December 2022 / MARKET OUTLOOK

China Market Outlook 2023

“What should be” versus “What is likely to happen”

Key Insights

- Since the Party Congress, China has announced a significant easing in its zero‑COVID restrictions and more measures to stabilize residential property, which is encouraging.

- China is at a different stage of its business cycle compared with other economies and has room to ease policy as inflation remains low.

- With institutional holdings the lowest they have been in five years and valuations far below average, the risk/reward ratio for Chinese equities is favorable.

The Chinese Communist Party (CCP) Congress in October has led to meaningful volatility for China equities (Figure 1). Investors each have their own political views and a belief of how things should be. The Congress has shown further consolidation of power for President Xi Jinping, which came as a surprise to many. It’s therefore understandable why people have concerns over the future direction of China.

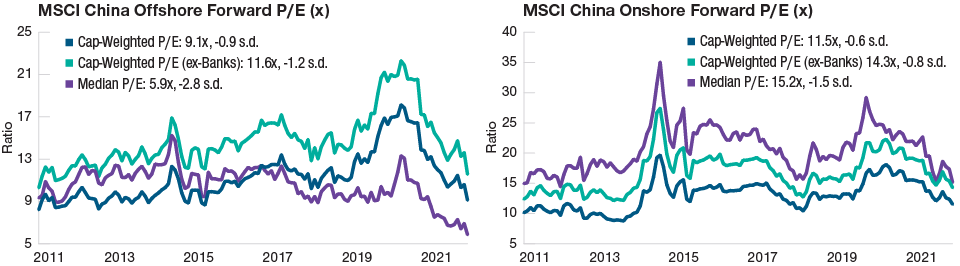

China Stocks Are Historically Cheap, Offshore and Onshore

(Fig. 1) Forward P/E ratio with and without Chinese banks

As of September 30, 2022. Past performance is not a reliable indicator of future performance. Actual outcomes may differ materially from estimates.s.d. = Standard Deviation.

Sources: Bloomberg Finance L.P. and MSCI (see Additional Disclosures).

However, as investors, we think it is critical to separate one’s political views from investment decisions. Investing is all about analyzing “what is likely to happen,” then adapting and positioning accordingly to construct a portfolio with a favorable risk/reward ratio.

Since the October Congress, the government has gotten its act together to address the two key issues that have dragged China’s economy and market lower over the past 18 months. First, there is a clear pivot to COVID policy and better visibility on an exit strategy. Second, the 16 measures supporting property may help set a floor for the industry. At the same time, China’s leaders have a full agenda, meeting foreign leaders to reset and stabilize the geopolitical situation.

COVID: Preparing for Reopening in 2023

China’s zero-COVID policy was a success in 2020 and 2021, which resulted in a stable economy while keeping the number of infections low. However, coming into 2022, Omicron brought new challenges. A cost/benefit analysis of the zero-COVID strategy (ZCS) started to shift to the negative side, especially since the strict Shanghai lockdown, which began on February 28 and did not end until August 7. In 2022, the ZCS has led to suppressed consumer demand, high unemployment, and weak business investment.

However, we think the announcement of “20 measures” on November 11 followed by more substantive relaxation measures on December 7 signals a clear turn in China's zero COVID policy. We believe China is ready to move on from its zero-COVID policy and has embarked on the path to reopening, though the journey could be disruptive and chaotic, with possible zigzags on the way. We also think the issue is likely to be largely behind us a couple of quarters from now, enabling China to return to its potential growth path. Higher-frequency data should be the first to improve. In October, domestic flights were down 62% year on year, subway passenger revenues fell 20% year on year, and cinema takings were down 72% year on year.1

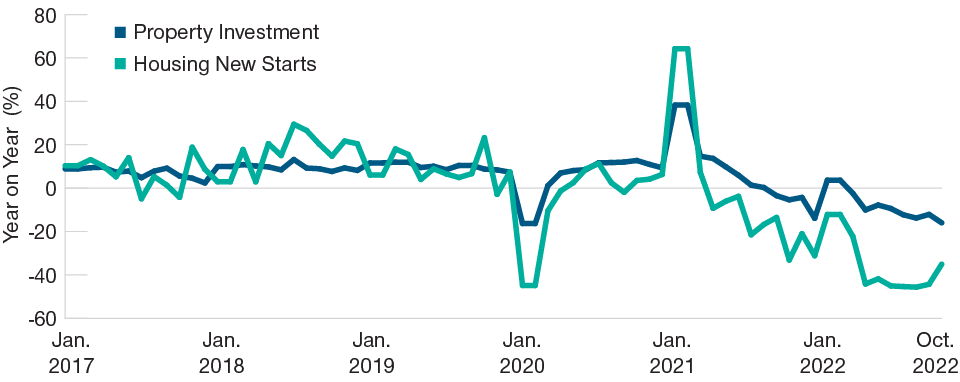

Property Sector: From “l Shaped” to “L Shaped”

China’s property market has declined sharply in 2022, with sales down 33%2 from their peak in the fourth quarter of 2020 and housing new starts down 37.8%3 in the first 10 months of 2022. Among China’s top 100 developers, over 90% are in a distressed situation, with bonds trading below 70 cents on the dollar. However, post-Congress we have seen more coordinated efforts to support the sector.4

Property is critical to China’s economy, contributing 10% to gross domestic product directly in 2021, or 25%5 if we include property‑related supply chains. We think that China’s property market has passed its peak and that long-term demand will probably be around half of the 2021 figure. However, a steep decline has already happened in 2022 (Figure 2). We don’t expect a V-shaped recovery in property but would expect to see a more stable situation in 2023.

