February 2023 / INVESTMENT INSIGHTS

Headwinds for Equity Markets Starting to Diminish

Disinflationary forces point to a more benign environment

Key Insights

- Inflation appears to be peaking, while supply issues are easing. A likely peak in inflation coincides with equity market valuations that have become more attractive on a 3-, 5-, and 10-year average basis.

- Potential earnings downgrades, however, increase the importance of finding segments of the market where earnings remain resilient.

- Companies able to compound and grow earnings through the next stage of the equity cycle are likely to be rewarded.

Markets suffered heavy losses last year as many factors combined to produce higher levels of macroeconomic volatility. From surging inflation to subsequent aggressive central bank tightening, Russia’s war on Ukraine to China’s zero‑COVID policy, these unexpected and persistent shocks tested investors’ resolve. Looking forward, we expect volatility to persist, but we see increasing signs that the headwinds that characterized much of 2022 will begin to dissipate as we move through the year.

Markets Shifting Focus to Potential Tailwinds

Weighing multiple complex factors will demand active approach

As of January 2023.

For illustrative purposes only.

Source: T. Rowe Price.

Why 2023 May Be More Positive for Equity Markets

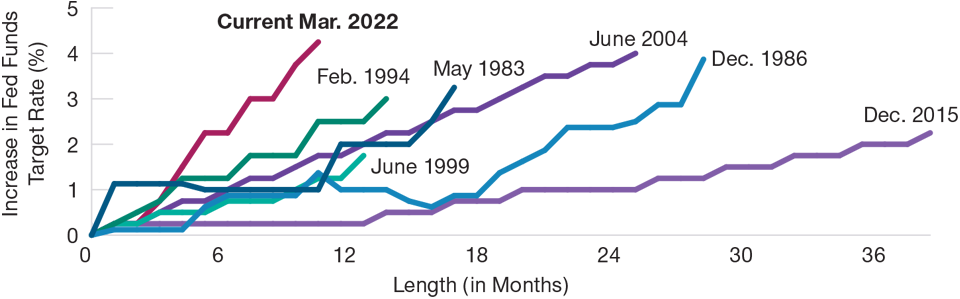

Part of the reason why 2022 was so tough for investors was the sheer acceleration and magnitude of interest rate rises throughout the year. With inflation ballooning to 40‑year highs, the U.S. Federal Reserve (Fed) embarked on delivering some of the sharpest sets of interest rate hikes in recent history (Figure 1). However, with recent inflation numbers showing signs of weakening, we are expecting the Fed to begin to slow and then pause its tightening cycle.

But why should inflation fall in 2023 and not enter a 1970s type spiral? We believe that inflation is likely to peak and fade from highs, in part driven by the same factors that contributed to the initial inflation spike.

Supply chain issues driven by the pandemic are now fading fast as China reopens and the world learns to live with COVID. While we have not resolved all the complex issues surrounding global supply chains—which broke down completely at the peak of disruption—huge progress has already been made, with supply conditions improving markedly.

At the same time, demand is falling and unemployment rising, given higher costs and an uncertain growth outlook.

Commodity prices have continued to weaken. Oil is trading at around USD 80 a barrel currently, while the forward curve points to a range of USD 60 to USD 70 per barrel further in the future. Gasoline prices likewise are flat, year on year, while other commodity prices have also eased back from their highs.

These factors take time to feed into neutral and then potentially disinflationary forces, but we expect that by summer we are likely to be at such a point, even before other disinflationary forces stemming from a low‑growth world begin to exert an influence. If inflation falls below the fed funds rate, this historically indicated a peak of the monetary tightening cycle.

Growth Versus Value—More Balanced and Nuanced

Growth stocks underperformed value and defensive stocks materially in 2022, with growth companies’ valuation multiples contracting sharply from their pandemic‑behavior‑enhanced levels. Higher interest rates are typically bad for growth stocks, and the succession of interest rate hikes last year proved very painful.

U.S. Federal Reserve Has Been Aggressive in Response to Inflation Spike

(Fig. 1) Delivering some of the sharpest sets of interest rate hikes in recent history

As of December 31, 2022

Data indicate start point for increase in fed funds target rate (%) and length in months the tightening cycle lasted.

Source: FactSet Research Systems Inc. All rights reserved.

Timing a change in fortune for either style is always difficult, but with valuations for defensives now elevated and energy and defensive sectors well owned, the case for owning these has weakened. Equally, while there is still a premium apparent within segments of the growth universe, that premium has narrowed materially versus value stocks. With broad market earnings downside increasingly becoming the focus for investors (for value, defensives, and growth stocks alike), we believe profit resilience and companies able to maintain shareholder returns will become even more important.

We are not making a specific style call but believe this is a moment in time when the market may very well return to earnings as the driver of equity returns, in what is likely to be a low‑growth or even recessionary world. If equity markets become more range‑bound and less directional, then stock picking is likely to take on even more significance, as will compounding of shareholder returns.

Equities Looking More Attractive on a Risk‑Adjusted Basis

Of course, no one valuation metric offers an investor “the answer,” with the last three years demonstrating that valuations are contextual. What we can say, however, is that interest rates are much higher than they were a year ago, while inflation appears to have peaked. But there are risks of earnings downgrades in 2023 as margins are pressured by inflation and low growth. It will therefore be important to search for segments of the market where you can find earnings resilience and even possible improvement, and that is where we are working hard.

Currently, equity markets are trading at an average valuation level as opposed to bubble or expensive levels, while positioning within markets remains decidedly defensive. That is clearly different to markets being extremely undervalued or pricing in a crisis. But a price‑to‑earnings ratio below the 3-, 5-, and 10‑year average is, in our opinion, a relatively solid starting point when thinking about forward risk‑adjusted returns.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.

February 2023 / MARKETS & ECONOMY