July 2021 / INVESTMENT INSIGHTS

How Weighing ESG Risks Adds an Edge in EM Corporates

Integrating ESG factors has the potential to provide a research edge

Key Insights

- Integrating ESG factors has long been part of our approach to risk management and potential alpha (excess return) generation within emerging market (EM) corporate bonds.

- The ESG profiles of companies within the EM corporate bond universe can vary markedly, making ESG integration essential to investment decision‑making.

- Three key ESG dynamics are at play within the EM corporate bond universe: growing investor focus, greater regulation, and an increasing market impact.

Integrating environmental, social, and governance (ESG) factors within our investment process is a long‑standing part of our approach to risk management and potential alpha (excess return) generation. Credit analysts research company fundamentals to identify those that we believe are inefficient or have the potential for ratings upgrades—this includes the consideration of ESG factors alongside traditional financial analysis.

We screen the portfolio using T. Rowe Price’s proprietary Responsible Investing Indicator Model (RIIM). RIIM analysis and the research of our in‑house responsible investing and governance teams provide broad coverage of the ESG risks and opportunities among companies in our universe. It offers a second perspective on the ESG characteristics and any elevated exposures in the portfolio.

Last, we utilize sovereign research and analysis to inform macro and sovereign views that underpin our corporate positioning. An emerging market country with better sovereign ESG characteristics—and a more robust regulatory environment—will typically provide a better backdrop for corporate investing and potentially encourage better corporate ESG practices. RIIM is invaluable here—it evaluates sovereign issuers on ESG criteria. Our sovereign analysts provide added insights on transparency, geopolitical assessments, and social stability factors.

The Integration of ESG Factors Is Essential

Integrating ESG factors is essential to our alpha generation and risk management goals. The ESG profiles of companies within the emerging markets corporate bond universe can vary markedly—there are questionable companies, and there are good ones. Some sectors are more prone to having riskier ESG characteristics, such as extraction industries, while others are leveraged to more sustainable business trends and have shown good progress on certain ESG factors, such as Chinese real estate companies.

Three key ESG risk categories that demand particular attention in the emerging market corporate bond universe are:

1. Social and Political Risk: The policy direction of a country—institutional quality, free speech, rule of law, and wealth equality—can have a profoundly positive or negative impact on its population and businesses. Conversely, improvements in areas like property rights and education can create sustained opportunities in the private sector. Our sovereign analysis is vital to building an in‑depth understanding of the social and political profiles of each country in which we invest.

2. Environmental Risk: In areas such as energy, utilities, and mining, which comprise a relatively large share of the emerging markets universe, a company’s environmental practices can have significant effects on its business. On the positive side, companies that improve their practices are likely to enjoy lower capital costs and regulatory support.

3. Corporate Governance Risk: For emerging markets, this is particularly important. Given the risks inherent in emerging markets lending, we require a high degree of comfort with the history, reputation, and other business relationships of the management teams we support.

ESG Trends to Watch Within Emerging Market Corporate Bonds

There are three dynamics at play here—client demand, regulatory pressures, and markets. Clients around the globe are increasingly concerned with how ESG factors play a part in their investment portfolios. It’s rare for our institutional client meetings not to feature discussions on ESG.

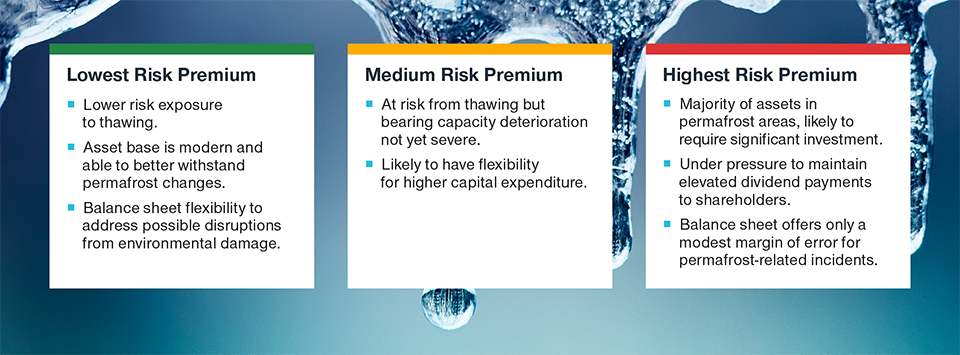

Assessing Company Vulnerability to Permafrost Thawing

Incorporating a risk premium1 for thawing into our bond evaluation

1 The additional return expected from an investment to compensate for the level of risk being taken. This is an illustrative example of how ESG factors may be incorporated into the investment process by portfolio managers. The views expressed may differ from those of other investment professionals at T. Rowe Price.

Regulation is also changing rapidly, driving changes in the way companies conduct their business and the extent and quality of their ESG disclosure. Particularly when it comes to environmental regulation, the landscape will be very different going forward. For decades, companies have borne little to no cost for the externalities of pollution or use of natural capital. Markets are increasingly pricing ESG factors into credit risk and spreads (the additional yield that investors require for holding riskier assets). For example, a Brazilian pulp and paper company we recently researched issued a sustainability‑linked bond at a lower cost than traditional debt.

ESG Factors as a Direct Influence on Investment Decisions

A recent example is our analysis of the impact of climate change on a Russian mining company. The company has infrastructure built on permafrost (ground that remains frozen at zero degrees or below for at least two years consecutively) in northern Russia. As the permafrost layer has begun to thaw and subside due to the warming of the climate, the company’s logistics infrastructure has suffered collapses, including a rail line and a storage tank. These issues will be costly to remedy and will require ongoing investment. As a result, we reassessed the appropriate spread.

Another example is a Chilean utility issuer. The company’s shift to renewables should lower the group’s average carbon intensity. The company is also transitioning its coal assets from providing baseload power generation to providing crucial grid balancing services, which has the potential to facilitate deployment of renewables in the electricity system. These adaptations have potential benefits in a world where momentum is building for a transition to cleaner energy.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution retail investors in any jurisdiction.

July 2021 / MARKETS & ECONOMY