China Property Sector Close to Bottoming

(Fig. 2) Housing new starts and property fixed asset investment

As of October 31, 2022.

Source: Macquarie Desk Strategy, China Macro, November 13, 2022.

The residential property slowdown will inevitably lead to slower economic growth for China over the next several years compared with the pre-pandemic trend. However, by proactively addressing the issues in property, it helps China to solve many structural problems and drive more sustainable growth in the longer term.

Geopolitics: China Remains an Essential Part of the Global Supply Chain

China’s supply chain strength is robust despite all the concerns on decoupling. Foreign direct investment into China has increased by about 20% year-to-date in 2022. China’s manufacturing capex in 2021 accounted for over 60% of the global total, and manufacturing output accounted for 30% of the global total, record-high percentage shares in both cases.

China has lost share in labor-intensive industries such as apparel, furniture, and electronics assembly. On the other hand, has been quickly gaining share in technology‑intensive areas like auto, equipment, electronic components, etc. China’s demographics has turned from tailwind to headwind, but its education/engineering dividend is just starting. Annual new STEM (science, technology, engineering, and mathematics) graduates in China are higher than for OECD (Organization For Economic Cooperation and Development) countries combined.

We do see selective decoupling happening in strategic high-tech industries, such as leading-edge semiconductors, biotech, and potentially electric vehicles also. That may slow down China’s development in certain areas, such as high-performance computing, Artificial Intelligence, etc. On the other hand, the concerns on supply chain security have helped to accelerate local substitution in power, semiconductors, analog, and medical devices, etc.

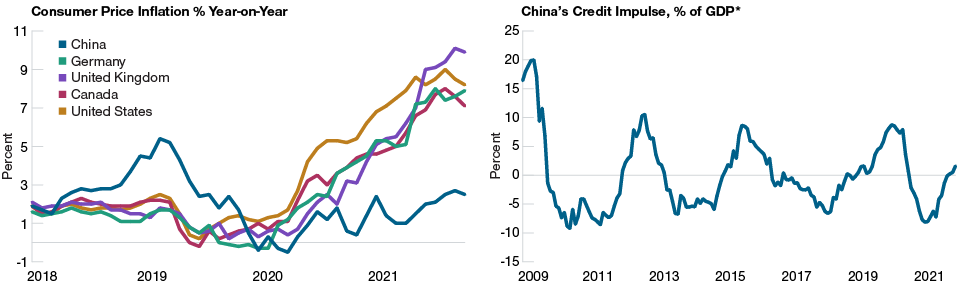

Business Cycle at Unique Stage vs. Other Major Economies

China is currently at a very different stage of its business cycle compared with other major economies (Figure 3). While other major economies are tightening to fight decade-high inflation, China has room to ease as inflation remains moderate. The divergence in inflation is the result of the different response to the pandemic. China’s priority during COVID was to protect supply, while consumer demand and employment remained weak.

China: A Different Stage of the Credit Cycle

(Fig. 3) Less inflation, more room for credit growth

As of August 31, 2022.

*Credit impulse equals annual change in new credit expressed as a share of GDP.

Sources: CEIC, PBoC, Morgan Stanley Research, FactSet Research.

The stable inflation outlook provides a favorable backdrop for liquidity. If we take the credit impulse as an indicator of China’s monetary cycle, the People’s Bank of China started to tighten in mid-2020 as the economy recovered strongly from the initial COVID lockdown. That was part of the reason for the slowdown we have been seeing in the economy over the past 18 months. The credit cycle turned at the beginning of 2022 when China began to loosen at the margin. But monetary policy has not flowed through to the real economy because of the extended COVID lockdowns as well as the property market correction. As both of these issues are expected to improve in 2023, the credit multiplier is likely to strengthen.

Investment Outlook

The past 18 months have been challenging for investors in Chinese equities. However, we have seen early signs of things turning around. With institutional holdings the lowest they have been in over five years and cyclically‑adjusted valuations far below average (Figure 1), the risk/reward ratio is favorable.

