May 2022 / INVESTMENT INSIGHTS

Keeping a Steady Hand in Uncertain Times

Volatility has not shaken our focus on long-term fundamentals

Key Insights

- The challenging macro backdrop means we have a subdued near‑term outlook for growth stocks.

- With an eye on compounding value, we seek names where we believe the market may not fully appreciate the length or strength of their growth stories.

- We remain selective, finding opportunities in names that we view as potentially steady growers and companies that we think are innovative disruptors.

Q. How have you been navigating this difficult environment for growth stocks?

The sell‑off in growth stocks has been challenging and painful. Correlations between equity performance often increase during big style rotations like the one that continued into the first quarter. Our patient strategy emphasizes high‑quality names that we believe have the potential to compound value durably over an extended time frame. The market did not necessarily recognize this distinction in the first three months of the year. But we remain confident in our process and belief that, over the long term, stocks tend to follow their earnings and free cash flow.

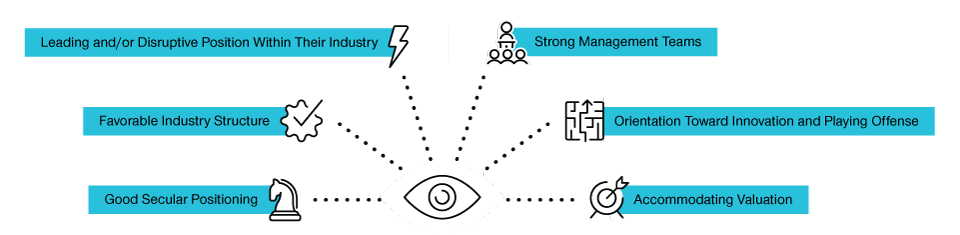

A Patient Approach Focused on Potential Long‑Term Compounding

(Fig. 1) What we look for when investing in a company

Source: T. Rowe Price.

For illustrative purposes only.

If we look beyond the broader weakness in growth stocks, the magnitude of some of the losses in individual names was notable. In this environment, differentiating between volatility and actual business risk is critical.

The significant drawdowns suffered by some of our communications services and information technology holdings appeared, in our view, to be exacerbated by the market’s fear and intolerance for corporate earnings that fall short of perfection. Regardless of any near‑term challenges, we do not believe that the longer‑term fundamentals for many of the online advertising and e‑commerce names in the portfolio have deteriorated to the extent that recent action in their stock prices might suggest.

Unfortunately, the declines in some of our portfolio holdings were more warranted. Robust demand at the height of the coronavirus pandemic for video communication and e‑signature solutions proved less sustainable than we expected. This tailwind also appeared to mask weaknesses in some software companies’ business strategies.

I am comfortable with the portfolio’s positioning and feel good about the companies in which we have invested, so our first‑quarter adjustments mostly occurred at the margin. When our holdings suffered pullbacks of a similar magnitude, we trimmed or exited some positions where our conviction was a bit lower and reinvested in names where we think the longer‑term risk/reward profile is more compelling.

Q. You mentioned the importance of differentiating between volatility and actual business risk. Tell us about an instance where emerging fundamental challenges prompted you to shift your long‑term views.

We assess emerging competitive threats very carefully, as the market tends to react quickly to the slightest whiff of potential disruption.

Consider the legacy payment processors, a group of companies that had earned a reputation as steady growers that benefited from the transition from cash to cards.

The dynamics in this industry remind me of traditional media in 2006. Although you could see the seeds of disruption from the rise of social media and streaming video back then, these competitive pressures did not start to show up in the incumbents’ financial results until 2013. And those headwinds intensified significantly in subsequent years.

We see the potential for a similar scenario to play out with the legacy payment processors. Given this view and our longer investment horizon, we prefer insurgents that offer compelling payment solutions and can innovate faster because their platforms are built on a modern technology stack.

Q. Over the six months ended March 31, 2022, you made some meaningful changes to the positioning at the top and bottom of the portfolio. How do these adjustments reflect your investment philosophy and process?

