May 2022 / INVESTMENT INSIGHTS

The Road to Net Zero

How the world is moving forward on emissions reduction

Key Insights

- Many countries have now established net zero targets—making energy transition an important factor from a fiduciary responsibility perspective.

- Data availability has continued to improve in that more companies are choosing to report, but a lack of standardization is still an issue.

- We are seeing a demand for products that invest in companies that finance climate solutions, commit to greenhouse gas reduction targets, or both.

Many entities, including federal and regional governments, corporations, universities, and investors are setting net zero targets—as the world looks to tackle climate change. Net zero means achieving a balance between the greenhouse gases (GHG) put into the atmosphere and those taken out. This state is also referred to as carbon neutral. The focus on net zero targets accelerated in 2021 and was one of the key objectives of COP26 (the 2021 United Nations Climate Change Conference). Coming out of the summit, more than 140 countries—accounting for 90% of global greenhouse gas emissions—had established net zero targets.1

The fact that so many countries have made this commitment makes energy transition an important factor from a fiduciary responsibility perspective. The net zero emissions reduction trajectory is a severe one—it requires a 50% reduction in GHG emissions between 2020 and 2030 and reaching net zero by 2050. It is incomparable with any energy transition that has ever taken place in modern history. Even if governments only partially achieve their goals, it will be highly disruptive to industry and macroeconomic trends.

Looking at the enormity of the task at hand, many want to do their part to aid the energy transition. At T. Rowe Price, we see this in demand for products that invest in companies that finance climate solutions, commit to GHG reduction targets, or both. To this end, we have joined the Net Zero Asset Managers initiative and are committed to developing investment products with net zero objectives to help meet the needs of these clients.

