October 2022 / INVESTMENT INSIGHTS

The Case for a Strategic Allocation to High Yield Bonds

Hybrid characteristics provide attractive risk/reward profile

Key Insights

- High yield bonds, in our view, have a key role as a strategic long-term investment and a mainstay allocation in a well-diversified portfolio.

- High yield bonds have an attractive risk/reward profile, having historically provided equity-like returns with less volatility than stocks.

- Investors have been able to recognize much of high yield’s value by maintaining a long-term allocation and taking advantage of the regular coupon payments.

High yield (HY) bonds, in our view, have a key role as a strategic long‑term investment and a mainstay allocation in a well‑diversified portfolio. Historically, high yield bonds have provided equity‑like returns with less volatility. Investors have been able to recognize much of high yield’s value over time by maintaining a long‑term allocation and taking advantage of the potential compounding effect of regular coupon payments.

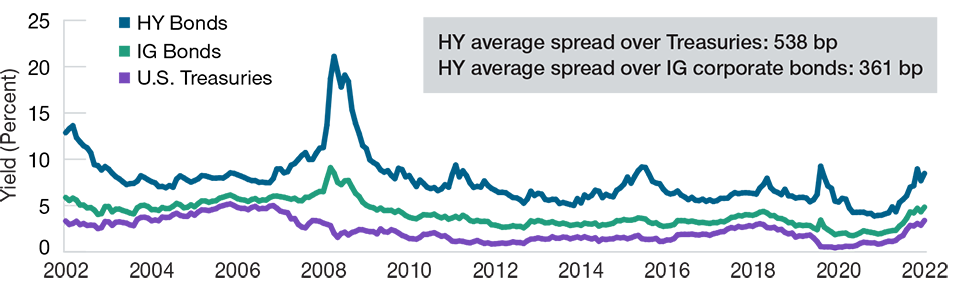

Yields and Spreads Over Time

(Fig. 1) Wider spreads to Treasuries indicate greater risk

From August 30, 2002, to August 31, 2022.

Past performance is not a reliable indicator of future performance.

Source: T. Rowe Price calculations using data from FactSet Research Systems Inc. All rights reserved.

High yield bonds are represented by ICE BofA U.S. High Yield Constrained Index; investment‑grade corporate bonds by Bloomberg U.S.

Corporate Investment‑Grade Index; and U.S. Treasuries by ICE BofA U.S. Treasury Index. A basis point is 0.01 percentage point.

Yield is based on yield to worst, which is the lowest potential yield that can be realized on a bond without the issuer defaulting.

The High Yield Risk/Reward Dynamic

High yield bonds are typically issued by companies that are rated below investment grade by one or more of the three main credit rating agencies. Due to their lower credit ratings, investors typically receive higher yields on below investment‑grade bonds in exchange for greater risk of default. This risk/reward dynamic is also expressed through credit spreads on high yield bonds, or their incremental yields over similar‑maturity U.S. Treasuries, which are perceived to carry near‑zero default risk. Typically, wider spreads indicate greater perceived risk.

Hybrid Asset Class

High yield bonds are often considered to be a hybrid asset class because they tend to exhibit characteristics of both fixed income and equities. Like most other fixed income securities, high yield bonds offer a steady stream of income in the form of coupon payments, which averaged 7.40% over the 20 years ended August 31, 2022.1

However, high yield bonds tend to be more equity‑like in how they behave, given that credit (default) risk is the primary risk associated with investing in the asset class. Thus, unlike most other traditional fixed income instruments whose performance is closely tied to changes in interest rates, high yield bonds’ performance tends to be much more strongly linked to the business results and fundamentals of the companies that issue them.

Positioning in a Diversified Portfolio

Given their hybrid nature, high yield bonds have a unique and attractive risk/reward profile, having historically provided equity‑like returns with less volatility than stocks. Therefore, they can be thought of as either part of an overall fixed income allocation or a potential equity replacement. For fixed income investors, high yield bonds provide the potential for higher yields and greater returns, while also adding important diversification from traditional fixed income investments.2 For equity investors, particularly those that may be more risk averse, high yield bonds can offer similar returns with lower volatility and potential downside than stocks.

Income as a Key Source of Return

Most high yield bond portfolio managers focus on opportunities for both income and price appreciation as they invest. However, an analysis of historical sources of return shows that, unlike stocks, high yield bonds have typically derived the majority of their long‑term total returns from income rather than capital appreciation.

Their relatively high and generally consistent coupon payments are a key reason why high yield bonds have historically exhibited lower volatility than stocks. Because their long‑term returns have tended to be so heavily income driven, it pays to think of high yield bonds as a long‑term strategic investment because the compounding effect of these regular coupon payments can be meaningful over time.

Download the full article here

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

October 2022 / INVESTMENT INSIGHTS

October 2022 / INVESTMENT INSIGHTS