These adjustments did not stem from a change in process or the kinds of opportunities we seek. When I became manager of the strategy, the portfolio had a long tail of smaller positions that were sizable in number but marginal in terms of their total weighting. At the lower end of the portfolio, we want our decisiveness to translate into position sizes that still matter. For example, instead of holding a basket of several managed care companies, we own two high‑conviction names in this area.

Our other bottom‑up investment decisions increased the portfolio’s concentration at the top, narrowing some of the strategy’s prominent underweights relative to the Russell 1000 Growth Index and building overweight positions in other instances. These purchases were in keeping with our long‑standing process, which is rooted in rigorous fundamental research. We work very closely with T. Rowe Price’s analysts, who know inside and out the industries and companies they cover. In our view, these high‑conviction ideas should be able to compound in value over the long term and in a variety of different economic environments.

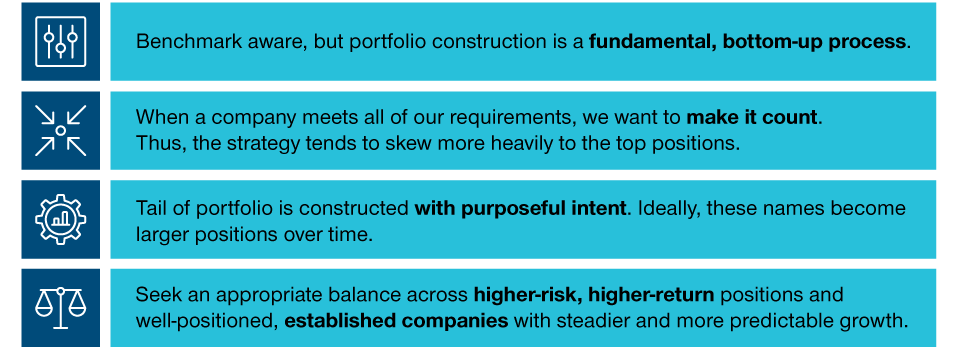

Building the Foundation for Potential Long‑Term Growth

(Fig. 2) Our thoughtful approach to portfolio construction

Source: T. Rowe Price. For illustrative purposes only.

We are methodical in our decision‑making. Our forward‑looking view on the companies in which we invest is not based on past performance but on how we view their prospects for long‑term value creation. We are also valuation conscious. We are willing to own some stocks that may look expensive in the near term, if we believe the rate at which the business is creating value is likely to support further upside potential in the coming years. However, we do not want to own names where, in our estimation, an extended valuation will get in the way of stock performance over a multiyear period.

Consider our position in Tesla. The automaker is a leader in electric vehicles (EVs), a product category that we believe represents a strong growth opportunity over the next decade. In our view, the potential combination of accelerating EV demand and constraints on the supply side could create a compelling fundamental backdrop for this company, especially if it executes on plans to scale up its production capacity.

Q. What is the rationale behind the portfolio’s limited exposure to cyclical sectors that tend to exhibit greater sensitivity to economic conditions?

We focus on a company’s underlying fundamentals and its potential to create value over a multiyear time frame. This approach involves making a single decision and, if our investment thesis plays out, should allow the power of long‑term compounding to do the hard work. Accordingly, our holdings typically fall into two general categories:

- Established companies that we believe can grow at a steady, predictable rate. We are happy to hold these names for the long term if we can enter at a valuation where we believe the company can compound value at an above‑market rate.

- Higher‑valuation companies where we see the potential for an extended run of strong growth as they seek to disrupt incumbents and take share in what we regard as a large addressable market.

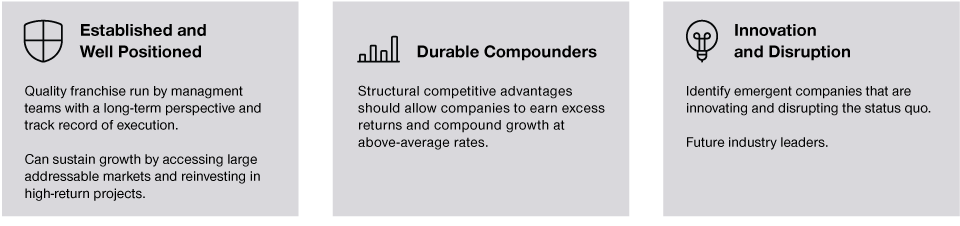

Focused on Fundamentals

(Fig. 3) The building blocks of companies that are potential compounders

Source: T. Rowe Price. For illustrative purposes only.

