October 2021 / INVESTMENT INSIGHTS

Taking the Temperature on Climate-Related Shareholder Proposals

Complexity and variability of resolutions demand a measured approach to voting.

Key Insights

- Climate‑related shareholder resolutions were prominent during the 2021 proxy voting season, reflecting the heightened priority of climate issues.

- Climate‑related resolutions are set to increase even further in the coming years as institutional investors file proposals as part of escalation strategies.

- While climate issues warrant urgency and votes can be contentious, the variability of resolutions tabled demands a nuanced, case‑by‑case approach to voting.

Climate‑related shareholder resolutions are often prominent topics during proxy season, being of great interest to investors, advocacy groups, and the public at large. This is perhaps not surprising given the many damaging, if not devastating, weather‑related events affecting many countries and communities in recent years. With a range of scientific disciplines forecasting an escalation in the potential detrimental impacts of a rapidly warming atmosphere in the coming decades, the spotlight is firmly on how companies are contributing to climate change and how investors are preparing for the associated systemic risks.

Rising concern among investors around climate change and its effects has been reflected in a growing number of shareholder resolutions linked to climate in recent years. Indeed, a number of climate‑related proposals were filed in the 2021 proxy season (as of March 31), covering a multitude of topics, particularly in Europe and the U.S. The season provides a timely opportunity to illustrate our approach to addressing votes in what can be a particularly heated area of debate.

The intensifying focus on climate, alongside new regulatory and industry initiatives, are working to compel greater levels of transparency from asset managers about their voting rationales. When it comes to shareholder resolutions, we take a case‑by‑case approach when determining our voting recommendations, as we consider both the characteristics of the change requested and the practicality of any prescriptive approaches that may be stipulated alongside it.

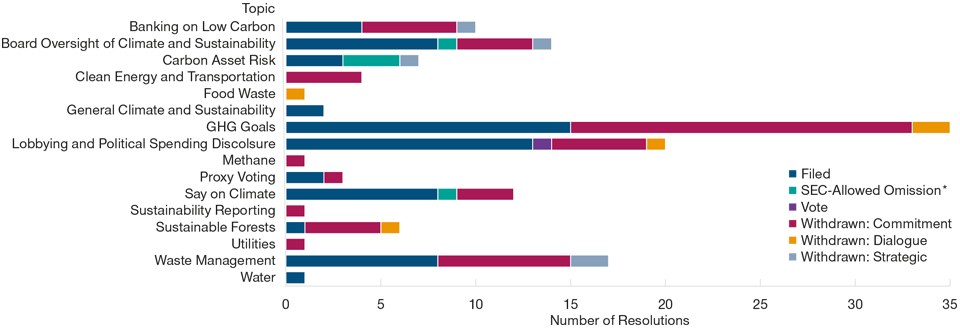

Climate Resolutions Make a Mark on the 2021 Proxy Season

In this year’s proxy voting season, climate‑related shareholder resolutions were prominent, particularly within high‑impact industries, such as the energy, industrials, and financials sectors. According to data from sustainability organization Ceres, there were 136 climate‑related shareholder proposals tabled between July 1, 2020 and March 31, 2021 (as of March 31), with just under half of these progressing to a vote at the respective company annual general meetings (AGM). The remainder were either withdrawn or omitted following consultation with the U.S. Securities and Exchange Commission (see Figure 1 footnote).

Climate-Related Resolution Topics—2021 Global Corporate Proxy Season

(Fig. 1) Shareholder resolutions on climate issues are becoming more prominent

As of March 31, 2021.

*Relates to U.S. companies only. In select cases, the U.S. Securities and Exchange Commission (SEC) might allow a company to omit a shareholder resolution from the proxy voting ballot. These SEC-Allowed Omissions are based on a “no-action letter.” Companies may ask the SEC whether it would recommend enforcement action against the company if a shareholder proposal was left off the ballot. The SEC may respond with a “no-action” letter, which indicates that they would not pursue enforcement action.

Source: Ceres.

Encompassing a broad range of topics, the most common resolutions filed in 2021 were those requiring companies to set targets to reduce greenhouse gas (GHG) emissions and to report on climate‑related lobbying. Other climate‑related topics addressed by these resolutions, on matters other than GHG emissions, included subjects like waste management (for example, plastic waste disposal and recycling initiatives) or proposals linked to deforestation. Of the 31 climate‑related shareholder resolutions from the 2021 season that have been tagged as notable votes by Ceres, Climate Action 100+, or ShareAction and that we considered as being directly related to climate, average shareholder support was 44% in favor of the resolution.

In addition to shareholder resolutions, the 2021 AGM season featured a number of “vote no” campaigns instigated at various U.S. utility and energy companies, where shareholders were encouraged to vote against directors at companies seen as laggards on climate issues. None of these ultimately proved successful and gained little support across the board.

