June 2022 / MARKET OUTLOOK

Fundamentals Matter

With earnings growth likely to decelerate and interest rates rising, what opportunities do equity markets offer?

A brutal spike in bond yields largely drove global equity losses in the first half of the year. In the second half, stock market performance is likely to depend on the outlook for corporate earnings growth.

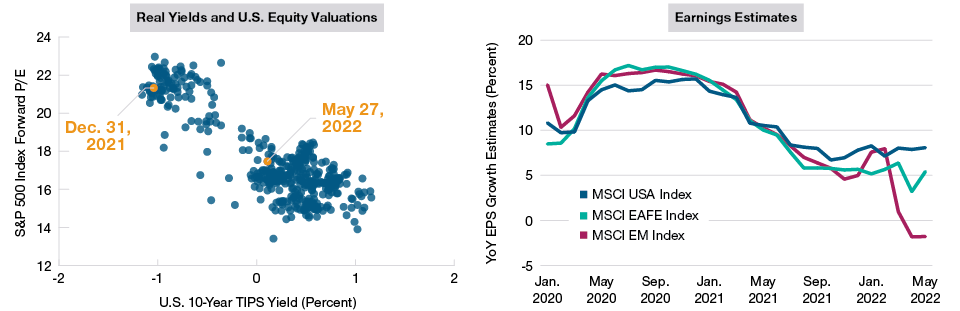

After spending most of 2021 in deep negative territory, Page notes, the real, or after‑inflation, 10‑year Treasury yield (as measured by the 10‑year TIPS yield) turned positive at the end of April. Figure 3 (left panel) shows the effect this had on U.S. equity valuations, which fell closer toward the middle of their recent historical range.

The Balance of Equity Risks Is Shifting From Interest Rates to Earnings Growth

(Fig. 3) S&P 500 Index forward P/E vs. 10‑year Treasury real yield and 2022 EPS growth estimates in USD

P/E versus real yields from January 3, 2014, through May 27, 2022. EPS estimates from January 31, 2020, through May 31, 2022.

Sources: Haver Analytics/U.S. Bureau of Economic Analysis, Federal Reserve Bank of Dallas, MSCI, and T. Rowe Price calculations using data from FactSet

Research Systems Inc. All rights reserved (see Additional Disclosures).

Now, Page says, with growth concerns rising, the focus is shifting to the “E” side of the price/earnings (P/E) ratio. “Everybody’s wondering if this will be the next shoe to drop.”

Although earnings momentum sagged in many non‑U.S. markets in the first half, earnings per share (EPS) growth in the U.S. remained surprisingly steady (Figure 3, right panel). But Page says he doesn’t believe this strength will last. “I think U.S. earnings are likely to decelerate in the second half, challenged by slowing economic growth,” he predicts.

Supply chain improvements also could impact earnings—but maybe not in a good way, Page says. While moving more products might boost sales and revenues, it also could limit pricing power and eat into profit margins.

Sector and Style Leadership

Poor earnings environments historically have tended to favor the growth style, which typically is less threatened by cyclical downturns. But, Thomson says, this time could be different, given the heavy weight the technology sector now carries in the growth universe.

“The pandemic really did pull forward digitization, so we’re going to be lapping some very strong 2021 earnings comparisons in the second half,” Thomson explains. “We’re also seeing some late‑cycle effects that are detrimental to tech, such as skill shortages and salary inflation.”

Consumer‑oriented technology platforms, such as streaming media, also could be exposed to a cyclical slowdown in spending, he adds.

These factors suggest that the back‑and‑forth style rotations seen since the pandemic recovery have tipped in favor of value. “A shift in market leadership appears to be underway,” Thomson says. “As we’ve seen from history, these cycles have tended to last a long time.”

China Could Offer Opportunities

With the Morgan Stanley Capital International (MSCI) China Index down almost 50% from its early 2021 peak as of the end of May, Chinese equity valuations appeared potentially attractive, Thomson suggests. However, Beijing’s “zero COVID” strategy has been a key obstacle to a growth revival.

“China has the capacity to stimulate,” Thomson observes. “But there’s no point in stimulating while locking down. It’s like stepping on the accelerator and the brake at the same time.”

How effectively Chinese policymakers will be able to boost growth in the second half is not yet clear, Thomson says. In addition to the coronavirus, sagging property values and credit defaults also could challenge any stimulus efforts.

That said, Thomson adds, in a world where many central banks are withdrawing liquidity to fight inflation, and governments in many developed countries are running deep fiscal deficits, China at least has scope to focus policy on supporting growth.

Another key factor for Chinese equities in the second half could be the regulatory climate, Thomson says, including Beijing’s treatment of the country’s domestic technology platform companies and its crackdown on foreign depositary receipt listings.

Thomson says he believes regulatory policies are likely to turn more market friendly in the runup to the Chinese Communist Party’s 20th Party Congress later in the year. “This regulatory cycle has been particularly drawn out and deep,” he says. “But we believe these issues will get better from here.”

Thomson says he’s reluctant to predict a leadership shift to non‑U.S. equities in the second half, given the U.S. market’s extended outperformance over the past decade. However, if the U.S. dollar appreciation seen in the first half subsides, and the technology sector continues to struggle, the relative performance of non‑U.S. equity markets should at least improve, he says.

Download the full 2022 Midyear Market Outlook insights

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

Justin Thomson is the head of International Equity. Justin is a member of the Management Committee and the chairman of the International Equity Steering Committee. He is a member of the Asset Allocation and ESG Committees. He also is the chief investment officer for International Equities. He is a vice president of T. Rowe Price Group, Inc., and T. Rowe Price International Ltd.

Arif Husain is the head of Global Fixed Income and chief investment officer of the Fixed Income Division. He is chairman of the Fixed Income Steering Committee and a member of the firm’s Management Committee. Arif is lead portfolio manager for the Global Government Bond High Quality Strategy. He is a vice president of T. Rowe Price Group, Inc., and T. Rowe Price International Ltd.