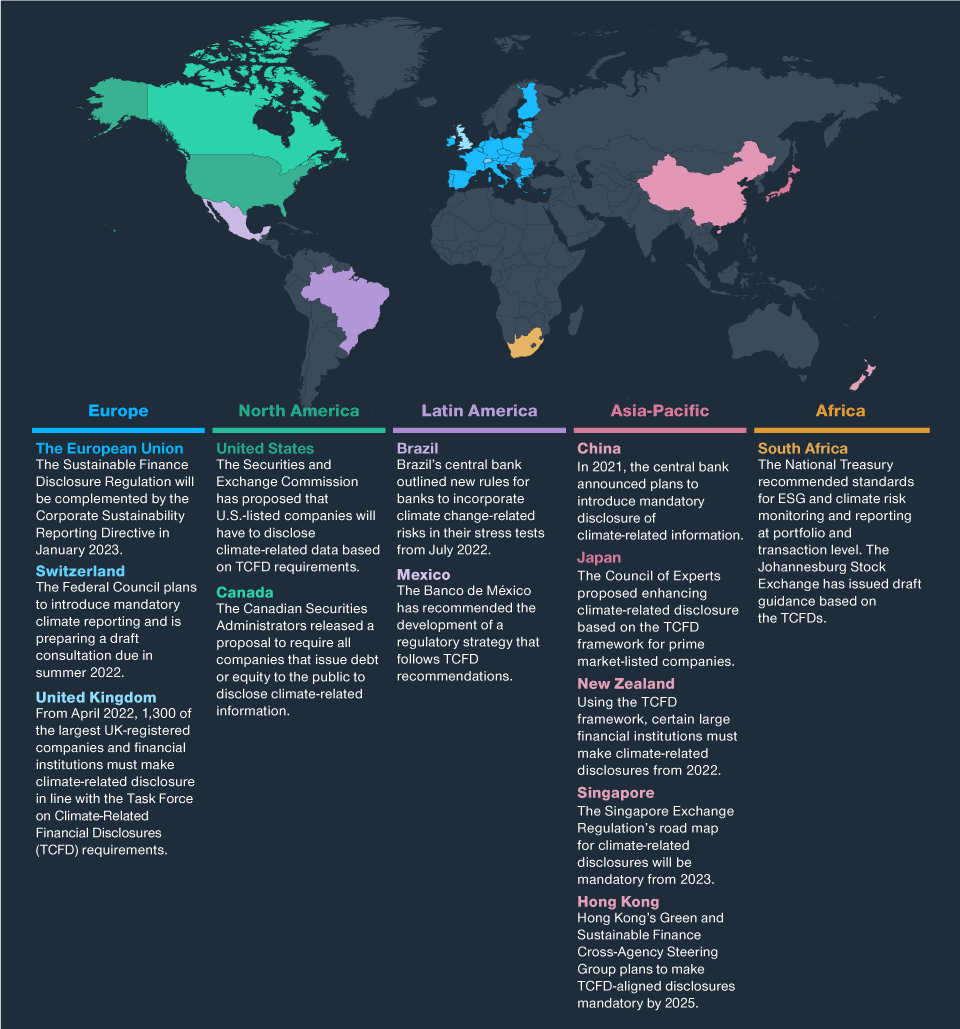

The Rise in Mandatory Climate Reporting

(Fig. 1) Will compulsory climate reporting become the norm?

As of March 31, 2022.

Sources: S&P Global Sustainable, Allen & Overy, Norton Rose Fulbright, Sustainable Stock Exchange Initiative. Analysis by T. Rowe Price.

Politics: What’s Happened and What to Expect

The COP26 summit held in Glasgow last November was driven by climate urgency. The impact of climate change has become much more real to politicians as major storms and other weather events are becoming more prominent. Whether or not the summit was successful is in the eye of the beholder. Technically, success should have been gaining agreement for all parties to limit global warming to 1.5°C, backed up with Nationally Determined Contributions (NDCs)—plans submitted by each nation that detail how they will deliver on GHG reductions. That did not happen as the aggregate NDCs fell well short of net zero 2050, but, given the enormity and difficulty of the task at hand, that probably was not a realistic expectation for COP26.

While politicians may have done well for the hand they were dealt, COP26 can only be viewed as a failure through the lens of climate change math. A range of estimates have come out regarding the commitments made at Glasgow, which imply a warming scenario of at least 1.8°C–2.1°C at the end of the century. The 1.8°C estimate comes from the International Energy Agency and has been criticized for making some heroic assumptions.2 The 2.1°C estimate assumes full implementation of the NDC targets and has a heavy reliance on strong progress being made between 2030 and 2050. More realistically, the Climate Action Tracker highlights that the 2030 targets are not ambitious enough and would put us on course for 2.4°C of warming.

As part of the Glasgow agreement, countries will resubmit their NDCs ahead of COP27 and have specifically been asked to improve their 2030 targets. A key take‑away from the talks is an acceptance that countries will meet more frequently to review their targets and measure progress against them.

Another giant gap in the equation for investors is corporate disclosure of GHG emissions data, something we also discussed in last year’s ESG Annual Report. Data availability has continued to improve from a year ago in that more companies are choosing to report, but a lack of standardization is still an issue (which means that when two companies report their GHG emissions, the comparison may not be apples to apples). Regulators are starting to address the issue, but reporting GHG emissions is still not mandatory in most places.

Evaluating Climate in Investments

With more than 140 countries (accounting for 90% of global greenhouse gas emissions) having established net zero targets, understanding how our investments are positioned in this changing landscape is essential to fulfilling our role as an asset manager. Similarly, many of our clients recognize this potential investment risk and want to understand how their portfolios are positioned regarding the energy transition. To this end, we provide quarterly greenhouse gas footprint profiles for a range of investment portfolios that we manage, where enough data are available.

Of course, isolating climate into a single factor such as GHG footprint can be misleading—it would be akin to financial analysis taking only the income statement into account and ignoring valuable insights from the balance sheet and cash flow statement. A GHG footprint gives you a “point in time” analysis and misses key items, such as the historic and forward trajectory of emissions and exposure to climate solutions. More importantly, a myopic view on GHG footprints could lead an investor to investing only in low emitters, thereby ignoring the prospect of GHG reductions in the real economy.