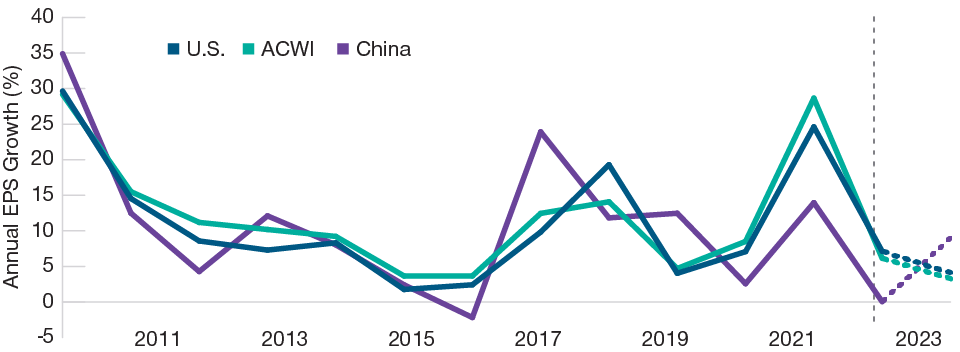

China’s corporate profits were suppressed in 2022 due to COVID and the property decline. However, we think they might have troughed. Consensus is expecting China’s 2023 earnings per share (EPS) growth to accelerate to 10% from 2% in 20226 (Figure 4). On the other hand, global EPS growth (MSCI ACWI) is expected to decelerate from 7.5% in 2022 to 3.7% in 2023.7

China Earnings Expected to Rebound in 2023 as U.S. and Global Earnings Slow

(Fig. 4) Year-on-year trailing EPS growth plus consensus forecasts

As of November 23, 2022. 2022 and 2023 values are consensus forecasts. Past performance is not areliable indicator of future performance. Actual outcomes may differ materially from estimates.

Sources: DataStream, FactSet, I/B/E/S, MSCI, Goldman Sachs Global Investment Research.

A Well-Balanced and Flexible Portfolio

In view of the considerable uncertainties in 2022, we have maintained a well‑balanced, diversified portfolio to navigate the market volatility. Themes that we are following closely include:

- Best growth assets in China that emerge stronger from the economic downturn, in our view. Examples include online recruitment, shopping mall operators, and hotel chains. COVID has been a significant headwind for them in 2022, but we expect a good setup for 2023/2024.

- Businesses with idiosyncratic drivers that are doing well despite the weak macro environment, such as auto parts and industrial companies levered to energy transition, shipbuilding, oil field services, etc.

- Defensive businesses with a historically attractive total return and improving outlook in 2023. That includes GARPY “growth at a reasonable price and yield” and value names in consolidating industries.

With better visibility on COVID and property in 2023, we expect various domestic-related sectors–including consumer discretionary, business service, recruiting, advertising, etc.–to accelerate. These are areas where we tend of find some very strong business models. We expect to find more attractive opportunities in these areas as the economy improves.

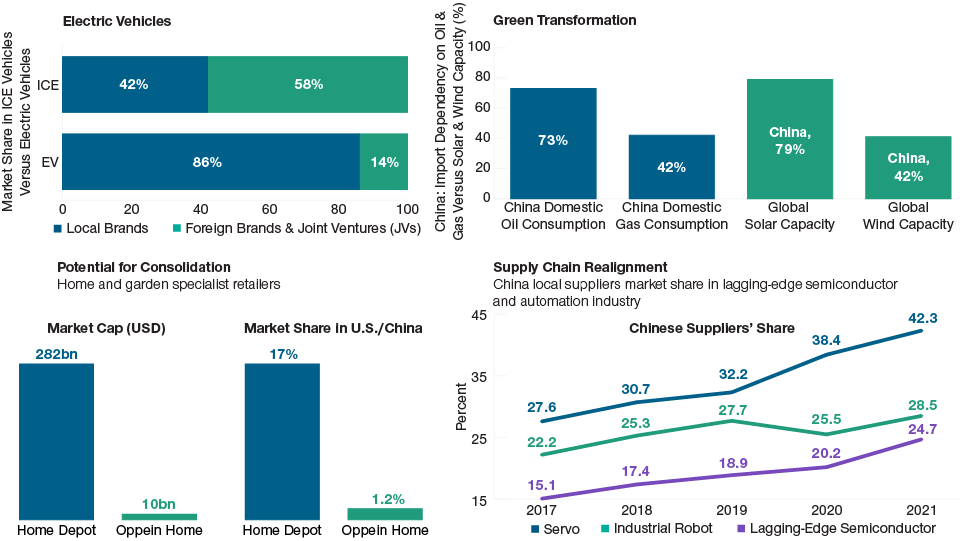

China: Where We See the Opportunities in 2023

(Fig. 5) No shortage of key investment themes

As of September 30, 2022. For illustrative purposes only. These charts are not intended to be investment advice or a recommendation to take any particularinvestment action. Using latest available data.

Sources: Goldman Sachs, SolarZoom, CPIA, Jefferies estimates, Credit Suisse, SMIC, Hua Hong, TSMC, MIR Databank, T. Rowe Price analysis, and Euromonitordatabase. ICE = internal combustion engine. ICE vehicles are conventional vehicles powered solely by an internal combustion engine.

The specific securities identified and described are provided for informational purposes only and do not represent recommendations.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.