September 2021 / MARKETS & ECONOMY

UK Turns to Bold Post-Brexit Reforms to Boost Economy

Freedom to set finance and immigration policies may spur growth

More than five years since the people of the UK voted in a referendum to leave the European Union (EU), some features of the post‑Brexit landscape are starting to take shape. From the increasing likelihood of no deal on financial services to the UK’s new points‑based immigration system, key questions about what post‑Brexit life will look like are being answered. And while further questions remain, there are early indications that the UK’s newly acquired freedom to set its own policies in key areas may ultimately more than compensate for any reduction in trade with the EU.

In the 11th of a series of updates, Quentin Fitzsimmons and Tomasz Wieladek, T. Rowe Price’s resident Brexit experts, provide an overview of how life after the EU is going in the UK.

What Has Happened Since Our Last Update?

On Christmas Eve last year, the UK and the EU agreed to a Trade and Cooperation Agreement (TCA) covering their post‑Brexit trading and security relationship. The agreement meant that a widely feared no‑deal Brexit was avoided, but the outcome nonetheless resembled what would have been called a “hard Brexit” at the time of the referendum.

The TCA set a deadline of the end of March to agree a Memorandum of Understanding (MoU) on financial services—and on March 26 the UK and EU duly concluded technical discussions on the content of the MoU. It was hoped (though perhaps not expected) that the MoU would pave the way for the UK financial services industry to be granted “equivalence” from Brussels to provide the same services in the EU as it did before Brexit. As yet, no such equivalence has been granted.

The UK’s new points‑based immigration regime for EU citizens came into effect on January 1. Since then, EU citizens not already living in the UK have been treated the same way as those from the rest of the world. The only exception to the new system is Irish citizens, who are permitted to live and work in the UK as part of the Common Travel Area.

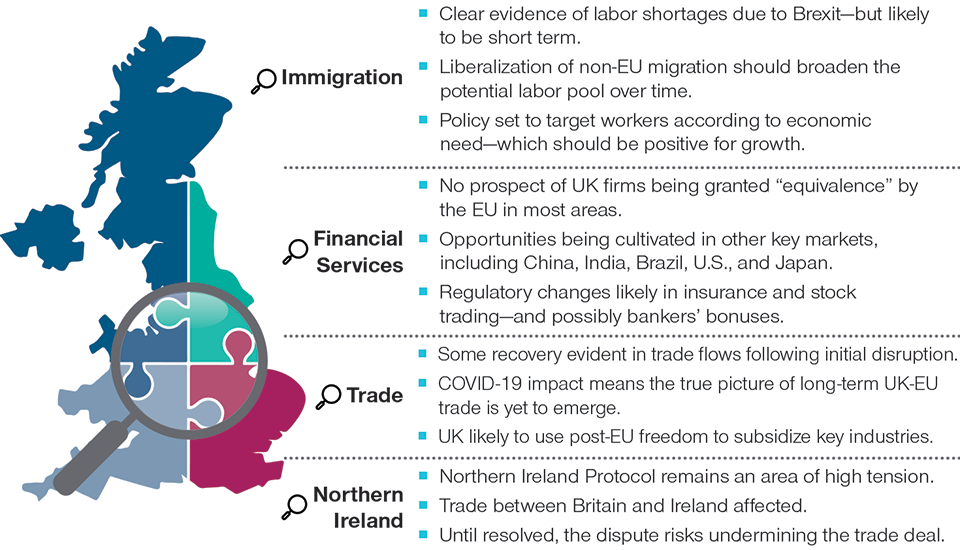

Post‑Brexit Policy Puzzle Takes Shape

Uneven progress in four key areas

Finally, the UK continues to seek urgent changes to the Brexit agreement known as the Northern Ireland Protocol, which is designed to prevent a hard border between Northern Ireland (in the UK) and the Republic of Ireland (in the EU). Since coming into force on January 1, the protocol has been the subject of heated disagreements between the UK and EU, most notably a dispute over transporting sausages and other chilled meats.

Where Are We Now?

Below, we share our views on how post‑Brexit life is shaping up for the UK in four key policy areas: financial services, immigration, trade, and Northern Ireland. Let’s take each of these in turn.

Financial Services

In a speech to business leaders in July, UK finance minister Rishi Sunak appeared to signal that his government is no longer assuming that equivalence‑based access to EU markets will be granted to UK financial services firms. If he is right, many London‑based businesses will have to accept that their ability to provide financial services in the EU will be significantly restricted for the foreseeable future. The question is whether the UK can reform its legal and regulatory framework in a way that retains the city of London’s competitive advantage.

Here, the UK faces a dilemma: Does it seek to remain close to EU law in the hope that equivalence may be granted at some point in the future, or does it introduce more ambitious reforms to attract business from the rest of the world? We believe it will choose the latter. There is now a major opportunity for the UK to form close ties with emerging financial centers such as China, India, and Brazil, as well as to deepen its existing relationship with traditional markets such as the U.S., Singapore, and Japan. Indeed, as the finance industry is highly dependent on human capital, the decision to allow all non‑UK students to look for employment for up to two years after their degree (as opposed to three months previously) supports this strategy. In the long term, the potential business to be won from these countries could help offset any loss of business from the EU.