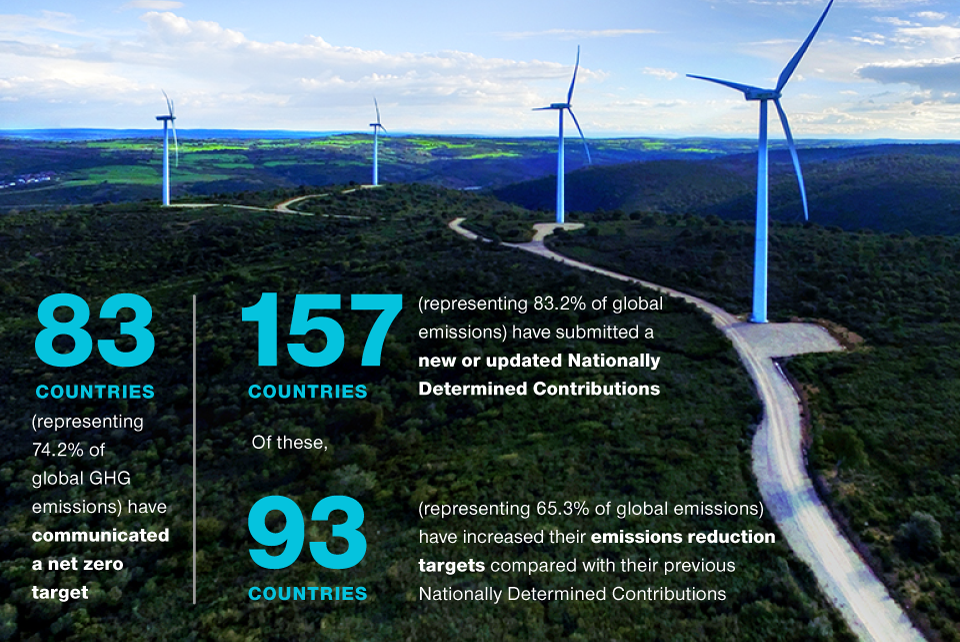

Global Commitments to Greenhouse Gas Reductions

(Fig. 2) Current NDCs are falling short

As of March 2022. Current aggregate Nationally Determined Contributions (NDCs) fall short of what is needed to reach net zero by 2050. Source: Climate Watch. 2020.

Washington, DC: World Resources Institute. Available online at:

https://www.climatewatchdata.org. World Bank. 2017. Nationally Determined Contributions (NDCs). Available at:

http://spappssecext.worldbank.org/sites/indc/Pages/INDCHome.aspx.

In recognition that net zero is a complex topic that cannot be boiled down to a single data point, we are committed to expanding transparency around climate reporting. Due to data availability and other limitations, this will take time—but we are committed to continued progress.

Investment Products Targeting Net Zero

Some clients want to go further than considering energy transition as an investment risk—by specifically targeting GHG reduction as an investment goal. A good example is the Net-Zero Asset Owner Alliance. The UN‑convened alliance includes 71 asset owners controlling more than USD 10 trillion that are committed to transitioning investment portfolios to net zero greenhouse gas emissions by 2050.

We have been working with clients that are members of the Net-Zero Asset Owner Alliance as well as other clients looking to set GHG reduction targets on their portfolios. This is something that can be more easily accomplished when the client (typically institutional) has set up their own separate account. Committing to a specific GHG reduction target limits the investment universe and, by default, prioritizes an environmental target over financial performance—not every client in an existing pooled asset would want this to take place.

Nevertheless, we recognize that there are many clients who wish to apply net zero targets to their investment portfolios but, for various reasons, need to rely on pooled investment vehicles. For this reason, we are seeking to develop investment products with net zero objectives to meet their needs.

Ultimately, by signing up to the Net Zero Asset Managers initiative we are illustrating our commitment to developing products with net zero objectives. It also underlines our intention to help promote best practices and create industry standards around net zero portfolios.

The Net Zero Asset Managers Initiative

As of April 25, 2022, T. Rowe Price has become a signatory of the Net Zero Asset Managers initiative (NZAMI).

NZAMI is an international group of asset managers committed to supporting the goal of net zero greenhouse gas emissions by 2050 or sooner, in line with global efforts to limit warming to 1.5°C. It launched in December 2020 as a sibling organization to the Net-Zero Asset Owner Alliance, with the aim of galvanizing the asset management industry to provide products suitable for asset owners committing to net zero goals.

NZAMI has grown to include 236 signatories with USD 57.5 trillion assets under management (as of December 31, 2021).3

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution to retail investors in any jurisdiction.