November 2021 / MARKETS & ECONOMY

Banks Set to Play Critical Role in Climate Change Fight

Transition to a low-carbon economy brings lending risks and opportunities

Key Insights

- With intensifying urgency on climate change action, it is crucial that banks are proactive in addressing climate change risks in their lending activities.

- While the financial impact of aligning lending portfolios to climate goals is likely to be small and occur over the medium to long term, actions taken can skew positively through green financing opportunities or negatively if banks simply exit certain climate‑sensitive sectors.

- In managing the transition to net‑zero carbon emissions, banks adopting broad‑brush sector exclusions over a risk mitigation approach will make it more difficult for certain climate‑sensitive industries to transition their businesses.

Looking ahead to the UN’s Climate Change Conference (COP26) in Glasgow this November, it is perhaps timely to consider the implications of the climate change agenda on the world’s banking sector. Indeed, one of the core goals of the conference is to mobilize the world’s financial institutions around their contributions to climate finance to help ensure that we meet the net‑zero targets.

As key financers of the economy, banks will play a pivotal role in the transition toward a low‑carbon economy through both green financing and efforts to align lending portfolios to the goals of the 2015 Paris Agreement on climate change, which aims to keep the global temperature rise to around 1.5oC compared with preindustrial levels. This shift will be challenging, but new opportunities may present themselves.

Pressure Building for Banks to Act on Climate Change

Leading banks are around three years into the process of addressing climate change risks on their business models. Action to date has mainly focused on screening and measuring loans for environmental, social, and governance (ESG) risks, but the pressure to do more is building from multiple fronts.

The world’s banking regulators are putting climate risk at the top of the agenda. Climate risk stress tests are being carried out in several jurisdictions, including the UK, Japan, Australia, and Europe. While there are no concrete announcements from U.S. regulators, the Federal Reserve has identified climate change as a risk to financial stability1 and, in December 2020, joined the Network for Greening the Financial System. Furthermore, Fed Governor Lael Brainard endorsed mandatory climate risk disclosures and “scenario analysis” tests in a February 2021 speech,2 while Chair Jerome Powell signaled that climate stress tests are “proving to be a very profitable exercise, both for financial institutions and regulators” in a July 2021 speech.3 As such, there are signs that the U.S. is moving in the direction of a climate stress test, which would bring them closer to regulatory peers in other major developed countries.

Meanwhile, there’s meaningful scrutiny by nongovernment organizations, such as the Rainforest Action Network, which publishes a “name and shame” report of banks’ annual fossil fuel financing. Reports like these are reputationally harmful, and companies named often become the target of shareholder resolutions at annual general meetings.

Climate change litigation is also on the rise, however, banks have not been materially targeted to date. Since 2015, there has been an increase in the number of climate risk litigation cases, with the majority filed in the U.S. Most have been filed against governments, but we are beginning to see companies named in lawsuits, particularly against the energy majors. The risk of future lawsuits cannot be ruled out, so banks would be wise to proactively align their portfolios to the Paris Agreement to avoid this low‑probability tail risk.

Against this backdrop, we believe that the more proactive a bank is in managing and reducing climate risks on their loan book, the lower the reputation risks are likely to be in the future.

Two Paths on the Road Map to Net Zero

As part of the transition, we believe banks will need to make difficult decisions about which sectors and clients to finance. We believe there are two possible approaches that banks could adopt:

Sector exclusion (risk avoidance) or

Working with existing clients to transition (risk mitigation)

We advocate that banks adopt risk mitigation and are encouraged so far that this avenue is proving to be the more popular. Exclusionary approaches, where banks completely exit a sector and stop all financing, may be easier to implement and explain to stakeholders, but we do not view this as the most helpful approach for reducing a bank’s lending risk or transitioning the economy to net zero. Instead, we believe that banks and the global economy are served better by taking a risk mitigation approach (i.e. working with clients on their efforts to transition to net zero). Ultimately, we believe that the lender and economy will benefit from supporting a high‑emitting company achieve net zero, but it is paramount that a bank financing a “high‑emitting transitioner” has a robust and effective process to ensure that the borrower has a genuine, credible plan to achieve net zero. Its also important to recognize that a risk mitigation approach will likely result in a bank excluding many high‑emitters, but this will only occur after a thoughtful evaluation of their business plans.

