May 2021 / INVESTMENT INSIGHTS

Prospects Brighten for Global Dividend Stocks

Post-pandemic recovery will likely aid company earnings and dividends

Key Insights

- The pandemic‑induced slowdown of 2020 compelled many companies to lower dividends, weighing on dividend investing styles.

- Signs of a global economic recovery augur well for dividend‑paying companies, as company earnings improve.

- We see opportunities in banks; utilities with exposure to solar and wind energy; and property and casualty insurance, which can potentially benefit from the recovery in economic activity.

Equity dividend or income strategies had a particularly difficult time in 2020, thanks to the deep, if short‑lived, global recession triggered by the coronavirus pandemic. However, as economies begin to recover, growth should feed through to company earnings and provide a foundation for companies to reinstate dividend payout ratios.

The Pandemic Weighed on Dividend Investing Styles in 2020

As a rule, listed companies are very reluctant to cut dividends other than in exceptional circumstances when they have few other choices. The reluctance of companies to lower dividends is largely because they fear a cut will be seen by shareholders and investors as a negative signal of management’s confidence in the future prospects of the firm.

The unprecedented speed and depth of the collapse in global demand due to the national lockdowns and social distancing policies introduced to counter the coronavirus meant that many companies had little choice but to slash their dividends last year. In 2020, around 30% of the MSCI World Index’s constituent stocks announced that they would cut dividends, the highest share of dividend reductions since the global financial crisis.

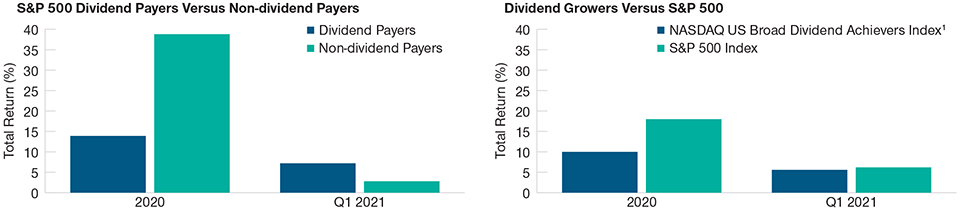

Dividend Payers and Growers Significantly Underperformed in 2020

(Fig. 1) Total returns in 2020 and Q1 2021

As of March 31, 2021.

1 Composed of U.S. securities with at least 10 consecutive years of increasing annual regular dividend payments. Is the secondary benchmark for our US Dividend Growth Equity Strategy.

Sources: T. Rowe Price analysis using data from FactSet Research Systems Inc. All rights reserved. S&P indices (see Additional Disclosure).

Given these widespread cuts, it is not surprising that dividend investing styles fell out of favor. The chart on the left in Figure 1 compares the performance of S&P 500 dividend payers with that of S&P 500 non‑dividend‑paying companies in 2020 and in the first quarter of 2021. The right‑hand chart makes the same comparison for dividend growth stocks (proxied by the NASDAQ US Broad Dividend Achievers Index). Due to the unique circumstances created by the coronavirus pandemic, 2020 was the worst year for dividend payers versus dividend nonpayers and for dividend growth stocks since 2009 and the global financial crisis.

Driven by the market rotation into value, dividend payers in the first quarter of 2021 outperformed, clawing back some of the ground lost last year. In contrast, dividend growth stocks underperformed slightly in Q1 as they were not favored by the switch to value.

In 2020, three growth sectors—information technology, consumer discretionary, and communication services—accounted for 87% of the gain in the S&P 500. In the first quarter of this year, the same three sectors contributed just 26% to the gain in the S&P 500. Financials and energy, in contrast, two of the biggest drags on S&P 500 returns in 2020, have contributed over 50% to the index’s gain in 2021.

Sustained Global Recovery a More Positive Backdrop

Overall, we think the investment environment should become a lot more favorable for global dividend/equity income strategies. With the global composite Purchasing Managers’ Index for manufacturing and services standing at a six‑and‑a‑half‑year high in March, it is clear that a powerful cyclical recovery is likely underway in the global economy. The International Monetary Fund in its April World Economic Outlook, for example, forecasts the global economy to grow by 6.0% this year, a dramatic turnround from last year’s 3.3% decline. The rapid rollout of vaccines against COVID‑19 in some countries has played a large part in the recovery of business, consumer, and investor sentiment. It is proving successful in rapidly reducing the number of new infections, promising an end to lockdowns and social distancing in countries that have been able to acquire sufficient supplies of the new vaccines. As a result, many economists expect a strong recovery in consumer services this year, which, until recently, was a lagging sector.