Say on Climate

The season also saw a marked increase in “say on climate” votes, where a company asks its shareholders to approve its climate strategy or transition plan via a nonbinding vote. The first example of this kind of vote was filed by the Children’s Investment Fund (TCI) at the Spanish airport operator, Aena, in October 2020 and won support from 98% of its shareholders, including T. Rowe Price. TCI is Aena’s second‑largest shareholder after the Spanish government,1 and the impetus for filing the resolution was frustration at management’s responsiveness to their requests for improved climate disclosure.

As originally championed by TCI, companies are asked to provide (i) annual disclosure of emissions and a plan to manage those emissions and (ii) an annual advisory vote on the plan and performance relative to plan. In practice, we have seen a range of implementation approaches. Some have proposed a triennial vote on the climate strategy instead of an annual vote on the reporting; other companies have offered both. Some companies are taking a “one and done” approach, while others are offering an ongoing commitment to holding a shareholder vote.

In some instances, the company has already agreed to undertake the say‑on‑climate exercise, so the vote takes the form of a management‑sponsored proposal, with a board recommendation of “for.” In other instances, the company has not agreed to implement say‑on‑climate, so the vote takes the form of a shareholder resolution. Say-on-climate proposals tended to find greater support in Europe than in North America.

Resolution Quality and Intention Must Be Carefully Evaluated

Groups filing climate‑related resolutions are not always shareholders themselves. Activist parties such as environmental and social advocacy groups can seek to harness investor voting power at AGMs to achieve their objectives. This is more common in certain major markets, like the U.S., the Nordics, and Japan, where the requirements for filing resolutions are less onerous. Some groups are known to file resolutions at the same company over a period of several years with only minor changes to the proposal from year to year. They aim to keep sustained pressure on the company even if shareholder support for the resolution is initially low, meaning that climate‑related proposals do not necessarily disappear after an unsuccessful attempt.

A wide range in the quality of shareholder proposals is evident, particularly where the parameters allowing resolutions are less demanding. Resolutions filed by individual investors tend to be lower quality, while those filed by large, institutional investors are usually more substantive and typically warrant more detailed consideration. The quality of the resolutions is often reflected in the overall regional support secured.

The degree to which a proposal is prescriptive as to how a company should address a climate issue can also vary. This can influence our decision to support or oppose a particular resolution. For example, even if we agree in principle, we may not always agree on the remedy.

Similarly, resolutions filed by advocacy groups at multiple companies can sometimes ignore differences between the companies, rather than being tailored to their specific activities. For example, resolutions filed this year at BP and Shell by a campaign group were almost identical, requesting that both companies set GHG emission reduction targets covering scope 1–3 emissions.2 Given that both companies already have such targets in place, the proposal did not ask for any material additional disclosures or targets. In contrast, a similar resolution tabled at Chevron was supported by a majority of shareholders as the firm has not set scope 3 emission reduction targets.

Fundamental, Case‑by‑Case Analysis

At T. Rowe Price, the analysis of climate‑related shareholder proposals by our Governance and Responsible Investing teams is conducted on a case-by-base basis. To reach a vote recommendation, we consider:

- The specific circumstances of each company (including the current level of disclosure);

- The company’s climate strategy; and

- The materiality of the issue for the company, i.e., the extent to which it relates to the company’s operations.

As discussed, we are unlikely to support resolutions that are excessively prescriptive (be they climate‑related proposals or otherwise), as this usually equates to the proponent, in essence, attempting to micromanage the company. Similarly, if we think that the company is already taking sufficient action to address the stated concerns, we will likely withhold our support.

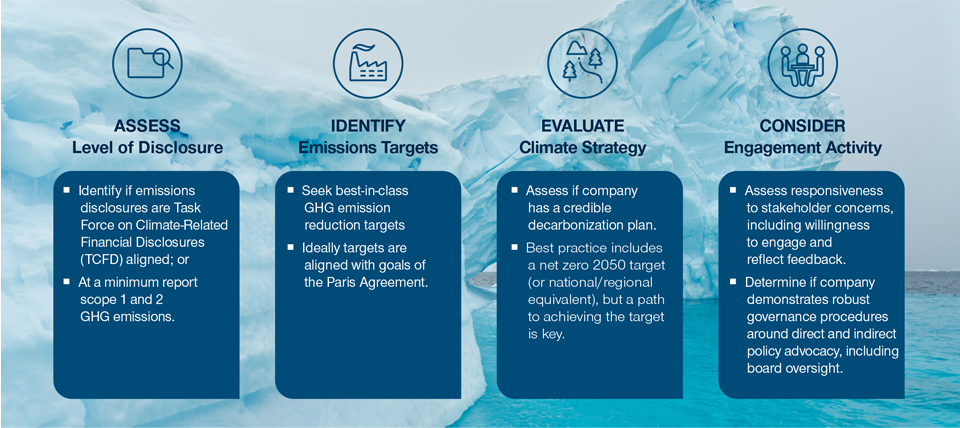

While the nature of our assessment of a company’s actions can vary according to the region and industry, specific measures we consider include those detailed in Figure 2.