Banks are moving beyond screening loans for ESG risks toward instituting net‑zero financed emissions targets to align their lending portfolios to the goals of the 2015 Paris Agreement. As a result, banks are setting net‑zero financed emissions targets for 2050—these targets are relatively easy to make but harder to operationalize. We would encourage banks that have made these pledges to articulate how they will transition their balance sheet to meet them so progress can be monitored and measured.

Financial Impact of Transitioning

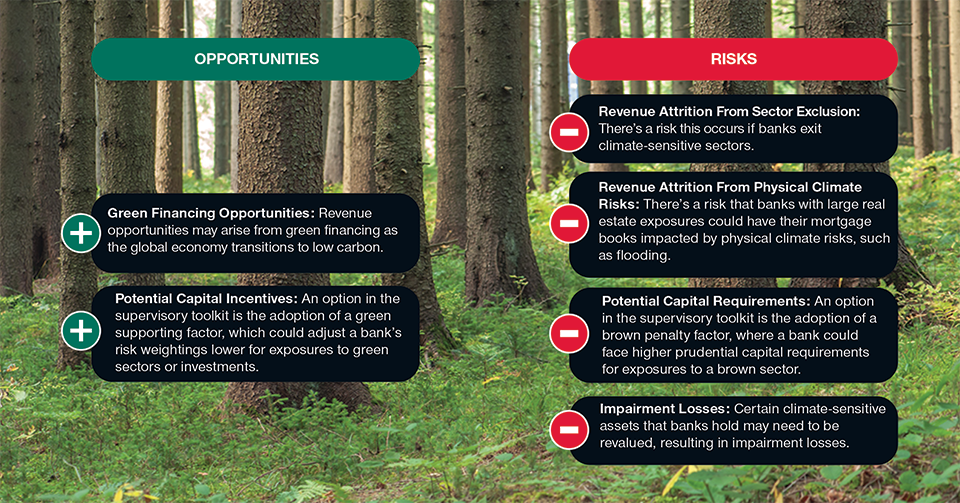

(Fig. 1) Potential revenue opportunities and risks for banks

As of September 30, 2021.

Source: T. Rowe Price.

So far, more than 50 banks from across 29 countries have signed up to the Net‑Zero Banking Alliance, an industry‑led initiative convened by the UN whose members have committed to bringing their lending and investment portfolios to net‑zero emissions by 2050 or sooner. Furthermore, signatories commit to publishing their progress annually and setting a net‑zero 2030 target for their most polluting sectors within 18 months of joining. While this is encouraging, we need to see more banks join and formalize their plans as just being on autopilot won’t get the sector to net zero.

Financial Impact Could Skew Positively or Negatively

We anticipate that the financial implications of the transition are likely to be small due to the general diversified nature of banks’ loan books and the long time horizon for the shift. Despite this, the finance implications have the potential to skew either positively or negatively depending on how proactive the bank is in aligning its lending portfolio.

On the positive side:

Green financing opportunities: Revenue opportunities may arise from green financing as the global economy transitions to low carbon, with the Global Financial Markets Association and Boston Consulting Group estimating that an annual investment of between USD 3 trillion and USD 5 trillion4 is required to achieve the ambitions set out in the Paris Agreement.

Potential capital incentives: An option in the supervisory toolkit is the adoption of a green supporting factor, which could adjust a bank’s risk weightings lower for exposures to green sectors or investments. This could be an opportunity for banks to lower their capital requirements. Although it’s too early to say whether this will happen or not, it is an option at regulators’ disposal if they seek to encourage more green lending.

On the negative side:

Revenue attrition from sector exclusions: There’s a risk that this will occur if banks exit climate‑sensitive sectors. According to independent research firm Autonomous, banks derive on average around 12% of their revenue from climate‑sensitive sectors, so this revenue may be lost if banks completely stop providing them with financing. But with the exit from these sectors likely to be gradual and over an extended period, we expect the revenue lost to be manageable.

