March 2021 / INVESTMENT INSIGHTS

China’s Economy: Recovery and Rebalancing

Emerging from the pandemic, an encouraging pathway for China’s economy

Key Insights

- China’s V‑shaped recovery from the coronavirus pandemic has been stark in comparison with many other economies.

- While this is encouraging, China’s long‑term strategy and track record are more important indicators as it strives to become a more developed economy.

- The rise of technology and innovation represents a meaningful shift in direction for China, a fact that is probably underappreciated by the market.

China and its strong economic recovery from the coronavirus pandemic have not gone unnoticed. Fourth‑quarter gross domestic product (GDP) growth came in at 6.5% year over year, pushing the annual average growth to 2.3% for 2020. China should be the only major economy to record economic growth for 2020. But what lies ahead for the second‑largest economy in the world, and what are the factors that we should watch for as it continues to progress?

Pandemic Response Has Allowed a Much Quicker Recovery

China’s V‑shaped recovery has been primarily attributed to a strong public health response. China successfully implemented what the IMF called “effective containment measures” to aggressively curb the spread of COVID-19, the disease caused by the coronavirus. The return to a more normal environment has been driven by three main factors—swift lockdowns, testing, and masks.

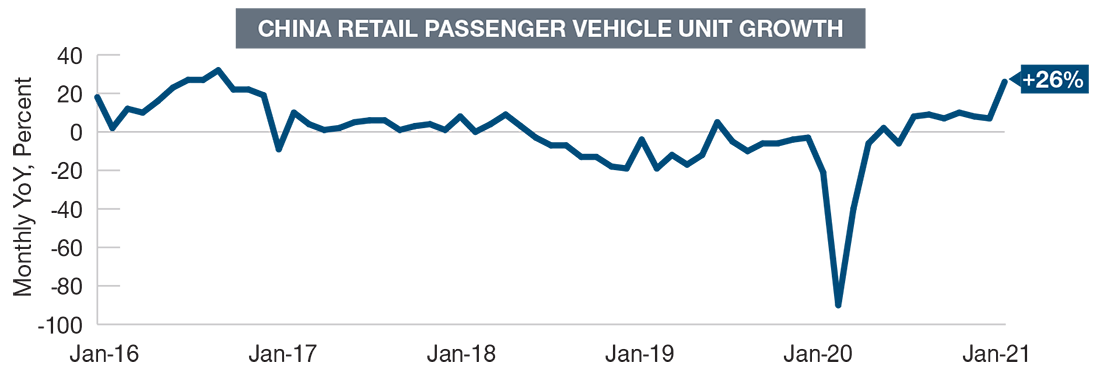

China adopted stringent measures very quickly to deal with the pandemic, with previous experience of pandemics (e.g., SARS) and the political structure allowing for quicker control of the disease. This has allowed the economy to get back on track much quicker, with manufacturing the first to bounce back and followed by a recovery in the services sector. Vehicle sales data provide one indicator of the nature of the V‑shaped recovery.

China’s Central Bank Is Playing the Long Game

The sharp recovery has not, however, been driven by major monetary or fiscal support. Unlike the unprecedented action taken by western central banks, China’s policy response to the pandemic has been more muted. This is primarily because its rapid recovery has enabled policy to taper relatively quickly.

China’s V-Shaped Recovery

Chinese vehicle sales indicate a strong rebound in consumer spending and sentiment

As of January 31, 2021.

Source: China Association of Automobile Manufacturers.

Compared with the stimulus measures undertaken in 2009 and 2016, Chinese policymakers have been a lot more guarded because of less balance sheet space but also because of not wishing to leave a legacy of higher debt. While credit to GDP jumped by over 20% in 2020, central bank policy for 2021 is focused on that not going higher.