What reforms might we see? Britain’s finance ministry has already set out a number of reforms it would like to make in capital markets. One is to amend insurance capital rules known as Solvency II to cut the burden on how insurers calculate their core solvency capital requirement. Another proposed reform is to scrap certain stocks and derivatives trading rules under the EU’s MiFID II framework to remove barriers to entry and encourage more smaller firms to list. Finally, there are discussions to scrap the EU’s cap on banker’s bonuses. Although politically unpopular, such a change would enable banks to make a higher proportion of their employees’ salaries variable, which would allow them to cut costs more quickly during a crisis and, therefore, contribute to greater banking sector stability.

Overall, we believe that Brexit could result in short‑term disruption but long‑term gain for the UK’s financial services sector.

Immigration

The UK’s post‑Brexit immigration system is likely to follow a similar pattern of initial disruption giving way to eventual gain. The disruption is already being felt as many UK industries, most notably the hospitality sector, have begun to encounter severe worker shortages since reopening after the coronavirus lockdown. The evidence suggests that there was a large exodus of EU‑origin workers from the UK during the pandemic and few have returned because of quarantine restrictions. It is uncertain how many of these vacancies will remain unfilled since it is unclear how many of 5 million people who have been granted settled status will eventually return.

Nevertheless, we believe the current labor shortages are likely to be temporary. Training in the professions reporting severe shortages, such as heavy goods vehicle drivers, ceased during COVID-19 lockdowns, creating a training backlog. At the same time, the furlough scheme kept many employees attached to industries that may not need as many workers in the future. These workers will eventually transition to those sectors that are currently experiencing shortages, although this will take time. Furthermore, the UK’s new immigration regime has made it far easier for immigrants from outside the EU to come and work in the UK. All of these reasons suggest that the current labor shortage in some UK sectors is more likely to be temporary than permanent.

In the longer term, the UK’s new immigration system may prove to be beneficial for growth. While it represents a significant tightening of controls on EU migration compared with freedom of movement, it also brings a considerable liberalization of non‑EU migration, with lower salary and skill levels, and no overall cap on numbers. A key labor market test in the UK’s pre‑Brexit immigration system required employers to demonstrate that workers who were already settled in the UK had the opportunity to apply for the position before it could be offered to a prospective immigrant worker. This requirement has now been dropped, meaning that a position can be directly offered to a migrant worker. Finally, the time that students at UK universities from outside the EU can search for a job in the UK has been extended from three months to two years. Overall, the UK’s new immigration system is considerably less restrictive for immigrants from outside the EU.

Economic migrants typically leave their home country in search of opportunities elsewhere. When the Eastern European economies entered the EU, the UK’s gross domestic product (GDP) per capita (a measure of income per person) was roughly double of these economies. The UK’s GDP per capita today is seven times that of India, whose citizens will benefit from the lower restrictions to come and work in the UK. This large difference in potential income between the UK and many large developing countries, together with the new less restrictive immigration system, will make the UK a magnet for many migrants from outside the EU.

Of course, these rules are still new, and only time will tell if they work as predicted. If, however, the UK government indeed uses the new system to attract workers in areas where they are most needed and can add the most value, the country’s post‑Brexit immigration policy may boost—rather than limit—long‑term growth.

Trade

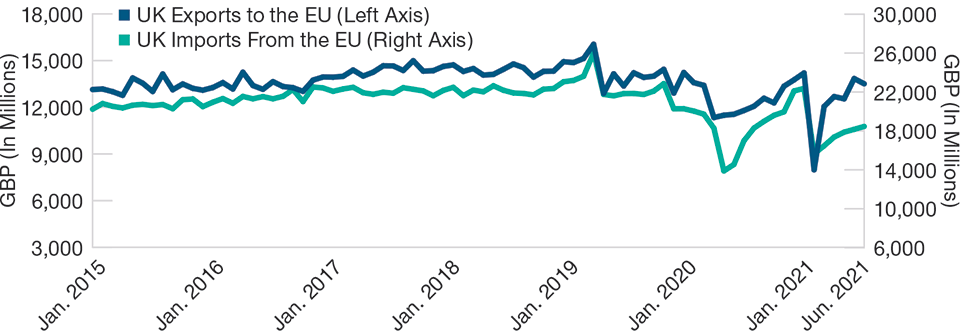

Trade between the UK and EU dropped by almost a quarter in the first three months after the UK left the bloc’s single market and customs union on January 1. However, it has shown signs of recovery since then. Official figures show that UK exports to the EU increased by 9.1% to GBP 14.1 billion in May, when exports first exceeded pre‑Brexit levels. In June, exports of goods to the EU rose by another 1.2% to GBP 14.3 billion.