Revenue attrition from physical climate risks: There’s a risk that banks with large real estate exposures could have their mortgage books impacted by physical climate risks such as flooding. While this is a potential danger, we believe the revenue impact will be negligible, with the majority of revenue attrition likely to come from transition risks instead.

Laggards may be subject to capital requirements: Banks are required to hold capital to guard against a number of risks. We believe results from regulatory climate stress tests may eventually feed into prudential capital requirements, but it’s too early to tell when and how and the scope of the requirements.

Impairment losses: Certain climate‑sensitive assets that banks hold may need to be revalued, resulting in impairment losses.

Lack of Reporting Standardization Poses a Challenge

At T. Rowe Price, we strongly advocate that our investee companies align their ESG disclosure to global standards. We suggest the Sustainability Accounting Standards Board (SASB) and Task Force on Climate‑related Financial Disclosure (TCFD). TCFD aligned reporting requires companies to disclose their governance, climate strategy/targets, risk management, and performance metrics relating to climate change, but there are concerns that the standard’s definition of climate‑sensitive sectors is too narrow as it only includes energy and utilities, excluding renewables; water utilities; and nuclear energy.

As there is no standardized framework for reporting, banks are disclosing different levels of details, making it hard to make comparisons. Some banks provide more granular breakdowns, although a wide variety of sector categorizations are used. There is room for improvement on the standardization of the banking sector’s climate‑related disclosures. We would note that the European Banking Authority’s proposed new Pillar 3 requirements for disclosing ESG risks set out some common standards that should help provide more consistency on carbon‑intensive industries if/when they take effect.

Banks in Action on the Climate Change Battle

A key goal of COP26 is securing commitment from developed countries to mobilize climate finance of at least USD 100 billion per year to help facilitate attaining global net‑zero emissions by mid‑century. Here, the role of banks will be crucial, and most leading institutions have now set targets for sustainable and green financing. For example, HSBC plans to provide between USD 750 billion and USD 1 trillion in low‑carbon financing by 2030, while Bank of America announced plans in April 2021 to upsize its sustainable financing target from USD 300 billion to USD 1 trillion by 2030.

Industry Initiatives

(Fig. 2) An array of initiatives that banks may join to help assess climate risks

As of September 30, 2021.

1 Source: https://www.unepfi.org/net‑zero‑banking/.

2 Source: https://equator‑principles.com/.

3 Source: https://sciencebasedtargets.org/sectors/financial-institutions#about-the-project.

Source: T. Rowe Price.

However, with variation in what banks define as green and the activities that qualify as financing, caution is warranted before making comparisons between institutions. Regardless, we believe there is a potential revenue opportunity for those banks that are at the forefront of green financing. Banks may even receive capital incentives for green financing in the future, similar to programs such as those launched by central banks in the past to encourage lending to small and medium‑sized businesses. For example, the Pillar 1 capital requirements—the minimum capital that banks have to hold for credit and operational risks—could be lowered for a bank’s exposure to green assets.

Additional efforts are seeing banks sign up to a number of industry initiatives highlighted in Fig. 2, which help them assess climate risks on specific loans.

We expect that there will be growing calls for banks to join these industry initiatives and advocate, in particular, that banks sign up to the Net‑Zero Banking Alliance and/or the Science‑Based Targets initiative, given the sector take up so far and credibility.

Adapting Practices for the Evolving Climate Crisis

A proactive approach in the current environment is paramount. With the increased attention from regulators and growing scrutiny from shareholders and nongovernment organizations, banks could suffer reputational damage unless they take steps to align their portfolios to the goals of the 2015 Paris Agreement. While a lack of standardized frameworks is an immediate challenge, we expect that best practices and common guidelines will emerge over time.

IMPORTANT INFORMATION

This material is being furnished for general informational and/or marketing purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, nor is it intended to serve as the primary basis for an investment decision. Prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested.

The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction.

Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price.

The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request.

It is not intended for distribution retail investors in any jurisdiction.

October 2021 / INVESTMENT INSIGHTS