December 2021 / INVESTMENT INSIGHTS

A Digital U.S. Dollar Will Strengthen the Currency’s Global Dominance

A Fed-backed CBDC will dwarf those of other countries

Key Insights

- The emergence of central bank digital currencies is set to reduce the U.S. dollar’s dominance of invoicing and foreign exchange.

- However, the global availability of a Fed‑backed digital currency is likely to reinforce the U.S. dollar’s status as the world’s most important currency.

- The increase in U.S. dollar dominance is likely to be greatest in commodity‑exporting economies.

The emergence of central bank digital currencies (CBDCs) is likely to increase—rather than reduce—the U.S. dollar’s dominance in the international financial system. Although digital currencies from other central banks may offer advantages to local investors in certain circumstances, the global availability of a U.S. Federal Reserve‑issued digital currency will ultimately strengthen the U.S. dollar’s position as the world’s most important currency.

In the fourth and final article in this series, we discuss the consequences of CBDCs for the future role of international trade and the global financial system.

A U.S. Dollar Digital Currency Would Dominate Trade Invoicing

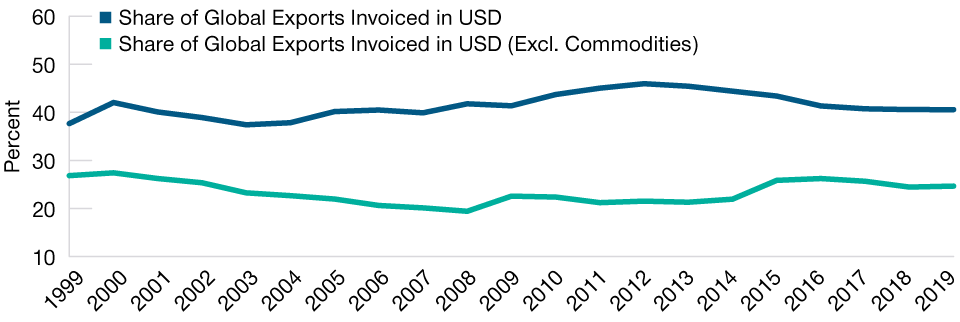

The U.S. dollar currently dominates global trade invoicing, composing around 40% of all invoices. One reason for this is that many commodities are priced and traded in U.S. dollars. However, even if commodity exports are excluded, the U.S. dollar share of invoicing is still very high at 25%—a remarkable figure given the share of exports destined for the U.S. is 10%.1

Another reason for the U.S. dollar’s dominance is that emerging market currencies are prone to volatility, which can be a source of market risk for firms as transfers can take a few days to settle. This risk can be reduced by conducting transfers in U.S. dollars.

However, there are also disadvantages of using the U.S. dollar for invoicing. One is that it can be expensive. Another is that it can introduce a risk associated with the mismatch between revenues and costs—for example, a firm may import raw materials priced in U.S. dollars but receive revenue in local currency, thereby exposing itself to a depreciation in the local currency.

The U.S. Dollar Dominates Trade Invoicing

(Fig. 1) It composes around 40% of global export invoices

As of December 31, 2019. Most recent data available.

Source: Boz, et al. (2020), “Patterns in Invoicing Currency in Global Trade,” IMF Working Paper 20/126.

Investors can bypass these problems by using CBDCs, whose use of distributed ledger technology allows payments to be cleared instantly, reducing the credit risk associated with the settlement between banks and market risk linked to the volatility of currencies. Indeed, research trials show that cross‑border transactions via CBDCs can be completed within a few seconds rather than a few days.2 For these reasons, many central banks are looking closely at CBDCs.

However, while the introduction of CBDCs may reduce the advantages of using the U.S. dollar as a fiat currency for trade invoicing, it may ultimately reinforce the U.S. dollar’s dominance as a digital currency. A U.S. Federal Reserve‑issued CBDC will be highly credible, very liquid, and widely available—and hence more attractive to firms than most local CBDCs—although this will ultimately depend on the type of goods traded. Trade in commodites, which are priced and traded in U.S. dollars, are likely to continue to be invoiced in U.S. dollars and the USD CBDC when it is widely available. However, for non‑commmodity goods, firms are likely to switch to invoicing in local currency CBDCs to help alleviate the risk associated with a mismatch in revenues and costs.