The People’s Bank of China (PBoC) has initiated a number of policies, designed to prop up the economy in response to the coronavirus outbreak. But it has also been very careful at the same time not to increase the financial leverage in the system with the country’s growing debt burden. It has succeeded in stalling the pace of growth, but there is still more to do, and the PBoC is likely to tread carefully. What is important to remember is that the PBoC has many weapons in its arsenal to help manage and ensure the stability of the economy. China has a strong record of achieving its objectives, and investors should remain focused on this.

Strong Recovery Followed by Managed Slowdown

In the short term, we expect economic growth to bounce back to around 8% to 9%, but after that, we expect it to head back down to around previous levels of 6%, with the medium‑term growth rate being around 5%. Beyond that, we see a further moderation to around 4% to 5% levels. China has already indicated that it would like to become a more developed economy by 2035, and so an economic growth rate below 5% would correspond.

Driving that slowdown is the simple fact that China’s working age population has started to shrink, and it is increasingly more difficult to eke out further productivity and technology gains. China has also been prioritizing the rebalancing of its economy for some time, looking to better reflect the three core pillars of growth—exports, fixed asset investment, and consumption.

Until 2008, exports dominated in terms of economic growth, while 2009 saw a sharp increase in fixed‑asset investment to tackle the problems that the global financial crisis brought. Since then, policymakers have been actively targeting domestic drivers for economic growth. And there are encouraging signs of success, as export dependence has fallen in recent years. But with the services sector still only constituting around 60% of GDP, there is still some way to go to match developed economies.

Shifting Priorities With a Focus on Innovation

China remains the major manufacturing hub of the world, but the composition of what it manufactures is shifting from pumping out cheap products for the western world to consume to higher value‑added items. Rising labor costs and the employment of artificial intelligence (AI) and robotics across swathes of industry have triggered a major change in the economy’s direction—nudged by trade wars with the U.S. and other countries like Australia.

We have seen significant investment in research and development (R&D) for the last few years. Today, China is leading the way in many up‑and‑coming technologies, spanning artificial intelligence and digital currencies to mobile banking, health care, robotics, and 5G technology. We expect that Chinese companies will narrow the AI gap with their U.S. counterparts quite significantly in the next few years. This is supported by abundant engineering talent, deep pools of private sector investment, and large amounts of digital data for deploying machine‑learning techniques. Companies also have government support in terms of regulation and research funding.

The rise of technology and innovation represents a meaningful shift in direction for China’s economy that is probably underappreciated by the market. Some believe that China is just mimicking U.S. companies, with Alibaba and Tencent as the eBay and Facebook of China. However, we believe this does not reflect the reality, with these companies leading the way in many fields. The top‑down drive to push innovation will continue, and we may see some failures along the way, but the direction of travel is clear.

China’s Economic Road Map

China is often accused of a lack of transparency, but when it comes to the economy, it is a different story. Since 1953, China has published a five‑year plan that details economic development goals for the next five years. The 14th Five‑Year Plan (2021–2025) was drafted during the fifth plenum held in October 2020 and will be finalized at the National People’s Congress in March 2021. Guidelines for the plan focused on President Xi Jinping’s “dual circulation” theory, sustaining higher‑quality growth through encouraging domestic markets, innovation, and reform.

China’s Economic Road Map

The 14th five-year plan (2021–2025)—three key goals

For illustrative purposes only.

Beijing views boosting domestic demand, upgrading supply chains, and seeking self‑sufficiency in key technologies as ways to hedge against external uncertainties and challenges. Dual circulation also supports the need for greater reliance on homegrown technology, and we expect a trend toward greater spending on R&D within capex budgets in the coming years.

Challenges Ahead, but Rising Consumerism Should Help Drive the Economy in a Different Direction

It is no secret that China faces a number of headwinds, including slowing growth, a high debt‑to‑GDP ratio, an aging population, U.S. trade war tariffs that are still in place, and lower potential growth as resources shift into lower‑productivity services. We may also see exports suffer from improved work resumption in other economies as the pandemic is gradually controlled.

