April 2024 / INVESTMENT INSIGHTS

The US economy has defied recessionary fears. What now?

An economic “soft landing” is undoubtedly positive, but there are reasons to be cautious

Key Insights

- The risk of a U.S. recession has notably decreased in 2024, and this is encouraging for equity markets in the near term.

- However, equity and credit risk markets are pricing in a great deal of optimism that the current regime of robust growth and disinflation will persist.

- Given this backdrop, focusing on reasonably priced companies demonstrating durable growth, and supported by solid fundamentals, seems appropriate.

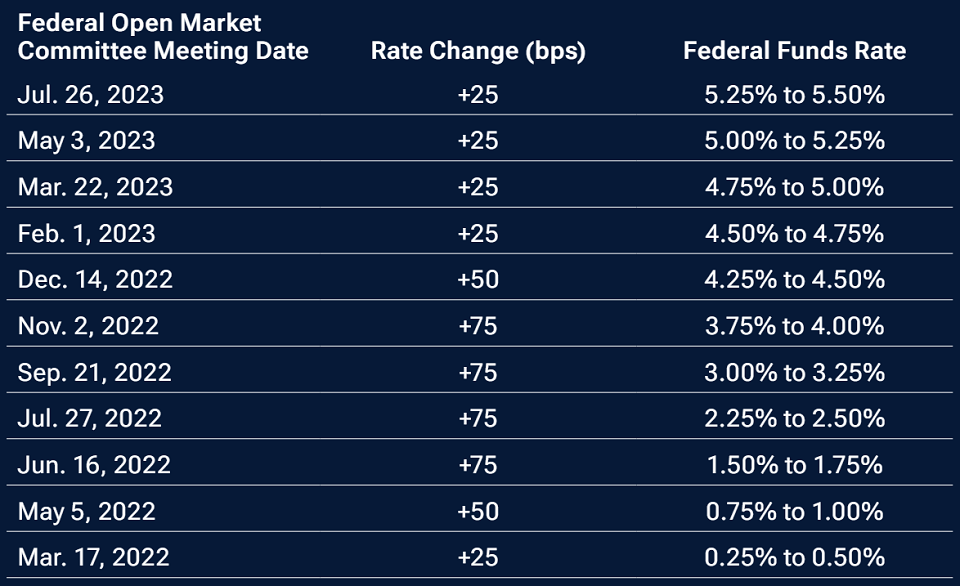

The U.S. Federal Reserve (Fed) appears to have pulled a rabbit from the hat and orchestrated a much‑hoped‑for economic soft landing. Despite an extreme campaign of monetary tightening (Fig. 1), macroeconomic conditions have meaningfully improved in recent quarters, enabling the Fed to pivot from its aggressive tightening bias and creating a scenario in which inflation has potentially been tamed without triggering a recession. So, what does this mean for U.S. equity investors in 2024 and beyond?

Taming U.S. inflation

(Fig. 1) Federal Reserve interest rate hikes 2022–2023

As of March 8, 2024.

Source: Refinitiv Eikon. © 2024 Refinitiv. All rights reserved.

Strong stock picking with a particular focus on managing risk

The risk of recession in 2024 has notably decreased, and this is very encouraging for equity markets in the near term. Real U.S. growth has stayed resilient while inflation has fallen substantially from the generation‑high levels of 18 months ago.

Nevertheless, renewed “risk on” confidence warrants caution, particularly when it is undiscerning, as was the case at the end of 2023 with the sharp market rally being led by low‑quality/higher‑risk stocks. History shows that the outperformance of companies lacking fundamental support has not tended to persist for long. And it proved so again this time, with higher‑quality, fundamentally stronger companies assuming market leadership once more since the start of 2024.

In the near term, the path of least resistance for U.S. equities looks like a continuation of the move higher that began in late 2023. However, with a number of ongoing risks to the outlook, sentiment will continue to fluctuate in line with the latest data releases or geopolitical developments. Given this prospective backdrop, good stock picking—targeting quality companies with durable or accelerating growth and reasonable valuations—is vital. Equally important will be managing risk and having the courage to “lean against the wind” should market sentiment become irrational or fundamentally unsupported, as was the case in late 2023.

A dynamic economy with structural advantages

One risk surrounding the U.S. equity market relates to the current high valuation levels, raising questions as to whether such levels are sustainable. While these concerns are amplified by the elevated valuations of a handful of stocks at the top of the market, it is also true that broader market valuations are currently expensive compared with history and versus major market peers. However, there are reasons to suggest that the current U.S. valuation premium is not only reasonable, but is likely to continue.