A U.S. CBDC May Raise the Risk Premia of Emerging Market Currencies

As well as being the dominant currency for invoicing, the U.S. dollar is also the most important vehicle in foreign exchanges, making up 44% of all transactions. An important advantage of any CBDC is providing access to those previously excluded from the banking system, especially in emerging markets—and here, again, the global availability of a USD CBDC could reinfoce the dollar’s role as the global vehicle currency of choice.

In times of macroeconomic stability, citizens of emerging market countries may choose to rely on their local CBDCs for transactions, as both a medium of exchange and store of value. However, during a recession, whether local or global, they may prefer a USD CBDC over the local currency CBDC, especially in countries with histories of high inflation and weak fiscal credibility. The global availability of a U.S. dollar CBDC, even if only in small amounts, would enable these newfound savings to move to the global safe‑haven asset instantly, raising the risk premia of the local currency.

Stabilizing capital outflows would require either higher interest rates or higher inflation, exacerbating the initial shock. Local authorities could stop citizens from moving funds to a USD CBDC by implementing capital controls. However, while this is an option for some large emerging markets like China and India, capital controls have failed in many other smaller emerging market countries, either because their anticipation caused a large outflow or the reputational damage led to an outflow in the aftermath of the crisis. Furthermore, the existence of stable coins, which are pegged to the USD, would make it difficult for countries to impose restrictions.

Alternatively, the U.S. could impose restrictions that only U.S. residents are allowed to hold U.S. dollar CBDCs. However, this would be similar to a control on capital outflows, which would be politically controversial given that the U.S. has held an open capital account since the Second World War. Given current competition from stable coins, which are available around the world, we believe it is highly likely that a USD CBDC will also be accessible to non‑U.S. residents via intermediary institutions (rather than directly through accounts held at the Fed).

If this occurs, the broad global availability of a USD CBDC would likely amplify U.S. monetary policy spillovers to emerging market economies, especially those with high risk premia due to a history of high inflation and little fiscal credibility. In those countries, previously financially excluded citizens will likely prefer to hold part of their savings in USD CBDCs and hence be more reactive to changes in the Fed’s interest rate on USD CBDCs (citizens of these countries who can already access the formal financial system probably already react this way).

However, the effects would be much stronger if the large group of currently financially excluded people had access to both the local and the USD CBDC. In practice, this would mean that central banks in these countries would have to tighten by more and respond faster to Federal Reserve monetary policy tightening. To avoid these side effects, monetary policy coordination in CBDCs will likely become an important theme of central bank collaboration in the future.

CBDCs May Increase Risk of Financial Disintermediation

Our discussion so far has assumed that individuals in emerging market countries would adopt the USD CBDC as their preferred safe‑haven asset CBDC of choice. Why not a CBDC from another advanced economy? One answer to this is that few countries offer the liquidity and monetary policy credibility to achieve the necessary economies of scale as the U.S.—the Swiss National Bank, for example, is already intervening very heavily against safe‑haven flows. On the other hand, there are risks of instability associated with the eurozone. However, one of the key reasons the U.S. could allow global access to its CBDC is that the introduction of CBDCs in the U.S. is likely to have a much smaller impact on disintermediation than in other countries.

A CBDC is a claim on the central bank and is therefore a safer form of money than commercial money, which is a claim on the financial institution. The lower risk of holding CBDCs means that direct access to central bank money is likely to lead to a transfer of deposits from commercial banks to CBDC accounts held at the central bank. This process will accelerate during periods of economic crisis, when confidence in the banking system is reduced. Previously, individuals would be limited by the cost of holding cash (due to the inconvinience, storage costs, and risk of theft). However, the digital nature of CBDCs removes these limits and would allow individuals to easily transfer all commercial bank holdings to central bank money. The corresponding fall in commercial bank assets would raise financial stability concerns, have implications for bank funding and increase the risk of disintermediation.