The unprecedented U.S. fiscal stimulus since 2020 has also been big enough to have significant spillover effects, boosting other economies. President Joe Biden’s USD 2 trillion infrastructure plan also plays an important role in the global recovery scenario. It greatly reduces the risk of a “fiscal cliff” developing in the U.S. next year as the impact of the front‑loaded USD 1.9 trillion American Rescue Plan Act begins to fade.

A Strong Earnings Rebound Can Help to Repair Dividends

A strong cyclical economic recovery in 2021 and 2022 should feed through to company earnings. Many of the companies that were forced to cut their dividends during the pandemic are likely to reinstate dividend payout ratios as economic conditions improve. Others, such as banks in a number of countries including the UK and in Europe, were obliged by government pandemic emergency support measures to cut or refrain from paying dividends even though their fundamentals had not deteriorated that much and they still had the ability to pay. There will also be companies in other sectors that in the pandemic cut dividends excessively, fearing a worst‑case scenario that did not materialize.

There are many companies with strong balance sheets and management in areas like consumer discretionary, transportation, infrastructure, and entertainment that, although hit by the pandemic, are showing an ability to stage strong recoveries. Some of these companies may only be yielding 1.0% today but have the potential to raise their dividend yield (DY) to 3% or 4% over the next two to three years. The companies to avoid are the dividend cutters that already had issues and fragilities before the pandemic struck.

Threat From Higher Bond Yields May Be Less Than Consensus Imagines

Since global long‑term rates may rise further, probably in steps, it is important to understand how to manage a dividend equity strategy over rate steepening and flattening cycles. Traditional high‑DY stocks or “bond substitutes” such as utilities, real estate investment trusts, infrastructure, or telecom companies are likely to prove vulnerable if U.S. Treasury yields rise faster than the market currently expects (which may not be such a high‑probability scenario based on the argument above). However, there are also cyclical growth dividend payers among bank, insurance, chemical, commodity, or property stocks that historically have shown they can outperform in upcycles even as bond yields rise.

The key to controlling the interest rate sensitivity of the portfolio is to maintain a good balance between these two types of dividend stocks over the interest rate cycle. As the economic cycle weakens and the yield curve flattens, one should have more stocks in the traditional high DY bucket. Conversely, one should have more cyclical growth dividend stocks during the economic recovery phase, when yield curves are steepening. Thus, we tend to follow a dynamic barbell approach in which our weighted average DY stays much the same, but where the portfolios’ interest rate beta or sensitivity varies over the cycle.

Dividend stocks can even be found in the technology sector among semiconductor manufacturers and semiconductor equipment companies. For example, a U.S.‑based manufacturer we own in this sector has achieved an annual growth of 12% from 2004 to 2020 and committed to return all free cash flow to shareholders via dividends and buybacks. The business is the beneficiary of the technology shifts toward digitalization, automation, and Internet of Things connectivity.

Historically, dividend‑cutting stocks have delivered lower total returns and higher volatility. In contrast, companies that pay a high or above‑average dividend combined with decent growth prospects can generate strong cash flow for investors, helping to act as a buffer or cushion to unexpected bouts of market volatility. The result of skillfully blending traditional high‑DY stocks and dividend growth stocks has the potential to provide an attractive overall portfolio risk/return trade‑off over the market cycle. We believe that after a difficult 2020, dividend payers and growers in the future can continue to provide strong downside protection and superior risk‑adjusted returns to investors over full market cycles.

Where We Are Looking for Dividend Opportunities

In terms of investment themes among dividend stocks in 2021, the fundamentals of some utility stocks have improved, driven by the secular shift to renewable forms of energy. We think that these companies are positioned to grow their earnings by 5% to 7% per annum and this, combined with their high dividend yield, could potentially see a total return to shareholders in the high single digits. One company we like is a leading generator of wind and solar energy in the U.S. Its management has committed to a 13% to 15% annual dividend growth through 2024.

We also believe there is further room for banks to run, as we think accelerating loan growth in 2021 is not fully priced in at current levels. Banks are also beneficiaries of the trend toward higher global interest rates. Elsewhere in financials, property and casualty insurance companies are poised to benefit from the rising residential property cycle as home price increases should flow through to margins and earnings. Durable, high‑quality growth at a reasonable price and yield stocks have generally lagged so far this year as investors favored other areas of the market. As a result, we think a number of these dividend growth names could offer attractive risk/reward profiles on a multiyear view.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution retail investors in any jurisdiction.