We are unlikely to reorient the portfolio materially to try to time inflections in the economic cycle. Accurately predicting the course of the business cycle is an extremely difficult proposition. Buying a stock because the company should do well at one point in the cycle and then selling it at another juncture requires that you make multiple good decisions for the trade to work effectively.

We tend to gravitate to names where we believe that the underlying business has a good chance of holding up well and growing through the economic cycle, even if the stock itself might experience bouts of volatility along the way. Achieving this consistency can be harder for companies whose growth prospects are tied to ebbs and flows in the broader economy.

Our approach to investing in the financials sector shows these principles at work. We prefer to invest behind names that we believe offer exposure to more durable upside catalysts than just the prospect of rising interest rates, even if that would be a tailwind.

In our view, the banking industry is in the relatively early stages of a digital revolution where convenient, user‑friendly software and applications will take precedence over the physical branch network. Competing in this intense environment will require significant technological investment and strong execution—a challenging prospect that creates a great deal of uncertainty for legacy business models.

We favor financials companies that we believe are positioned to benefit from these disruptive trends over the longer term. For example, we see the potential for an investment bank that we own to be an attractive partner for fintech innovators because of its size and scale. At the same time, we view the company’s limited exposure to some of the banking industry’s most at‑risk legacy business lines as a potential competitive advantage.

Q. Where are you finding opportunities?

We think that the widespread sell‑off in growth stocks, while quite painful, has created some attractive opportunities in would‑be disruptors.

One name that we like is a leading online retailer of used cars in the U.S. We believe that by significantly improving the consumer’s experience, this company should be able to take share in the highly fragmented market of used‑car dealers. Although this name could experience further volatility and operational challenges in the near term, we like the company’s business model and view its growth potential as compelling over a multiyear time frame.

We also see opportunities in established companies that we believe have the potential to be all‑season compounders, thanks to strong competitive positions and defensive characteristics.

In the consumer discretionary sector, we like select retailers that, in our view, should be well positioned for the long term as well as in the current inflationary environment. One of our favorite names is a discount retailer that focuses on rural towns where competition typically is not as intense. Not only do we believe that low in‑store prices and the convenience of one‑stop shopping can help this retailer to attract and retain customers, but we also see the potential for the company to grow by opening new locations and expanding in certain product categories.

Q. What’s your outlook?

Our expectations for growth stocks are somewhat subdued for the remainder of the year. The Federal Reserve and other key central banks are still early in their efforts to tighten monetary policy, suggesting that the rate of change in interest rates could be on the higher side versus when this process is further along. The lapse of the unprecedented fiscal stimulus unleashed last year could also create difficult year‑over‑year comparisons for some companies, especially consumer‑facing businesses. Meanwhile, China has imposed lockdowns to curtail coronavirus outbreaks in large metropolitan areas, disrupting supply chains and economic activity. Russia’s invasion of Ukraine is another source of considerable uncertainty. All these factors could make investors more skittish.

Nevertheless, we remain bullish on growth stocks over a multiyear horizon. We do not claim to have an edge in predicting near‑term macro developments or timing shifts in investor sentiment. However, as some of these macro‑level uncertainties resolve themselves and begin to stabilize, we see the potential for the market to refocus on companies’ underlying business fundamentals. And to the extent that inflationary pressure and rising interest rates eventually spur concerns about economic growth, these conditions may burnish the appeal of the special companies that we seek: businesses that we think exhibit the potential to compound value by sustaining strong growth rates in a variety of macroeconomic environments.

The near‑term environment may be challenging. However, we remain committed to our patient investment strategy.

The specific securities identified and described do not represent all of the securities purchased, sold, or recommended for advisory clients, and no assumptions should be made that investments in the securities identified and discussed were or will be profitable.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.