Central banks are exploring whether CBDCs can be introduced without incurring these negative side effects. One possible solution is a cap on CBDC holdings, which would limit the amount individuals can transfer out of commercial bank deposits. In order to tackle the risk of disintermediation, central banks can utilize a hybrid model for CBDCs whereby private sector intermediarites handle retail services but the CBDC remains a direct claim on the central bank. For example, the “sand dollar,” introduced by the Central Bank of The Bahamas, has a holding limit and transaction limit in order to prevent a large fall in commercial bank deposits. Research on CBDCs from the People’s Bank of China on the digital yuan and from the Riksbank on the e‑krona have both focused on a hybrid framework for CBDCs.

Most of the proposed restrictions on CBDC availability stem from fear of disintermediation in countries that rely heavily on the banking system for financial intermediation.

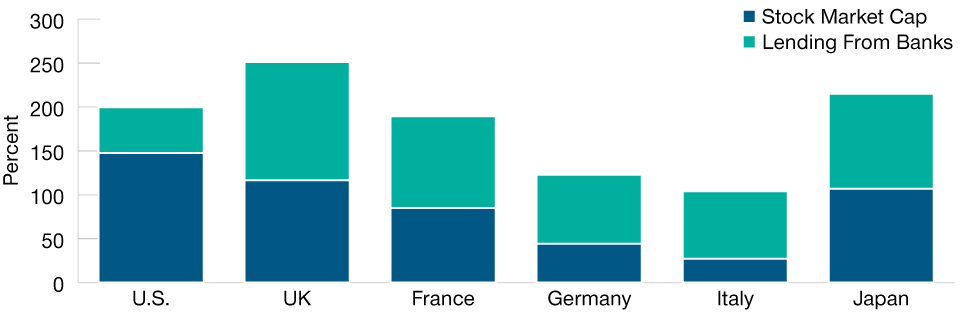

The U.S. financial system has much deeper and more developed nonbank capital markets than the rest of the world. Indeed, bank‑based finance only makes up about 25% of financial intermediation in the U.S., compared with 70% in the eurozone. Fear of disintermediation will therefore present a smaller hurdle to CBDC introduction in the U.S., meaning fewer restrictions on how much citizens are allowed to hold. Furthermore, private sector organizations have already promoted USD‑backed stable coins, which are freely accessible anywhere. To be competetive, a USD CBDC would have to adopt some of these features. Overall, we believe that the current U.S. financial structure therefore gives U.S. policymakers fewer disincentives to introduce an unrestricted USD CBDC and to make it a globally accessible financial instrument.

U.S. CBDC Dominance Will Likely Be Felt Most in Commodity‑Exporting Countries

The USD is the dominant currency in the international monetary system, and the impact of introducing a USD CBDC on a country will depend on a variety of factors. For countries with weak institutions, histories of high inflation, and low fiscal credibility, access to a USD CBDC is likely to strengthen the dollar’s dominance, raising the volatility and amplifying the boom and bust cycles in asset prices.

The increase in USD dominance is likely to be greater in commodity‑exporting EM economies as goods will continue to be priced in dollars and transactions in USD CBDCs are likely to become cheaper. In EM economies with strong fiscal frameworks and instutitional quality, however, consumers will be incentivized to switch to local currency CBDC transactions given the speed and efficiency benefits. Distinguishing between these two types of emerging markets will become increasingly important when investing within this asset class.

The Risk of Financial Disintermediation Is Low in the U.S.

(Fig. 2) The financial system includes a lot of nonbank capital

As of December 31, 2018. Most recent data available.

Sources: Haver Analytics and World Bank World Development Indicators.

However, the emergence of a U.S. dollar CBDC could make movements in the U.S. dollar more countercyclical. In times of global crisis, citizens across the globe (but especially those in countries with weak institutions) will likely convert their savings to a U.S. dollar CBDC, raising the demand for U.S. dollars and strengthening the currency. On the other hand, in times of economic stability, the cost of holding a U.S. dollar CBDC will probably outweigh the benefits for firms and households outside the U.S. Of course, the resulting large movements in capital flows into and out of the U.S. would have significant effects on bond yields as well. Understanding these dynamics, and how they are amplified by the introduction of a widely available U.S. dollar CBDC, will therefore be key for active global bond and currency managers.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution retail investors in any jurisdiction.

December 2021 / INVESTMENT INSIGHTS

December 2021 / INVESTMENT INSIGHTS