Framework for Assessment of Climate‑Related Action

(Fig. 2) Key areas of analysis in a fundamental, case‑by‑case approach

For illustrative purposes only and subject to change.

As of October 2021.

Analysis: T. Rowe Price.

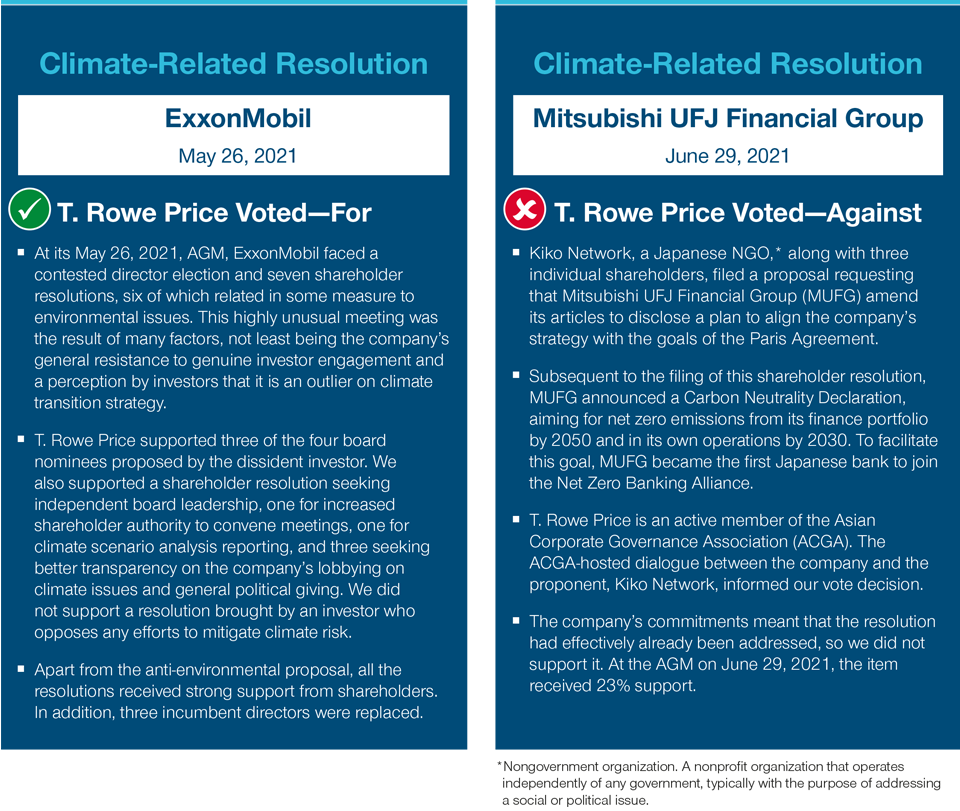

2021 Proxy Season—T. Rowe Price Voting on Climate‑Related Shareholder Resolutions

In line with this fundamental assessment framework, included below are two examples of how we approached specific climate‑related shareholder resolutions during the 2021 proxy season and the reasoning that informed our voting decision in each case.

Climate‑Resolutions Set to Remain in the Spotlight

Beyond shareholder proposal filings, many investors are also exploring ways to adopt climate change voting strategies that express concerns through voting on routine agenda items, such as director elections, executive compensation proposals, or the approval of annual reports. In the absence of a dedicated agenda item where investors can express their views on environmental and social issues, addressing such concerns via votes on routine agenda items could also become a more common practice.

Concerns about climate change risks are an increasing priority among investors around the world. Worries around the issue are set to drive ever greater numbers of climate‑related shareholder proposals on annual proxy ballots. The urgency of climate change, growing community concern, and regulatory pressure are adding to the imperative for transparent and structured approaches to voting recommendations.

The diverse range of resolution topics, quality, and proponent motivations means a generalized approach is impractical. Ultimately, achieving outcomes that will drive companies to real action on climate change demands developing insights into the quality and potential effectiveness of each of the actions proposed.

Looking Forward to the 2022 AGM Season

At T. Rowe Price, we believe that say on climate, as a means of structuring the dialogue between companies and their shareholders, must not detract from the responsibility of the members of each company’s board to assess, set, and oversee implementation of the company’s climate transition plan. Votes on the election of board members remain the ultimate mechanism for shareholders to express concerns over a company’s management of climate risk.

In 2022, T. Rowe Price plans to step up its current voting against directors who fail in the oversight of material environmental, social, or governance risks. Companies in sectors highly exposed to the impact of climate change and that have failed to demonstrate sufficient preparedness for a low‑carbon transition will be in scope for a vote against the Board chair, or other relevant committee member.

The specific securities identified and described above are for informational and illustrative purposes only, do not represent recommendations or securities purchased and sold. No assumptions should be made that investments in the securities mentioned were or will be profitable.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution retail investors in any jurisdiction.

November 2021 / MARKETS & ECONOMY