Trade going the other way has bounced back, too. The EU statistics office Eurostat has reported that EU exports to the UK rose by 4.7% in June, while the bloc’s exports to the rest of the world dropped slightly the same month. Seasonally adjusted EU exports to Britain remained below the last months of 2020 but were higher than June 2020, when coronavirus restrictions were tighter.

On the surface, these figures seem to imply that post‑Brexit trade between the UK and EU has already recovered strongly from its early‑year dip. Caution is advised, though. It is possible that trade was so heavily suppressed by the coronavirus that the recent sharp increase in volumes is more indicative of a post‑COVID-19 recovery than a post‑Brexit one. There is anecdotal evidence that many UK companies, particularly small firms, continue to struggle with the additional red tape that exporting to the EU now involves. It remains unclear whether widespread reports of empty supermarket shelves are due to lack of EU lorry drivers or self‑isolation requests due to close contacts with a person who tested positive for COVID‑19. As such, the true picture of the long‑term post‑Brexit trading relationship between the UK and EU is probably yet to emerge.

UK–EU Trade Appears to Have Recovered

(Fig. 1) The picture may be distorted by COVID-19, however.

As of June 30, 2021.

Source: Office for National Statistics.

It is also worth highlighting the fact that the UK government seems to have shifted its approach to industrial policy since leaving the EU. In June, the government announced plans for a more “nimble” post‑Brexit system of state subsidies to boost or protect selected industries. It said that the new system would “start from the basis that subsidies are permitted if they follow UK‑wide principles—delivering good value for the British taxpayer while being awarded in a timely and effective way.” Indeed, this approach has already borne some fruit: Former PM Theresa May’s Life Science Industrial strategy change in 2017 resulted in the creation of the UK’s first Vaccines Manufacturing and Innovation Centre. When completed in 2022, this pre‑pandemic investment will support the fight against the pandemic through enhanced vaccine research and production capabilities.

During negotiations on the trade deal, the EU had pushed for Britain’s state‑aid rules to remain aligned with the bloc to ensure a “level playing field,” but Prime Minister Boris Johnson resisted this. The new regime will likely enable the UK government to support chosen industries more easily than when it was in the EU, but it will not amount to a subsidy free‑for‑all—a subsidy advice unit will be established within the UK’s Competitions and Markets Authority to advise on whether subsidies are fair, and companies that feel they have been unfairly disadvantaged will be able to challenge decisions in the courts.

Even allowing for these checks and balances, however, the UK’s switch to its own system of state subsidies should allow it to allocate resources more efficiently and provide vital support for industries that are driving key social developments, such as green technology. The success of this strategy depends on making the right investments. However, UK authorities already demonstrated their ability in this area by investing in a Vaccines Manufacturing and Innovation Centre in 2017. While not all investments will work out, foresightful industrial policy can lead to important economic benefits.

Northern Ireland

At the time of writing, it remains to be seen how the tensions between the UK and EU over post‑Brexit trading arrangements in Northern Ireland will be resolved. Despite signing up to Northern Ireland Protocol, the UK has accused the EU of applying it too rigidly and is seeking to get rid of most of the checks to allow goods to flow more freely. The protocol keeps Northern Ireland aligned with the EU’s single market for goods to ensure free trade across the Irish border. However, it has also resulted in additional checks on goods moving between Northern Ireland and the rest of the UK—a development that has been vehemently opposed by Northern Ireland’s Democratic Unionist Party, one of the two biggest parties in the Northern Ireland Assembly.

Freight flows between Britain and Ireland have fallen by almost a third since the beginning of the year as Irish businesses have opted to send goods directly into Europe rather than through the UK to avoid potential delays as goods travel from Britain into the EU. The EU has insisted it will not renegotiate the protocol but says it will consider any proposals that “respect the principles” of the deal.

As yet, no resolution to the dispute over Northern Ireland is in sight. Given the stakes involved, it seems likely that one will be found eventually, but until that happens the possibility that disagreements over Northern Ireland unravel other parts of the TCA cannot be completely dismissed.

Early Days—But Growing Optimism

Brexit remains an ongoing process rather than an accomplished fact. Eventually, the smoke will clear and we will get a better view of what the post‑EU British economy will look like. Until then, the debate about the costs and benefits of Brexit will continue.

In the meantime, the most sensible course—in our view—is to monitor developments closely and adjust our analysis as more information becomes available. On that basis, we note with interest that it appears that the UK is going to use its new immigration system to attract highly skilled foreign workers to areas where they are most needed and enact key regulatory changes to boost the competitiveness of its key financial services sector. Both developments should be economically beneficial over the long term, as should the UK government’s switch to a new system for directing state subsidies.

Although there are signs that the trade in goods has begun to recover, it may take a while longer for the true picture of the post‑Brexit EU-UK trading relationship to emerge. Until it is resolved, the dispute over the Northern Ireland Protocol has the potential (however unlikely) of causing the gains made so far to be lost. The next few months should provide further clarity on these issues.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution retail investors in any jurisdiction.

September 2021 / INVESTMENT INSIGHTS