September 2021 / INVESTMENT INSIGHTS

The Cycle—Where Are We? Implications for Global Equity Investors

Complex environments need active management to help steer portfolios in the right direction

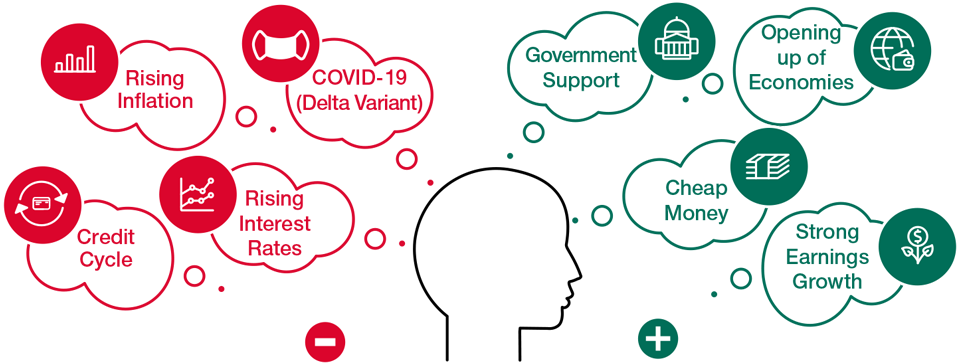

Equity markets have continued to make gains despite concerns around the new delta variant of COVID‑19 as accelerated vaccine distribution has helped fuel expectations of a relative “return to normal.” Within equity markets, much debate centers on the future path of interest rates, inflation, and economic growth. Here, we analyze where we believe we are in this current cycle.

Asset Prices Are High for a Reason

Asset prices are high because interest rates remain low, and there is no credit cycle to act as a disruptor. Both governments and central banks have proven to be a good backstop to a global pandemic that would have otherwise had much more severe consequences for financial markets without the unprecedented intervention taken. The outcome is that there appears to be little systematic risk if interest rates can stay at low levels and COVID‑19 slowly gets better. However, we are seeing ample examples of careless risk‑taking in financial markets. History suggests that this type of behavior should be actively managed within portfolios.

“Absurd” Inflation Is Likely to Fall

We are witnessing “absurd” inflation in many areas of the economy, as well as general inflation in the labor market. We agree with the U.S. Federal Reserve (Fed) that absurd inflation is transitory; lumber, DRAM,1 and used cars are pockets of absurd inflation we’d highlight. The question of whether labor inflation becomes embedded is still one to be resolved. While a degree of labor inflation is a good thing, an escalation would likely necessitate a change in monetary policy that could potentially disrupt the cycle.

We believe that demographics and technology, however, remain powerful structural forces that can continue to put downward pressure on long‑term inflation trends. These forces have not disappeared and should return as economies normalize.

Markets Most Afraid of Fed Mistake and a Rapid Increase in Interest Rates

We believe that the market’s (asset prices) greatest fear is that absurd inflation might lead to a Fed mistake. Specifically, a rapid increase in interest rates that causes a crisis and a flattening, or even an inverted yield curve. In this scenario, the price of virtually all assets would fall—stocks, bonds, real estate, art, wine, etc. We had a preview of this type of move in December 2018.

In June 2021, we saw the market panic at moving Fed dot plots and the indication of tightening. Any hint of tapering or rising rates seemed to imply a “crisis” to a market that clearly requires easy monetary policy to maintain balance.

We are wary of the level of interest rates today and believe that the price of Treasuries represents hedging and risk aversion more than being an accurate indicator of future economics. We believe interest rates should be higher, but not so much higher on an absolute basis that it would imply a dangerous change in regime.

Many Areas of Growth Investing Appear Crowded and Full of Momentum

The valuation of many growth assets increased significantly during the worst of the pandemic, and many of these valuation levels have been maintained, even as a path to relative normality has become clearer. Mega‑cap technology stocks have dethroned consumer staples and utilities as a source of market defensive positioning. We see significant crowding and momentum in some of these areas of growth, especially in SPACs, IPOs, and MEME2 stocks. We believe this is dangerous and requires prudence and active management to try to avoid significantly mispriced risk.

Is “Goldilocks” Possible? The Best Path Is Slow Normalization.

We are increasingly leaning toward a “goldilocks” scenario where we see lower inflation (than today) but higher rates (although still historically low). This could potentially be driven by:

- A significant slowdown in the Chinese economy as reform and regulation are implemented when they can be (i.e., right now, during the current period of high economic growth).

- An acceleration in COVID-19 cases from the delta variant, which slows economic recovery.

- Continued progress in improving supply chain functions. The cure for high prices is high prices, as is often quoted.

Complex Markets Require Deep Thinking

The challenges and opportunities for investors in current markets

For illustrative purposes only.

Goldilocks implies that “absurd” inflation fades and economic growth stabilizes. We would expect to see lower inflation as more workers return to jobs and tight supply conditions ease. This has the potential to evolve into a good environment for stock pickers but one that is bad for crowded growth trades and pure speculators. A “normal” environment is less speculative.

Back to School and Learning to “Live With COVID-19”

The next big macro catalyst will be back to school in the U.S. and whether this relieves the mismatch of labor supply and demand. American families with children have been a labor swing factor. If schools can stay open (enabling normal child‑care) while unemployment benefits roll off, we could see some normalization in labor supply and demand dynamics. This would be positive for risk because it points to the goldilocks scenario we mentioned above. The big question remains whether Americans (and the rest of the world) can adapt to “living with COVID” as opposed to a world without COVID‑19, which now looks very unlikely.

The Bottom Line for Global Focused Growth

We are comfortable with our portfolio, especially on a relative basis when compared with the barbells of growth and value factors. There are several segments of the portfolio where we are being carefully contrarian. We are searching for solid growth assets that are out of favor currently but where we see potentially higher growth in 2022 and beyond. This includes some travel‑related names. We also believe it is worth exploring China’s regulatory changes and the opportunities that it may create—albeit with prudence.

We have talked previously about stocks that have “crossed the chasm” during COVID-19, and we continue to look for companies that have expanded their addressable markets and opportunities while looking to avoid the “imposters.”

As we move through this extraordinary period, we continue to focus our time on the hard and difficult choices required in these complex times. Our aim is to own stocks where we have an insight about improving economic returns while avoiding stocks that imply unnecessary risks and should be avoided. This is our role as fundamental bottom‑up stock pickers.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution retail investors in any jurisdiction.

September 2021 / MARKETS & ECONOMY