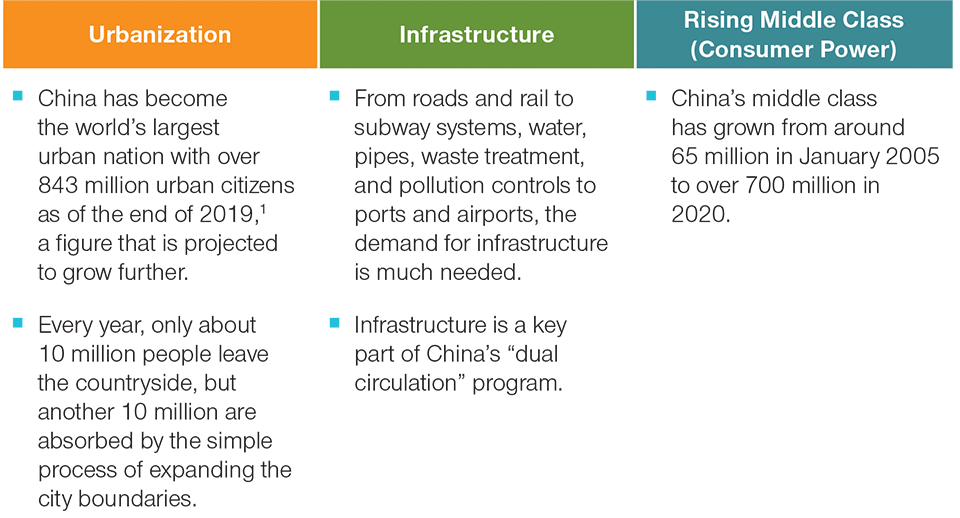

But the long‑term drivers remain. Urbanization, infrastructure, and a rising middle class provide pillars for future growth. There also may be a misconception that urbanization is largely about people moving from rural China to towns and cities. Instead, we believe its main feature is the upgrading of living space and amenities.

Some commentators perceive, incorrectly, that urbanization is purely about expanding numbers. We see it as expanding spending, as existing urban households upgrade from dilapidated state apartments to modern and often much larger apartments or houses.

The rise of the middle class should also help power China in a different direction. That comes with a rise in disposable income with household income having grown at around 10% annually. This increased income will likely engender greater spending and subsequently help drive the domestic element of economic growth upward.

Long-Term Drivers for China’s Economy

As of March 2021.

1 Source: World Bank.

Alongside household consumption, fixed‑asset investment will also remain a major theme. The large growth in urban housing space and vehicle population will need infrastructure. At the same time, China is finding answers to its aging population problem in pharmaceutical developments, with this industry already the second largest globally, fueled by government initiatives.

Focus on China’s Successful Record

Policies in China over the next few years will continue to focus on structural reforms, with policymakers continuing to seek lower, more sustainable growth, but of better quality. This is the long‑term goal, and investors should concentrate on China’s past record and its ability to achieve this.

WHAT WE’RE WATCHING NEXT

We shall continue to monitor macro data to ensure that the recovery continues. The data so far this year are encouraging. We are hearing of rising wages and greater employment. Data showed urban job creation reached 11.9 million in 2020 (versus a target of 9 million), while the official unemployment rate has continued to trend down throughout the fourth quarter to 5.2% in December.

Looking ahead, softening property and infrastructure investment may weigh on construction hiring, while service hiring should recover further as activities rebound. In the near term, we think the recent mobility restrictions and travel constraints during Chinese New Year may bring some downward pressures for domestic consumption, but we expect that to be temporary. After the first quarter, with COVID‑19 cases under control and the labor market improving, we expect consumption—in particular, service consumption—to recover further on stronger consumer income and confidence.

This is part of a series of TRP Insights focusing on China. The aim in our series Investing in China is to explore the key drivers for China’s economy, market opportunity, outlook, and our strategy for investing.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution retail investors in any jurisdiction.