Risk appetite and valuations typically rise when an improving economic outlook enhances investors’ confidence that companies will be able to deliver consistent profit growth. And stocks tend to move higher as long as earnings expectations rise, even if valuations (as indicated by forward price‑to‑earnings ratios) are elevated. This is the environment we are currently in, with higher valuations being driven by increased earnings expectations.

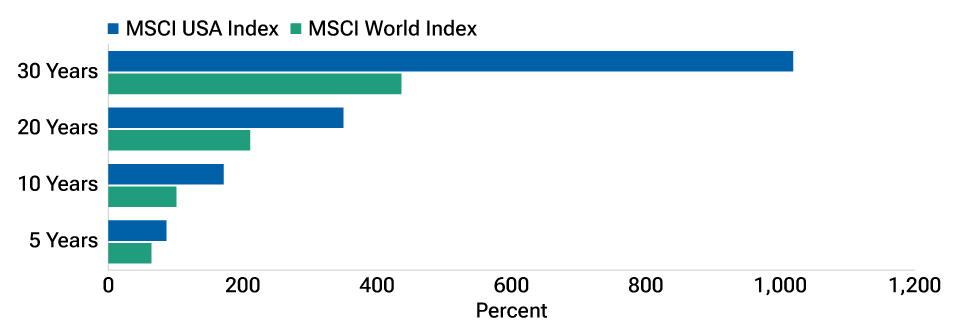

U.S. equities have consistently outperformed

(Fig. 2) MSCI USA Index vs. MSCI World Index comparative returns

As of March 8, 2024.

Past performance is not a reliable indicator of future performance.

Source: Refinitiv Eikon, analysis by T. Rowe Price. Cumulative returns. © 2024 Refinitiv.

All rights reserved.

In terms of longer‑term sustainability, the U.S. economy is diverse and dynamic and features certain structural advantages that have helped U.S. equities outperform global stock indices over the last 5‑, 10‑, 20‑, and 30‑year periods (Fig. 2). With attributes including a large, well‑educated, and productive workforce; a culture that embraces capitalism and champions entrepreneurship; and leadership in technological innovation, a higher market valuation may not be quick to revert to long‑term averages.

Key risks to the outlook

Current U.S. data are consistent with an economic soft landing as the most likely near‑term scenario. Growth is robust, the labor market is healthy but no longer overheated, corporate earnings growth is positive overall, and the Fed historically has been inclined toward a more dovish tilt during an election year. However, equity and credit risk markets are pricing in a great deal of optimism that the current regime of robust growth and disinflation will persist. We think there is reason to be a little more cautious. Given the dogged resilience of the economy over the past year in the face of severe monetary tightening, the potential for overheating in 2024 as monetary policy is eased cannot be ruled out. This could lead to stickier, or even reaccelerating, inflation, particularly if oil prices move higher.

This scenario would not only be detrimental for lower‑quality, highly levered companies, it would also have negative implications for longer‑duration stocks, including less cash‑generative technology companies. These businesses tend to be more reliant on future earnings and so are more vulnerable to any increase in the interest rates used to discount those earnings.

Targeting durable, reasonably priced growth

While the positivity surrounding the U.S. soft landing is encouraging and would arguably benefit cyclical companies, many of these stocks appear to be pricing in considerable optimism, with seemingly little regard for any potential deterioration in the outlook. We remain more circumspect than this. As such, more reasonably priced companies demonstrating durable/accelerating growth, appear appropriate in the current environment.

Investment opportunities are underpinned by a “four‑pillars” framework that considers and scores each company on the basis of quality, market expectations, fundamentals, and valuation. Currently, there appear to be a number of stocks within the energy sector, for example, that fit this reasonably priced growth profile. Similarly, while not all parts of the technology sector look appealing, certain companies geared to the exciting potential of artificial intelligence (AI) appear reasonably priced. These specific investment areas are discussed in more detail below.

Looking ahead in 2024

The outlook for equities early in 2024 appears considerably brighter than during most of 2023. Growth remains resilient, the labor market is healthy but no longer hot, and the Federal Reserve has already made its easing intentions clear. It is also worth noting that in every election year since WWII where an incumbent has been up for reelection, U.S. equities have finished the year an average of 13.6%1 higher than they began. The key risk to this outlook, in our view, is that the economy starts to heat up once more as the year progresses. The oil market could tighten in 2024, services inflation is still elevated, while a too‑dovish Fed could also stoke renewed inflationary pressure.

That said, we remain confidently positioned for a prospective “soft landing” environment, leaning toward good‑value, higher‑growth business with fundamental support. At the same time, we continue to tread carefully around low‑quality, highly levered companies (e.g., the stocks that rallied sharply into the end of 2023) and also long duration, noncyclical assets given their heightened sensitivity to any potential rise in inflation.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.