returns. Actual outcomes and returns may differ materially from the illustrations provided.

On the other hand, in the benchmark-agnostic case, once the client and portfolio manager have agreed on an appropriate cash + x% return, the manager ‘owns’ or is responsible for the entire return distribution. The portfolio manager in this case is granted greater discretion and flexibility, requiring a strong skill set that aims to generate a return as close as possible to the objectives over the specified time horizon.

A Questionnaire to Guide the Client’s Choice of Approaches

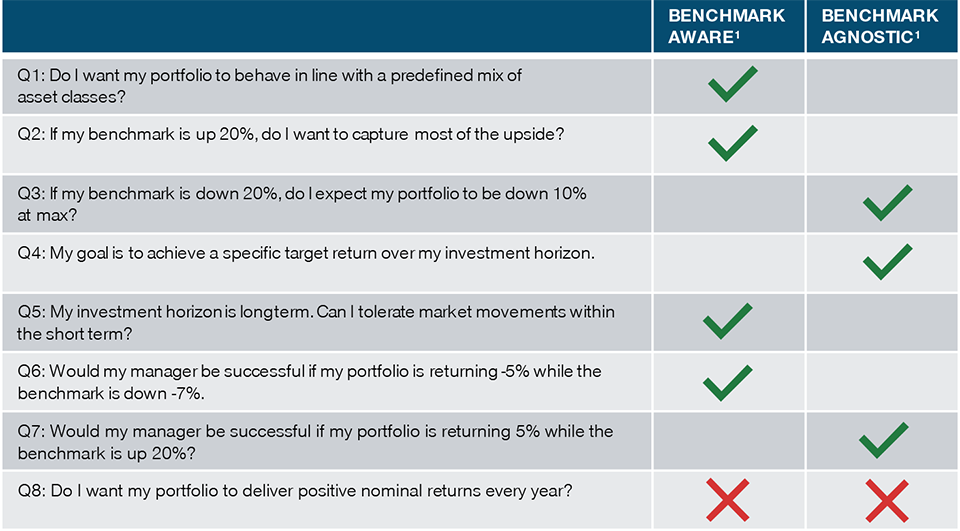

Having examined the key differences between a benchmark-aware and a benchmark-agnostic global multi-asset mandate, we have constructed a short questionnaire to help guide a potential client in making this important initial choice (Figure 4). This step can help to reduce the scope for disappointment by the client on subsequent portfolio performance that results in disagreements with the manager over the way the portfolio is being managed and who is responsible for what.

A Questionnaire to Guide the Client’s Choice of Mandate

(Fig. 4) Client portfolio key features

1 A green check indicates a positive answer to the question and a red cross a negative answer.

Source: T. Rowe Price. For illustrative purposes only.

Prospective clients should think long and hard before answering each question honestly. While the hypothetical examples in our questions of performance divergences between benchmark-aware and benchmark-agnostic portfolios may seem wide, in practice, gaps this big can easily arise. The biggest potential conflicts in the mind of the client are likely to arise between Q2 (“If my benchmark is up 20%, do I want to capture most of the upside?”) and Q3 (“If my benchmark is down 20%, do I expect my portfolio to be down 10% at max.?”).

In practice, it may be hard for the benchmark-agnostic investor to be satisfied with a return that is in line with or even modestly above their target when markets hit a purple patch and are rallying hard. So in the case of Q7—“Would my manager be successful if my portfolio is returning 5% while the benchmark is up 20%?”—it would be only human nature to be less than fully satisfied in this particular case, but this is what a benchmark-agnostic investor should expect. Equally, the benchmark-aware investor may find that in a deep market correction their capacity to sustain a drawdown is less than they had assumed.

But in view of such behavioral biases, we believe that a careful consideration by the client followed by a full and frank discussion with the portfolio manager of the differences between a benchmark-aware and a benchmark-agnostic mandate is essential in laying the groundwork for a healthy long-term client/manager relationship.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution retail investors in any jurisdiction.

November 2021 / INVESTMENT INSIGHTS